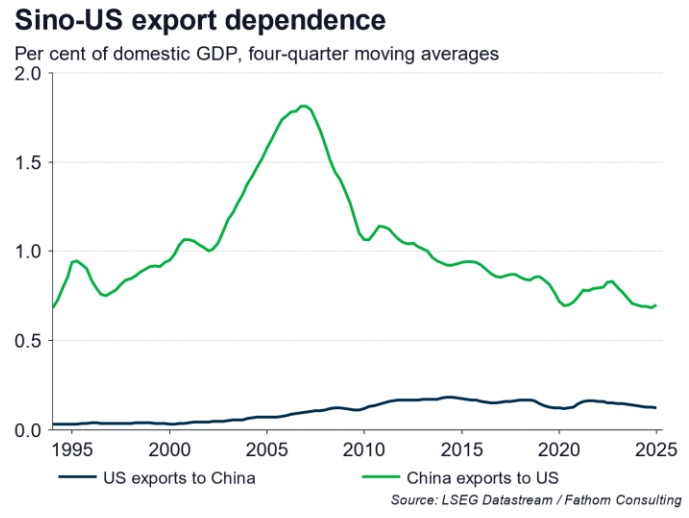

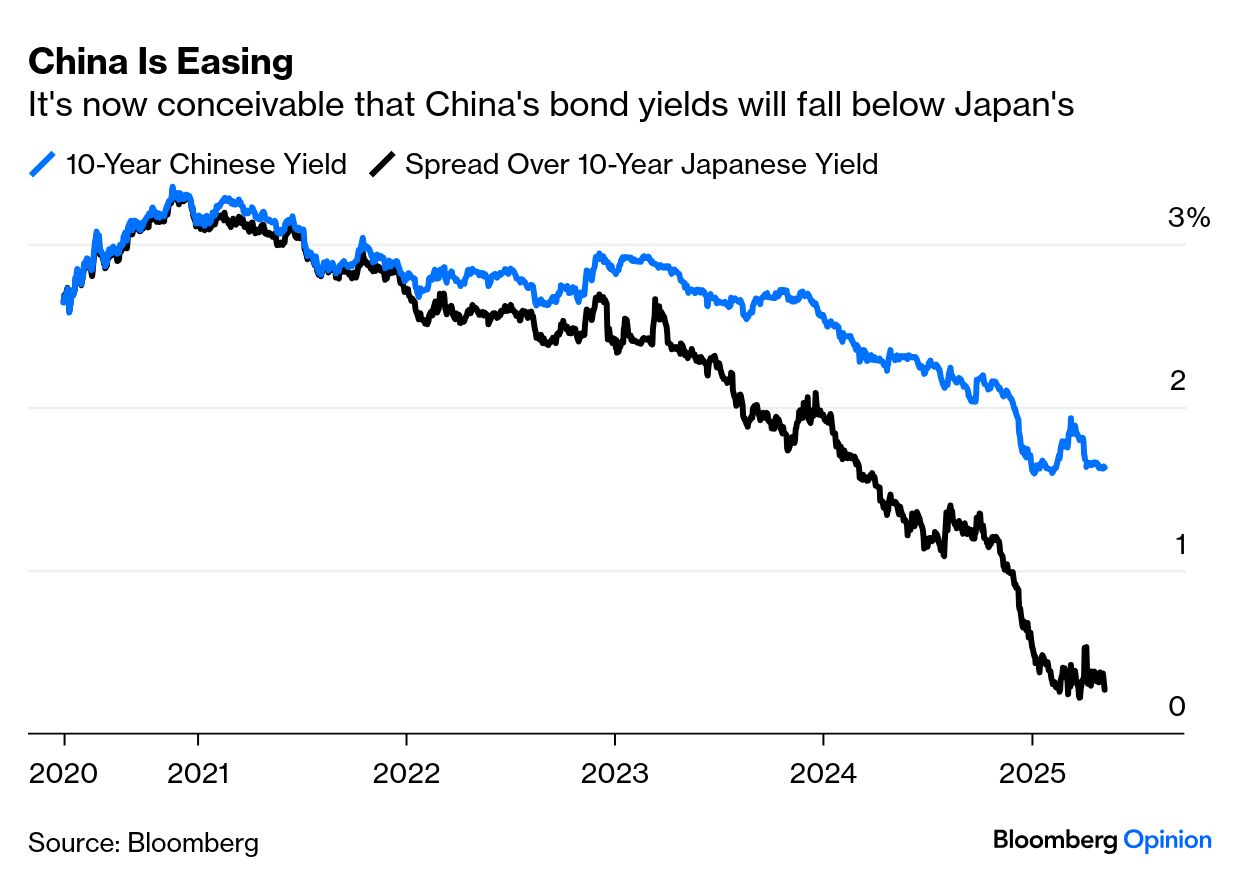

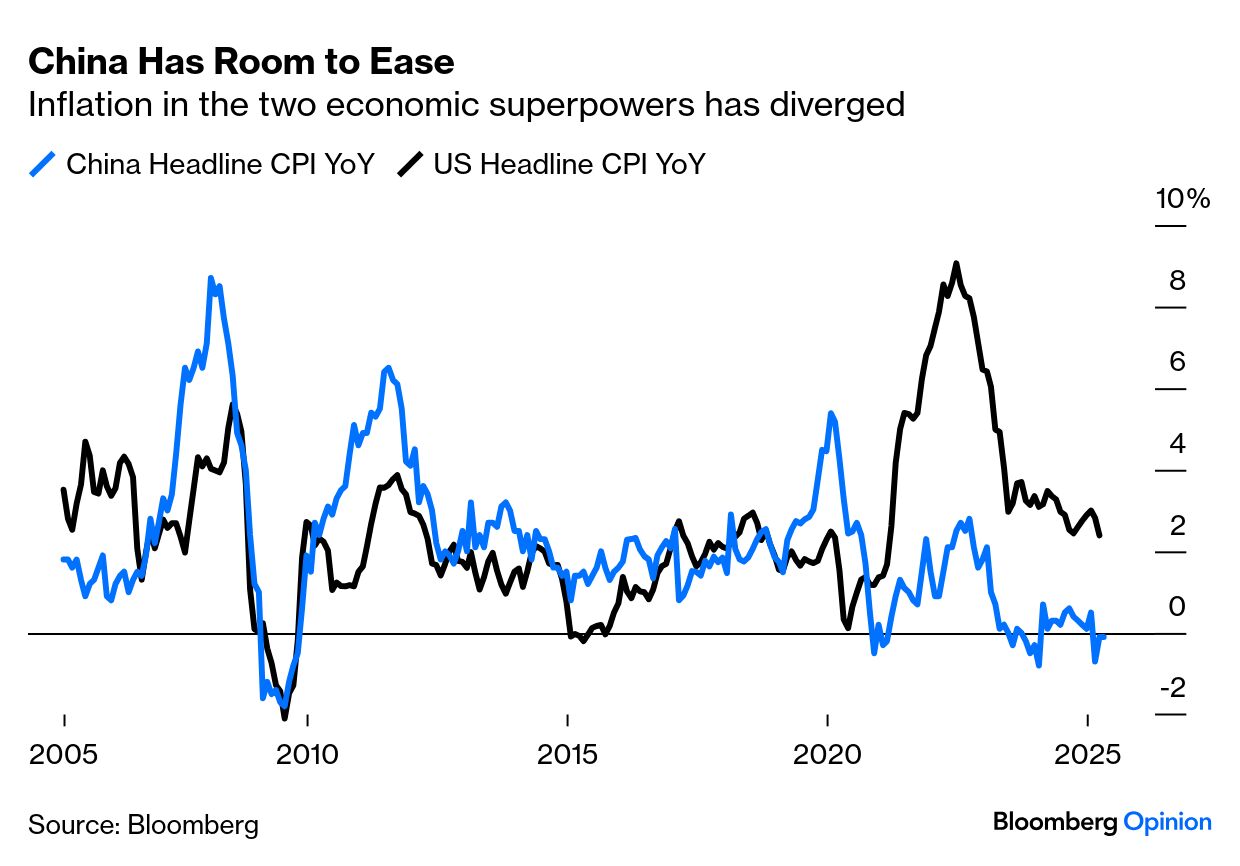

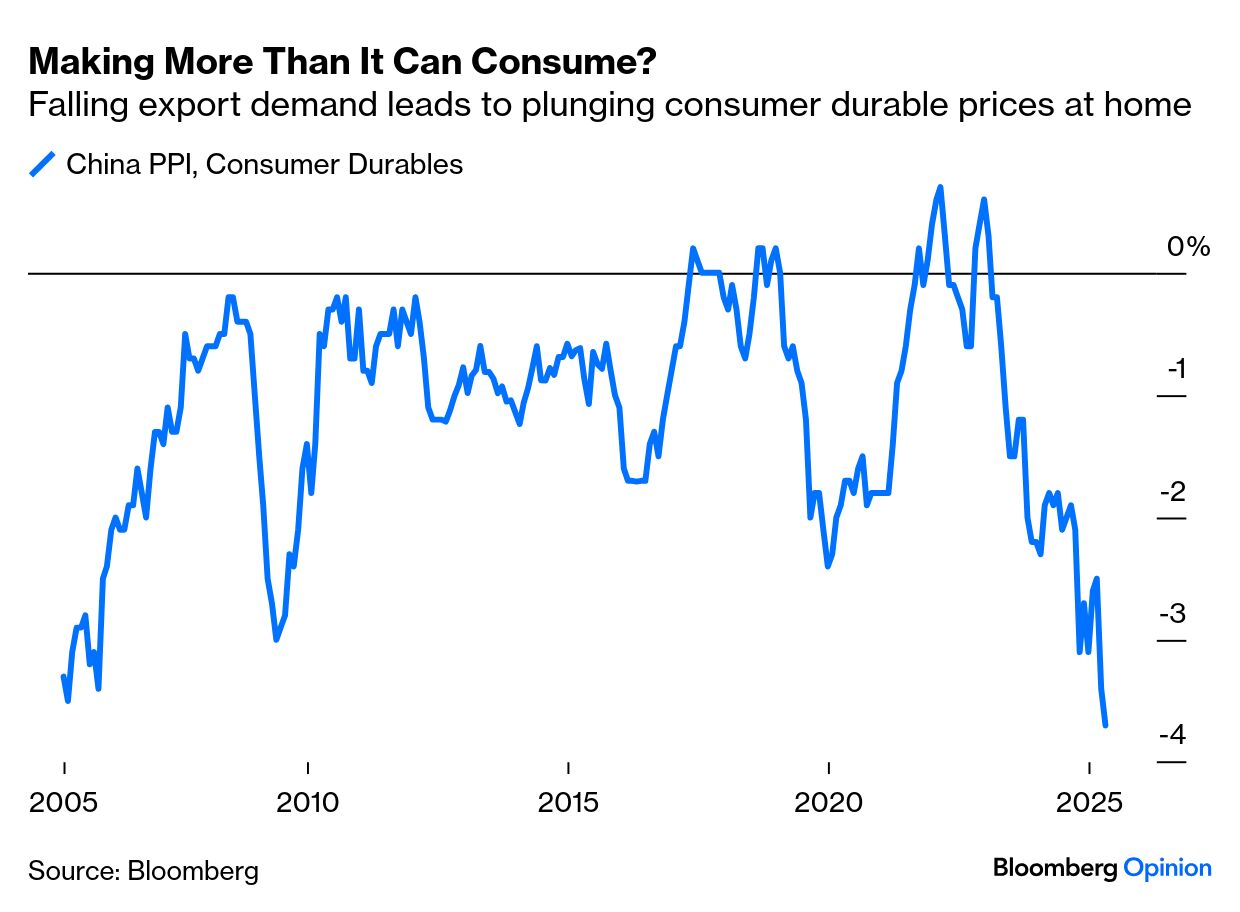

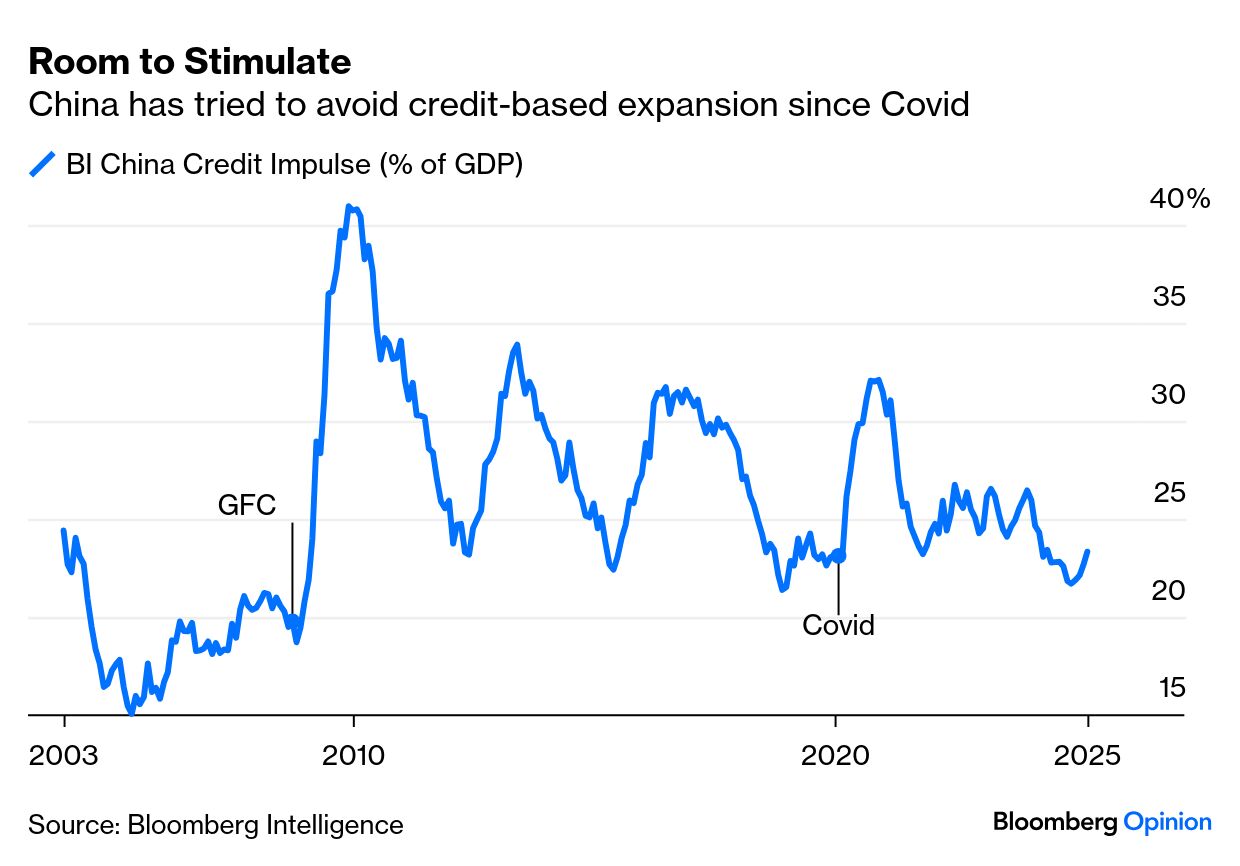

| China’s economic reforms can be likened to a bird and a cage. So said Chen Yun, the deputy to Deng Xiaoping and a key driver of economic reform in the 1980s. The bird was the economy, the cage the party’s plan. “A bird cannot be held tightly on your hand, otherwise it will die. It must be allowed to fly, but only within the cage. Without a cage, the bird will fly away.” This extraordinary analogy provides the title for a new book, The Bird and the Cage — China’s Economic Contradictions by Nicholas Borst, and it makes the history of the last 50 years much easier to understand. President Xi Jinping was never going to allow the bird of economic liberty to escape the cage altogether, and so the clampdown on the private sector began. Now, China’s contradictions must bump against the need to win its trade war with the US. The Communist Party never let the bird out of the cage, which gives it certain advantages — it can force its people to put up with austerity and outlast a democracy where the leadership might suffer retribution from the electorate. The planned, or caged, nature of China’s economy also lends itself to war-time strategizing, as the country can still be run from the top down in a way the US cannot. China’s plan has long been to reduce dependence on exports and develop a consumer economy driven by a growing middle class. The first art has happened, as this chart from Elisabeth Werenskiold of Fathom Consulting in London demonstrates: The outline of how China is proceeding is now clear. After a brief reversal, the historic fall in 10-year bond yields has resumed. The landmark moment when they actually slip below the yields on Japanese government bonds again seems as though it could be imminent: Meanwhile, the fall in inflation suggests that it has no choice but to stimulate, and do so in a big way. Headline CPI is now running very slightly negative, and the country has now swapped places with the US. While the Federal Reserve needs to be cautious about cutting rates, the People’s Bank of China does not. US tariff policy would tend to be inflationary for Americans and deflationary for everyone else, so there is every chance that these trends will be exacerbated: China’s deflation issue is most dramatic if we look at the producer price index for consumer durables, which is now deflating at an annual rate of almost 4%, the lowest in two decades. This suggests the country is swamped with products it can no longer sell to the US, while domestic demand is still insufficient to fill the gap: The authorities have started to ease, and they have a lot further they could go. It has been their aim to wean the country off credit and ensure that China avoids its own Lehman moment, which is why it has eschewed monetary stimulus for an unusually long time since the pandemic. That gives space to expand now: The path seems clear; China is going to have to open the taps again. That could store up more risk of financial turmoil for the future. In the present, it implies good things for both Chinese bonds and stocks. The caged bird of the domestic securities markets will get to sing for a while as the party maneuvers to stay in control. Long before artificial intelligence euphoria hit Wall Street, digital finance was already reshaping the foundations of global markets, transforming how value is stored, transferred, and trusted in an increasingly connected world. Blockchain technology not only enabled crypto currencies, but led to tokens of real assets (or tokenization), which investors can access. This S&P Global report shows that tokenizing private credit could ease the process of buying into private-credit funds and trading shares. But adoption is hampered by the absence of cross-border regulatory frameworks. Without them, siloed approaches are undermining the benefits digital assets are supposed to deliver. And so a new CFA Institute paper argues that taking digital finance, or tokenization, to the next level requires legislatures to establish a legal status for these assets. Globally, investors in the nearly $3 trillion digital asset market face a challenge enforcing ownership rights and identifying the responsible issuer or issuing entity. CFA Institute's Olivier Fines argues that tokenization could drive the convergence of capital markets and technology, and remove the layers of financial intermediaries needed to validate transactions: If you think you own your house, there's somewhere in public that is able to affirm that yes, Mrs. Smith owns that house and here's the record in the digital finance space – a blockchain. What gives faith in the process is the distributed ledger. The irony here is that it would be boring if the conclusion from that logic [were] that I might want to reintroduce an entity in the middle to act as guarantor and we reintroduce all the scaffolding that we got rid of in the first place.

Regulators need to get principles in place to avoid having to reintroduce all the friction points that now exist. This “club sandwich” of institutions — banks, clearinghouses, and registries — Fines argues, work together to confirm ownership, balances, and trust. This is why a bank statement is trusted to reflect actual funds. In a digital finance ecosystem where trust and verification are built directly into the technology intermediaries would become obsolete. With the next generation more familiar with crypto assets, streamlining regulation is more pressing than ever. But this shouldn’t happen too quickly. “A number of principles we will not deviate from,” says Fines. “This has to be done with fiduciary duty in mind, with the notion that your assets are safe from predation.” Digital assets’ market capitalization still pales compared to equities, which are worth more than $110 trillion globally. So it’s not surprising that clear global rules are lacking. Still, the potential of digital finance is unmissable. Trump’s crypto-enthusiasm suggests a more supportive regulatory regime ahead. His order, Strengthening American Leadership in Digital Financial Technology, aims to bolster US digital assets. The expectations of a supportive regime have buoyed cryptocurrencies in recent months. Trump’s executive order piles on the growing number of documents aiming to shape digital finance. A University of Cambridge database of regulatory policy documents on crypto from 17 jurisdictions shows a remarkable rise: An analysis of these documents shows regulators are worried about the risks related to crypto asset exchange rules, requirements for brokers operating on exchanges, risk assessments of crypto assets, and custody/wallet requirements. A legal status for tokens is needed as a starting point to foster trust and enable market expansion. Giovanni Bandi, one of the paper's authors, points out that defining links between real-world assets and their digital representations, particularly regarding property rights, are necessary. This would encourage investment and innovation in tokenized assets, which are projected to expand to $16 trillion by 2030. If there’s one reason why a universal legal framework is needed, it’s FTX. The spectacular collapse of Sam Bankman-Fried’s crypto platform has dampened expansion. As long as a repeat remains technically possible, Fines says, “I do not think that digital finance has a very bright future.” -- Richard Abbey |