Major U.S. equity indexes fell on Wednesday, as investors sought to rotate from frothy growth names into value. This was driven largely by declines in the “Mag Seven,” which were hit in part by Trump's announcement of a 25% tariff on some chip imports. Bank shares also dropped, as the industry has had a disappointing start to the earnings season this week.

Ultimately, the main trend we’re seeing is a new year sector rotation. Even though high-flying tech dialed back yesterday, U.S. small caps continued to push ahead. What seems clear is that investors want to remain invested and have just become a bit choosier as to where they’re putting their money.

The selloff extended into Asia trading on Thursday, with Japan’s Nikkei easing 0.9% after reaching an all-time high on Wednesday, as investors reduced exposure to chip and artificial intelligence-related stocks.

Yet the promise of AI remains strong, as chipmaking juggernaut TSMC posted blockbuster results on Thursday, including a 35% rise in fourth-quarter profit to a record high. Invoking what it called the “AI mega trend”, the chipmaker said it expects a nearly 30% rise in revenue in 2026. This comes as it looks set to boost investment in the U.S. in return for an apparent reduction in tariff rates to 15% from 20%.

The other major moves this morning were the declines in oil and gold prices after President Trump said he had been informed that Tehran’s killing of demonstrators was subsiding and that no plans were in place for executions.

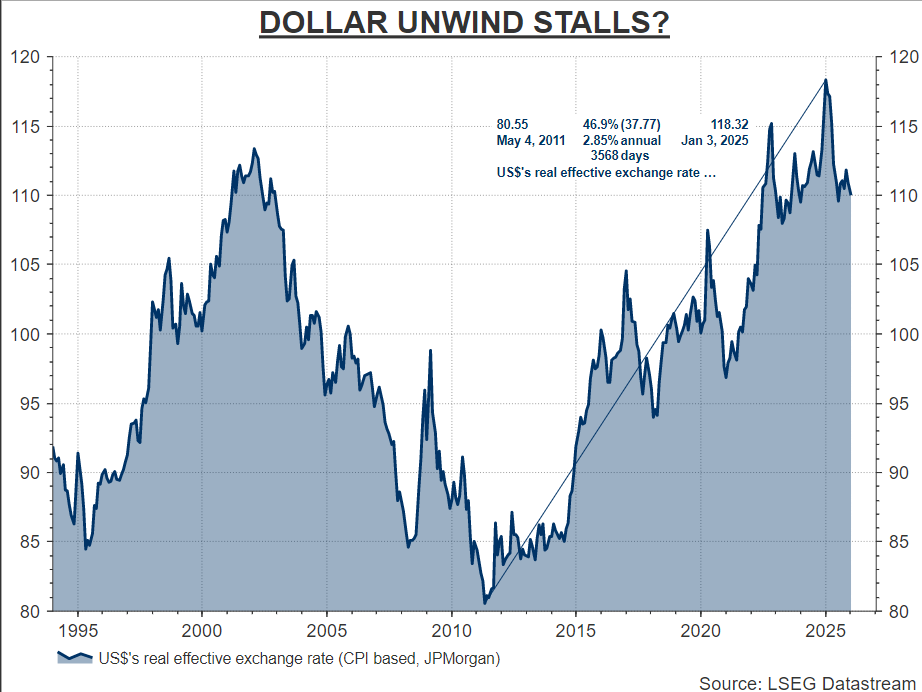

The dollar index steadied against major peers on Thursday, as Trump stated in a Reuters interview that he had no plans to fire Fed Chair Jerome Powell, days after his administration announced a criminal probe into the Fed Chair that drew broad condemnation. The recent slew of fairly healthy U.S. economic data has solidified expectations that the Fed will hold rates steady this month, though markets still expect two cuts this year, likely after Powell’s term ends in May.

Whether today's apparent lull in safe-haven demand will have any staying power is an open question. Trump appears to be in wait-and-see mode concerning Iran, having still not ruled out the possibility of military action, his administration’s probe into Powell remains live, and global geopolitics are still fractious as the Trump administration refuses to backdown from its claim that it will acquire Greenland.

Meanwhile, the Japanese yen also stabilized after falling to its weakest point against the U.S. dollar since July 2024 overnight. It recovered some of that ground amid warnings of possible bond-buying intervention by Japanese authorities.

Japanese bond yields have also eased after reaching record peaks on speculation - which has now been confirmed - that Prime Minister Sanae Takaichi, who has supported massive fiscal stimulus, will call snap elections.