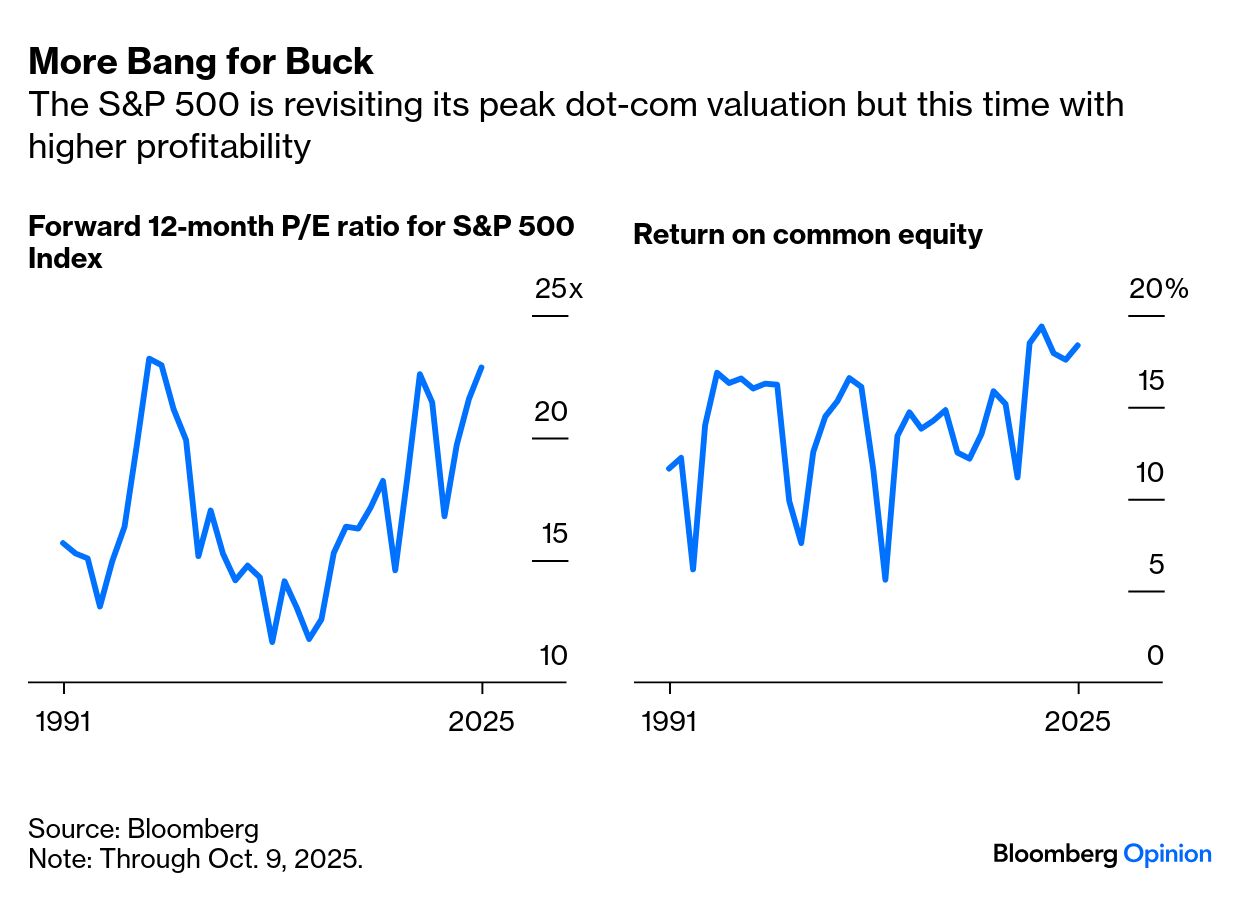

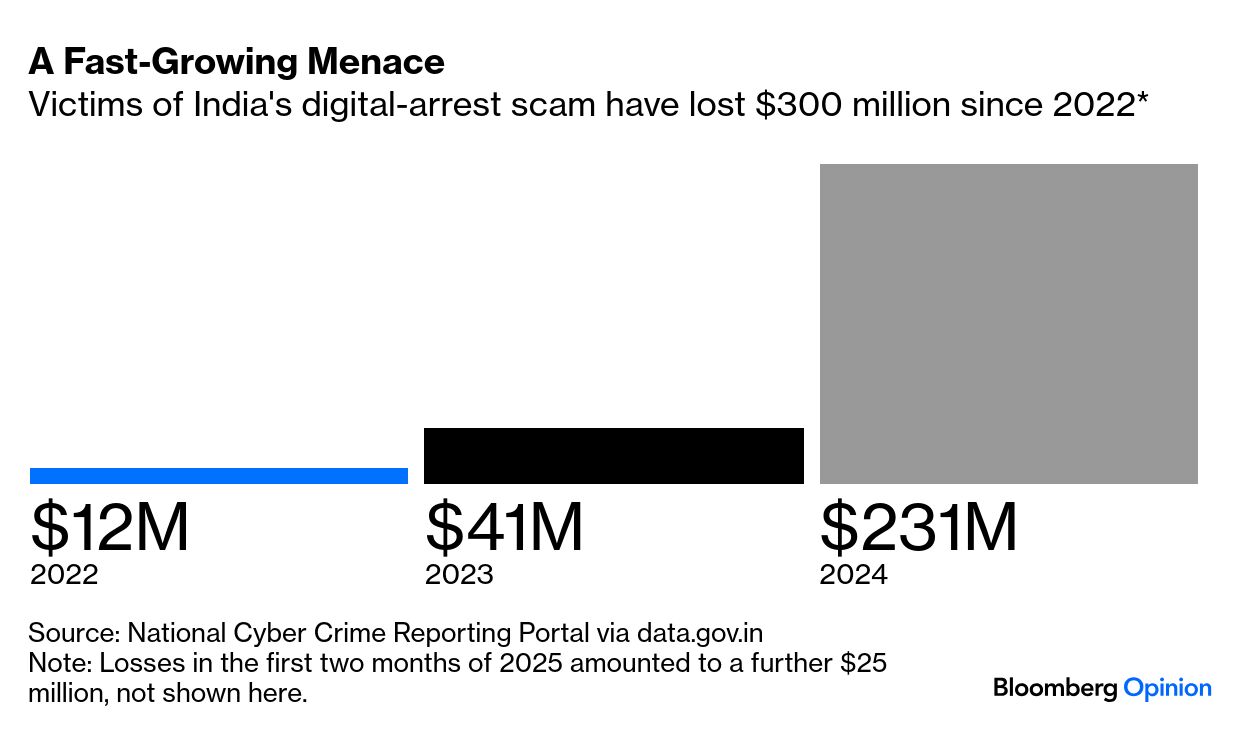

| I’m Justin Fox, and this is Bloomberg Opinion Today, a high return-on-equity portfolio of Bloomberg Opinion’s opinions. Sign up here. After falling sharply on Friday in response to yet another tariff announcement from President Donald Trump, stocks returned this morning to their usual activity — going up. Whether that rebound will continue for the rest of the week is anybody’s guess; John Authers has a rundown of the conflicting short-term drivers. But there’s an underlying force pushing US stocks upward that isn’t dependent on the president’s fickle whims. That would be the investment and profit boom surrounding generative artificial intelligence, which is unlike anything the US economy and markets have seen since, well, the internet boom/bubble of late 1990s. Nir Kaissar examines the contrasts and similarities between the current tech boom and the last one, and comes to two main conclusions. One is that the internet and related technologies that were the subject of all that hype a quarter century ago really did pay off big time for long-term investors, with an investment in the Standard & Poor’s 500 Index at the peak of the dot-com bubble in March 2000 growing sevenfold since then, and an investment in 1995 up 26-fold. The other is that, while the forward price-earnings ratio of the S&P 500 is almost as high now as in 1998 and 1999, by some other important metrics stocks don’t look as frothy as they did then. As shown in the chart, return on equity is higher than in the late 1990s. Debt ratios are much lower. And market expectations of further profit growth are “very achievable” in the medium-term, Nir writes. None of this means stocks will just keep on rising as they have since late 2022. That hypothetical investor in the S&P 500 at its peak in March 2000 was down 24% a year later and 41% three years later, and Nir himself warned a couple of weeks ago that high stock allocations among institutional investors might be signaling a market top now. But he still thinks that “AI is likely to pay off big for long-term investors.” Costs of Trump’s Interventionism | During his first term, President Trump got a lot of credit for unleashing the animal spirits of American entrepreneurs with tax cuts and deregulation. Trump II has featured some more tax cuts and deregulation, but its defining economic theme has been interventionism. Steep and ever-changing tariffs have commanded the most attention, but there’s also been browbeating of companies that aren’t performing as desired, extreme favoritism for some industries over others, a growing appetite for government stakes in corporations and an ongoing campaign to bully the Federal Reserve into lowering interest rates. How’s all that that going? Today’s reports from Bloomberg Opinion columnists aren’t encouraging. With homebuilders currently the target of what seems to be a concerted barrage from Trump and Federal Housing Finance Agency Director Bill Pulte aimed at getting them to build more, Conor Sen points out that Trump’s tariff and immigration policies are making it harder and harder to do that profitably. The administration’s tight embrace of the fossil fuel industry also seems to be doing that industry no favors, with the stock prices of Exxon Mobil Corp. and Chevron Corp. treading water this year. The problem, Mark Gongloff argues, is that “the demand outlook for fossil fuels is poor,” while Trump’s extreme animus against solar and wind power is depriving Americans of needed energy sources. Then there are the equity stakes the administration has taken in three mining companies — “socialism with Trumpian characteristics” is how Liam Denning describes it. Creating economic incentives for miners to extract rare earths and other strategically important minerals in the US makes sense, Liam writes. But by picking favorites through share ownership, the administration may discourage private investment in other miners and reduce the odds of creating the kind of “dynamic ecosystem of competing and collaborating critical minerals producers” that would make the US and the global economy less dependent on Chinese mines. Finally, Alison Schrager warns against something that’s not exactly administration policy now but certainly fits with the president’s rhetoric about interest rates: policies aimed at keeping rates on government securities below their market levels. This sort of “financial repression” can ease government fiscal burdens and also prop up struggling companies, but it also risks creating an ultra-slow-growth “zombie economy” clogged with unprofitable businesses. We’re all familiar with scam calls and texts, but India’s digital-arrest con, in which callers claiming to be from the government and often possessing sensitive personal information threaten affluent retirees with imprisonment and dire consequences unless they stay on the phone and then fork over large sums, seems next-level. In a detailed examination, Andy Mukherjee faults Indian banks for doing far too little to protect their customers from such scams. US stocks have had a good year. Emerging market stocks have done even better, and Marcus Ashworth thinks the time has come to stop calling most of them “emerging.” The term was coined by a World Bank economist in 1981 to replace “Third World,” but since then countries such as China, India and Brazil have emerged in a big way and it’s not clear what purpose the label now serves. How to turn Gaza ceasefire into real peace. — The Editorial Board. New gene therapy brings hearing to the deaf. — Lisa Jarvis America is getting used to broken government. — Abby McCloskey Macron is playing Russian roulette. — Lionel Laurent Pakistan’s power move is saying yes. — Mihir Sharma AI is delivering “workslop.” — Catherine Thorbecke OpenAI keeps doing deals. — Matt Levine The curious timing of Trump’s tariff threats. — Shuli Ren Trump urges leaders to seize Gaza momentum. First Brands CEO resigns. Crypto’s big crash reveals pitfalls. Columbus, Ohio, doesn’t celebrate Columbus Day. SpaceX and xAI buy unsold Cybertrucks. Explaining the economics Nobel. Notes: Please send zombie companies and feedback to Justin Fox at justinfox@bloomberg.net. Sign up here and find us on BlueSky, Tiktok, Instagram, LinkedIn and Threads. |