|

|

|

|

Oh, hi again. End-of-year inflation numbers are rolling in, and they give us a good idea of what we can expect for increases to programs such as the Canada Pension Plan and Old Age Security. Let’s take a peek at the numbers. |

|

|

|

|

CPP payment increases are likely to slow in 2026 |

|

|

|

|

Any day now, the federal government will announce how much CPP payments will rise by in 2026, but we already have a pretty good idea of what to expect. |

|

|

|

|

CPP payments are adjusted every year based on how much Canadians paid for goods and services, as tracked by Statistics Canada. The 2026 adjustment is based on data from November, 2024, to October, 2025, compared with the year prior. The increase is designed to make sure pension payments align with rising costs. |

|

|

|

|

Jason Yee, the principal financial analyst at Finepoint Solutions Inc. in Saskatoon, estimates that CPP payments will increase by about 2 per cent in 2026 for those already receiving benefits this year. |

|

|

|

|

That’s down from 2.6 per cent in 2025 and 4.4 per cent in 2024, and a sign that inflation is cooling. CPP adjustments are tied to the rate of inflation, so as price growth slows, so do benefit increases. |

|

|

|

|

October’s inflation numbers haven’t been released yet, and that’s the last piece of the puzzle that could nudge the estimate of 2 per cent, but Yee said it’s not likely to change much. |

|

|

|

|

He added that the Bank of Canada’s inflation target is 2 per cent, and that’s around the number many financial planners already use when modelling retirement projections. |

|

|

|

|

Still, even as inflation cools, prices for essentials like groceries and gas remain well above prepandemic levels. That means retirees may be burning through their savings faster than they anticipated, and in some cases, rethinking their retirement plans altogether. |

|

|

|

|

“It’s definitely a known issue,” Yee said. “Inflation for the typical senior looks very different from the [inflation] for broader Canada.” |

|

|

|

|

Some advocates say the way to fix that gap is by rethinking how CPP increases are calculated. One proposal: Adjust the inflation “basket” used to measure costs so it better reflects the expenses seniors actually face, such as the cost of groceries. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

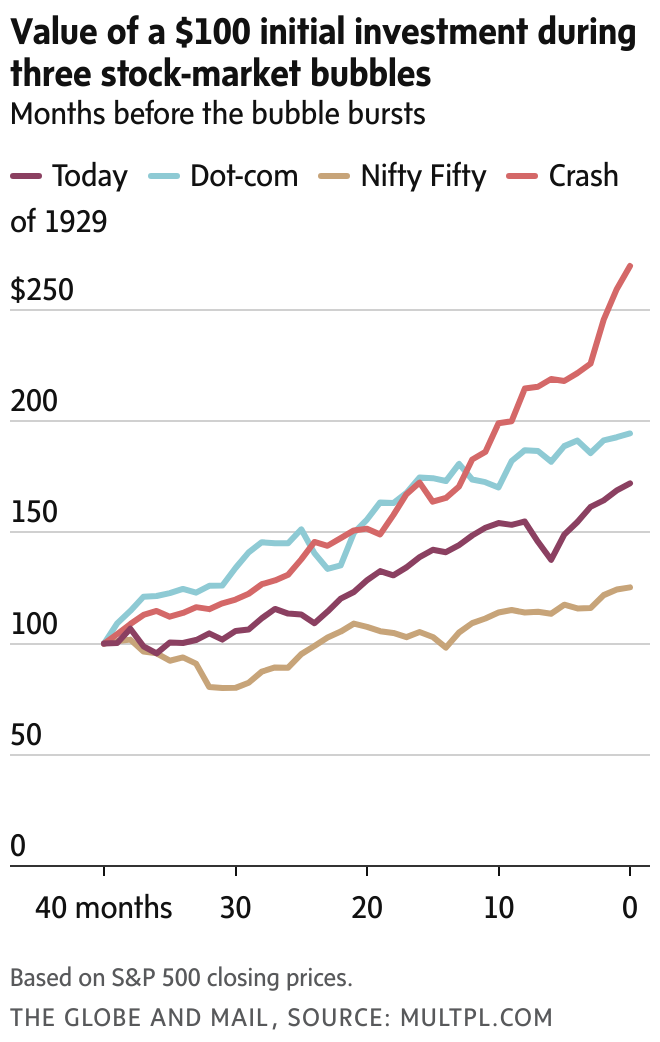

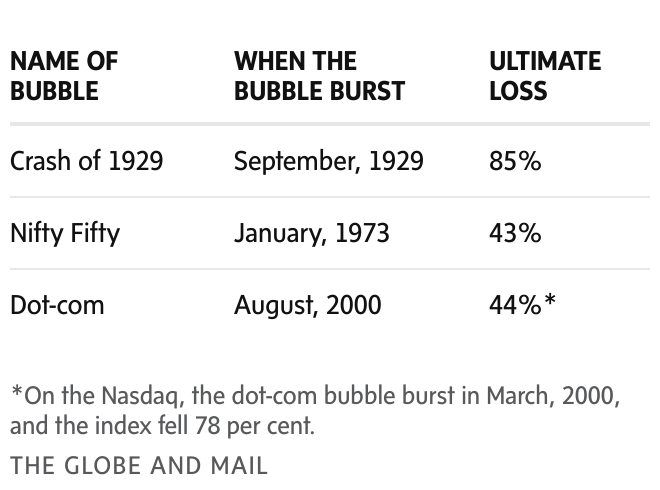

Yes, but: Despite warning signs, Vettese recommends retirees stay invested in equities because the end of the rally might still be a year or two away. He said that retirees can reduce their equity exposure and avoid stocks that have risen the most. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The situation: A consumer proposal reduced her debt from $63,000 to $23,000, an amount she then hustled to pay back over eight months. She is now debt-free and plans to save aggressively for a down payment. She worries about how much she’ll have for retirement but is comforted by the changes she’s already made. |

|

|

|

|

What she’s saying: “I’m one of those elder millennials that was told all my life that I should start saving as soon as you can,” she says. “But you can only control right now, so you might as well be responsible rather than complain about missed time.” |

|

|

|

|

|

|

|

|

|

|

Have you recently received an inheritance, whether it was a financial gift, a family pet or an unexpected heirloom? What did you do with it? Send us an e-mail. |

|

|

|

|

|

|

|

|

|

|

|

|