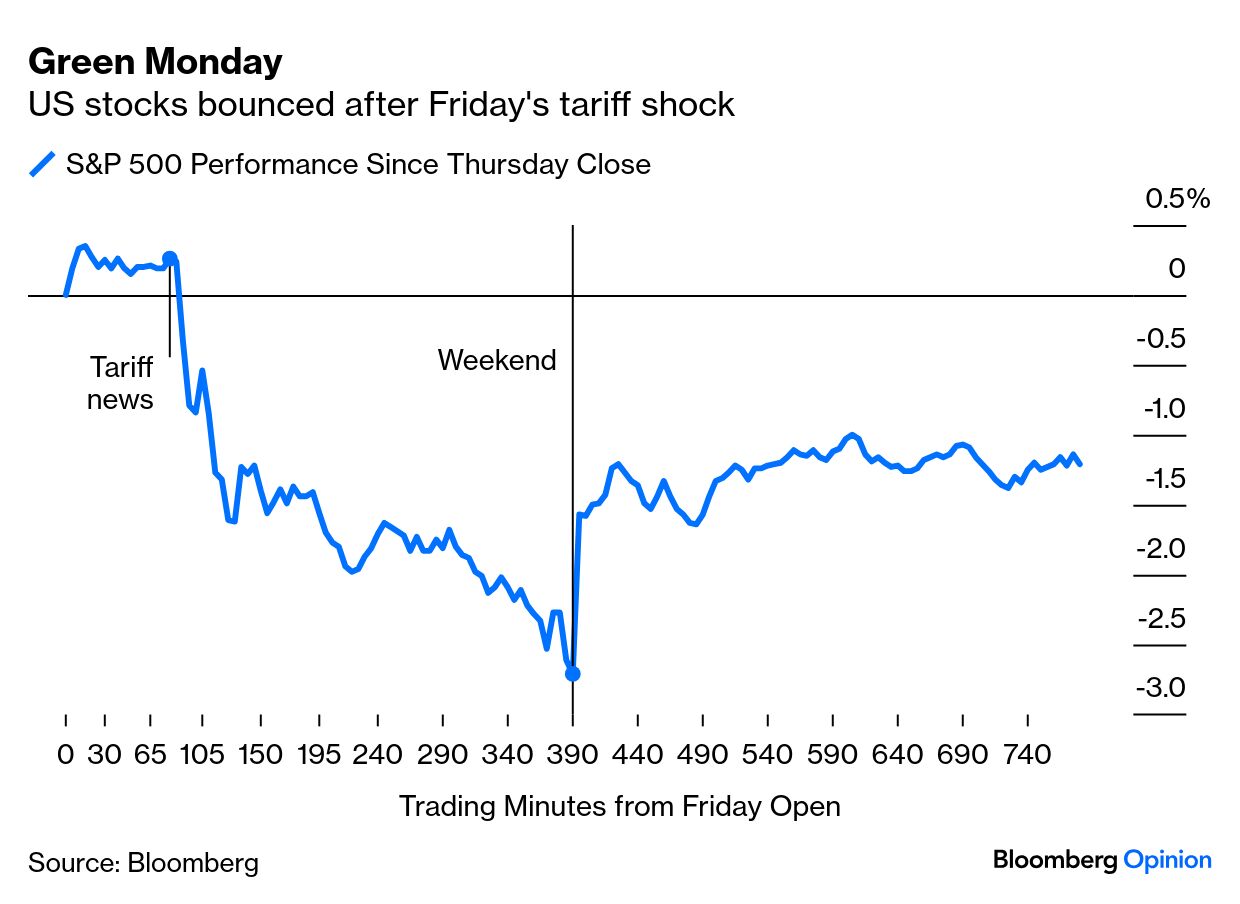

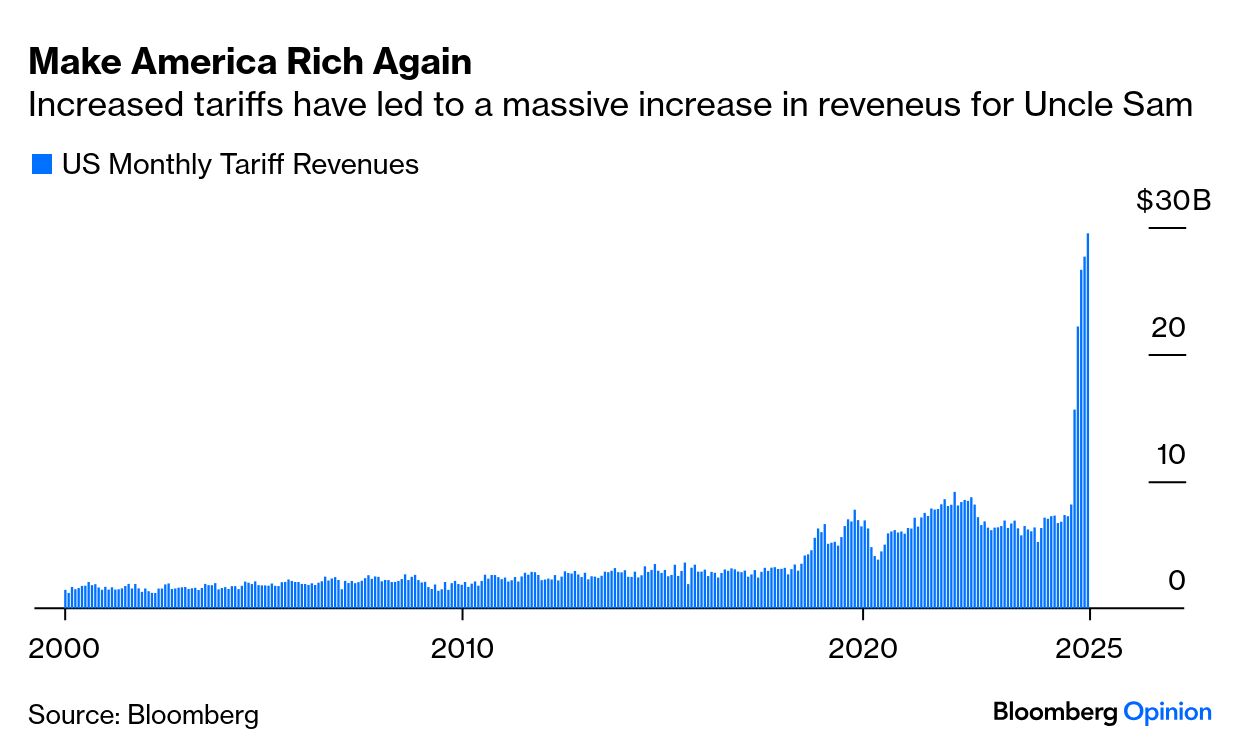

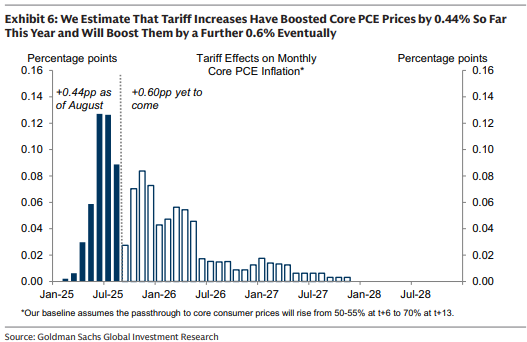

| The panic is over, kind of. Presidential social media postings promising to increase tariffs on China by 100% prompted quite a market selloff. A more emollient tone then spurred a bounce on Monday — although the S&P 500 is still only about half the way back to its level before President Trump made his threat: The bull market is intact (and now three years old). But it’s disconcerting that we still don’t know exactly how high tariffs are going to be in a year — or even in a month. We also have little idea exactly how much impact those tariffs will have on the key economic issue of the age, inflation. Looking back a bit, consumer backlash over soaring prices helped sink William McKinley’s tariffs in the late 19th century. Donald Trump, a fan of McKinley’s, hasn’t faced the same resistance, even as effective tariff rates climb to comparable heights. The difference may say less about economics than political mood. Beyond that, global supply chains are far more complex today, and numerous sectoral carve-outs to avoid causing pain to US businesses make it increasingly difficult to gauge how much of the tariff burden is actually passed through to consumers. The lack of clarity has made policymakers reactive, increasing the risk that when they finally respond it will be too late. For now, what’s clear is that Washington’s attempt to reshape global trade has brought in a record haul in US customs duties, totaling $165 billion for the year as of September. This is a huge success for the America First agenda, and has tended to quieten political opposition: That money is now in government coffers. Who ultimately is going to bear the cost? Josh Hirt of Vanguard says companies have less flexibility to raise prices now than they did immediately after the pandemic. Many are absorbing a portion of tariff costs by narrowing their margins in a calculated attempt to preserve demand and avoid another dose of consumer pushback. But this has limits. Companies will eventually pass tariff costs through to consumers, says Hirt, but this will unfold over time. A recent analysis by Goldman Sachs’ David Mericle suggests consumers will likely shoulder about 55% of tariff costs by year’s end. All else equal, US importers would bear 22% of the burden while foreign counterparts absorb 18% by cutting prices for goods; 5% would be evaded. That implies that core PCE, the Federal Reserve’s favored measure of inflation, which is up 0.44 percentage points already due to tariffs, will rise by a further 0.6 percentage points eventually. As core PCE currently stands at 2.9%, that implies that if nothing else changes, it’s heading for 3.5%, which would be difficult to withstand politically: This burden on consumers starkly contrasts with the administration’s narrative that the levies are penalizing foreign exporters and helping out US taxpayers. But there has been minimal collective pushback to date. Alberto Cavallo of the Harvard Business School Pricing Lab, which tracks the prices of more than 350,000 goods sold by the largest US retailers, has observed a gradual pass-through instead of a one-time, big jump in the level of retail prices: It is a complex pricing decision for the firms. There’s a lot of uncertainty about the levels of those tariffs — whether they’ll be permanent or not, how they will impact each individual firm. And there are a lot of concerns also about how consumers will react. All this is preventing many of the adjustments from happening quickly.

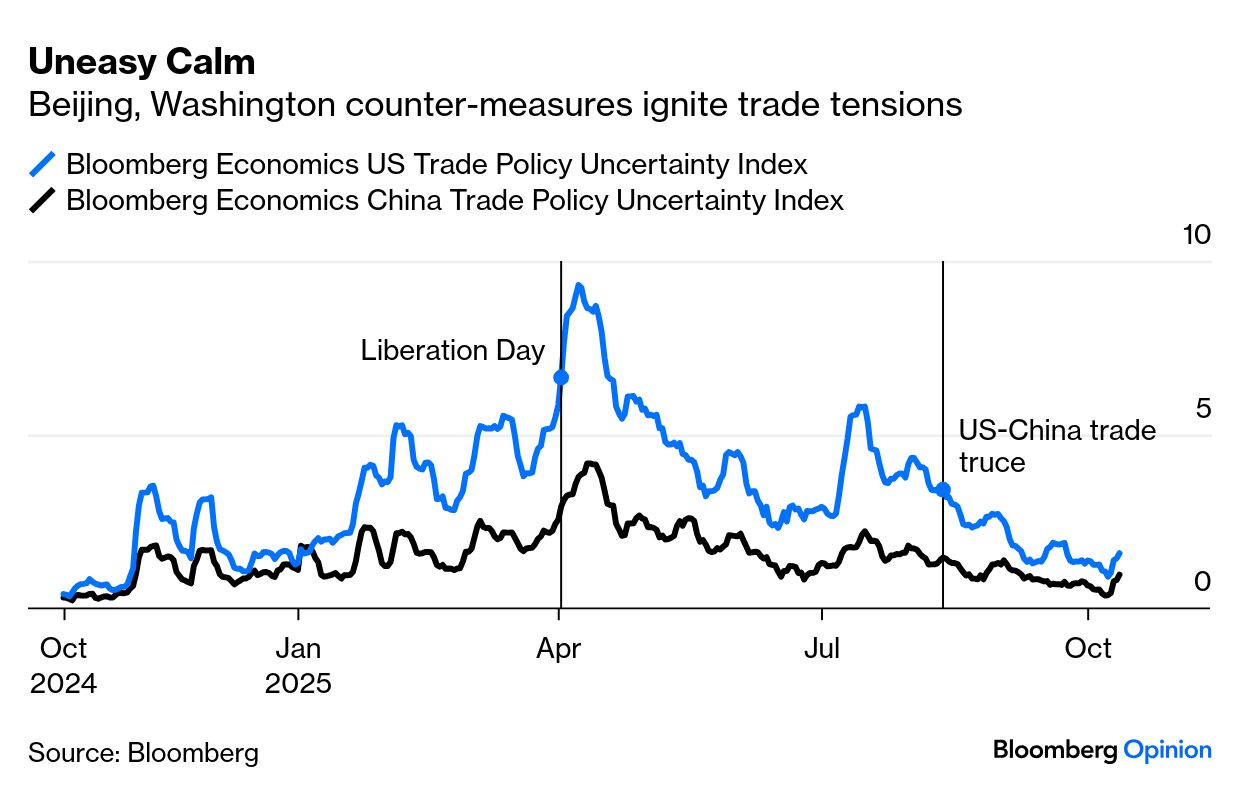

Even though the tariffs announced on Liberation Day in April largely remain intact, markets shrugged them off until last week’s flare-up in tensions between Washington and Beijing. The resulting selloff shows an underlying lack of confidence, but measures of trade uncertainty remain well contained. They’ve ticked up recently, but only slightly: Without a deal with China, it’s reasonable to expect a faster pass-through of tariffs to consumers, according to Harvard’s Pricing Lab. At current tariff levels, Cavallo’s tracker finds the largest price increases concentrated in Chinese goods, like household products and electronics, as China already faces the steepest tariff rates. With tensions escalating, retailers appear more willing to pass along higher costs. For their part, consumers seem so far to accept hikes for Chinese imports as the political case has been made for them: If you look at all the goods that we cover — which is a good representative sample of what you would find if you went to one of these very large retailers — the overall price increases are between 5 percent for imported goods and about 2.5 percent for domestic goods.

Ultimately, American consumers’ resilience comes at a cost, and tariffs will make it even steeper. The Washington–Beijing standoff will test how much pain households are willing to absorb in the name of economic brinkmanship. — Richard Abbey |