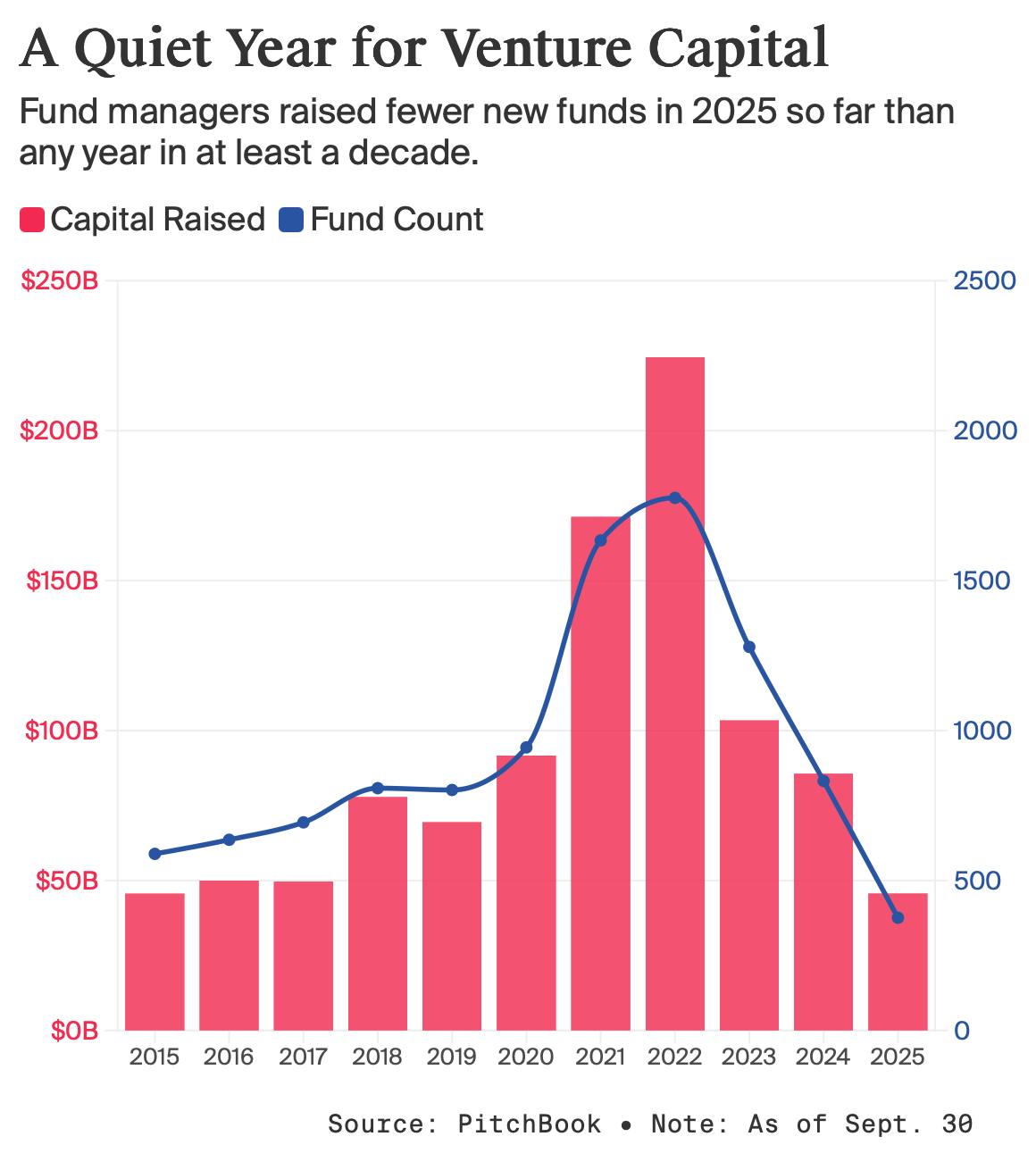

The sky’s the limit for valuations for companies like SpaceX, but the venture firms writing the checks have less money in total to spend. Recent data from PitchBook shows how steep the decline in cash is. Fund managers raised $45.7 billion in new funds in the first nine months of the year. At that pace, fundraising is headed for the lowest level since 2017. The number of new funds, meanwhile, is on track to be the lowest in at least a decade. There were just 376 new funds in the first nine months of the year, less than half of the 832 for all of last year and a steep drop from the 1,776 funds launched in 2022.

The sky’s the limit for valuations for companies like SpaceX, but the venture firms writing the checks have less money in total to spend.

Recent data from PitchBook shows how steep the decline in cash is. Fund managers raised $45.7 billion in new funds in the first nine months of the year. At that pace, fundraising is headed for the lowest level since 2017.

The number of new funds, meanwhile, is on track to be the lowest in at least a decade. There were just 376 new funds in the first nine months of the year, less than half of the 832 for all of last year and a steep drop from the 1,776 funds launched in 2022.

It isn’t necessarily shocking that the limited partners in VC funds are growing skittish. The majority of venture funds formed between 2017 and 2024 had yet to see a single public listing or sale, portfolio management company Carta said earlier this year. The timing of these funds meant that they largely missed the 2021 liquidity boom, with startups too young to make money in that banner IPO year.

Last year, VC funds recovered after two years of negative returns in aggregate, according to a report by Cambridge Associates. “While the last year has been one of recovery for the private markets, the aftershocks of the 2021 era continue to reverberate,” said Cambridge, predicting that the “distribution drought” and “fundraising slowdown” to continue into 2026.

This hasn’t stopped new firms from entering the picture. For example, comms guru Lulu Cheng Meservey recently raised $40 million to launch her first venture fund. Max Gazor recently left CRV to start a new firm, Striker Venture Partners.

Despite challenges, we are seeing some large new funds form, particularly those that had exits in recent years. Andreessen Horowitz is in the process of raising over $10 billion in new funds and Tiger Global Management is raising more than $2 billion.

What’s more, there has been a rebound in acquisitions this year. Tech mergers are on track for their biggest year since 2021.

Initial public offerings are slowly coming back. In fact, as I reported Friday, SpaceX is working toward a listing in the second half of next year. But there won’t likely be enough money returned from IPOs to satisfy VC funds’ backers. I expect venture funds to continue to rely on so-called secondaries, or the sale of existing shares, to return cash to their investors.

Cambridge notes that fewer than 5% of private market activity comes from secondaries, which leaves a lot of room for expansion.