|

|

|

|

|

|

|

|

|

One in five adults struggles with literacy, leaving many vulnerable to accepting risks and commitments they don't understand. Andrew_Rybalko/iStockPhoto / Getty Images

|

|

|

|

|

Oh, hi again. If you’ve ever stared at a complicated regulatory financial form and felt completely lost, you’re not alone. But knowing what you’re signing is crucial, so let’s break it down today. |

|

|

|

|

Think before signing on the dotted line |

|

|

|

|

Across Canada, financial advisers often hand clients forms full of fine print, but one in five adults struggles with basic literacy. That gap can make it hard to really understand risk, fees or long-term commitments, leaving people vulnerable to mistakes or missed opportunities. |

|

|

|

|

“People don’t always understand the risk side of things, or even the basics of investment accounts,” said Thanuja Sangary, a former CIBC adviser and founder of Sangary Consulting. She’s heard of many clients who sign paperwork without knowing what they were agreeing to, a situation that can put anyone at a disadvantage, and usually isn’t their fault, she said. |

|

|

|

|

Fees can be another surprise. Clients might end up in higher-fee funds without realizing the long-term impact. “A lot of people don’t understand what 2 per cent could mean over 25 years,” Sangary said. |

|

|

|

|

The problem starts long before clients walk into an adviser’s office. Mélanie Valcin, CEO of the national literacy group United for Literacy, says about 20 per cent of Canadian adults fall into the two lowest literacy levels, making financial documents even harder to navigate. |

|

|

|

|

Sangary advises clients to do their own research prior to having conversations with an adviser and to come up with questions to ask them. This can include inquiring about how they choose different funds and what their investment philosophy is. Even a little advance prep can give you a big confidence boost, which can empower you to understand what you’re signing, she said. |

|

|

|

|

“When you’re picking an adviser, make sure they can explain these concepts to you without talking down to you, because if your adviser is not explaining these things in a way that’s understandable, just don’t go with that adviser,” she said. |

|

|

|

|

Subscribe to the Retire Rich newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for Retire Rich here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

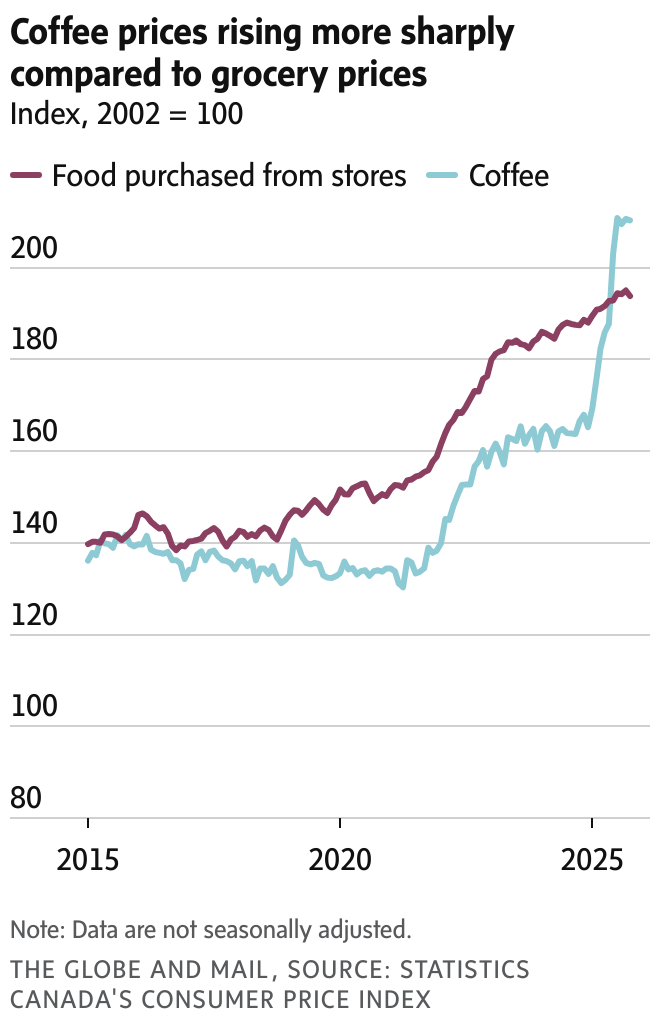

What’s happening: Coffee prices have jumped 26.3 per cent over the past year, compared with a 3.4-per-cent rise for overall groceries, according to Statistics Canada. Over six years, prices have soared 59 per cent. |

|

|

|

|

What they’re saying: “When supply goes down, prices go up. That’s basic economics 101,” says Michael von Massow, a food, agriculture and resource economics professor at the University of Guelph. Poor harvests in Brazil and Vietnam, extreme weather, crop disease and U.S. tariffs are all pushing costs higher, as Canadians keep buying coffee. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Todd Korol/The Globe and Mail

|

|

|

|

|

|

|

|

|

|

|

The numbers: The couple has a mortgage-free home in Alberta and $3.5-million in combined assets, including $500,000 in a corporate account, $1.4-million in RRSPs, and $220,000 in TFSAs. Their goal is to maintain a standard of living of about $94,000 a year, adjusted for inflation. |

|

|

|

|

The situation: Vince and Mindy want to wind down their corporate account without triggering unnecessary taxes or Old Age Security clawbacks. They’re also balancing registered accounts and planning when to start government benefits. |

|

|

|

|

Key steps, from a financial planner: The plan calls for deferring Canada Pension Plan and OAS benefits to age 70, drawing $100,000 a year from the corporate account until it’s gone, and unlocking Vince’s locked-in retirement account, splitting it between his RRSP and a life income fund for withdrawals. Registered accounts are drawn strategically to keep taxes low, and a balanced investment approach helps cover expenses during market downturns. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|