| | In this edition, parsing what’s real versus systemic in the latest market concerns, and what corpora͏ ͏ ͏ ͏ ͏ ͏ |

| |  | Business |  |

| |

|

- Tariff war games

- SOTU listening guide

- Meta’s chips buffet

- Paramount’s back in the game

- Chinese EVs can save the US

|

|

Markets are unsettled this week by two things: one real but not systemic, the other systemic but not real. I wasn’t two steps into Bill Gurley’s book launch last night in New York when I overheard “Blue Owl” and “Citrini” from a group of men wearing classic Midtown investor uniforms. At a time when so many people are on edge, it’s natural that investors are trying to make connections to fit their feelings. The ongoing problems at Blue Owl Capital, where retail investors are rushing for the exits from a handful of private-credit funds, are real. But I don’t think it will become a spillover event, or a fatal one for Blue Owl, which embodies the fast growth of the private-credit industry but not its loosest lending standards. A similar hiccup at Blackstone three years ago was contained by dropping the gate on fleeing investors and selling some choice assets at decent prices, something Blue Owl did last week. The industry continued its growth, and the race for assets is still one. Someone will catch any knife that drops; the blast radius will expand, a little, but lose intensity. The other market rattler this week was a 7,000-word AI doomsday scenario that is systemic but not real. The financial danger of AI, as laid out by a little-known research firm, isn’t whether hyperscalers are overspending or software gets leapfrogged by vibe-coders, but rather a world where nobody can afford to buy anything. The essay was entirely fictional and, plenty of economists noted, overly simplistic. We have a clearer sense of what jobs AI will replace than the ones it will create, and we’re modeling outcomes without considering what governments and businesses would do midstream to change those trajectories. (Policymakers wouldn’t sit on their hands while consumer demand went to zero, and if they need encouragement, Jamie Dimon says he’ll be pushing them.) The two events are connected — Citrini’s bear case involves a “daisy chain of correlated bets,” including a lot of private credit loans to software companies — but only loosely. People looking for proof points to justify a general malaise will find them, and the fast-moving frontiers of both technology and finance leave investors looking to backfill their jumbled feelings. |

|

FedEx wants its tariff refunds back |

Benoit Tessier/File Photo/Reuters Benoit Tessier/File Photo/ReutersFedEx was the first major US company to sue for a tariff refund after the Supreme Court invalidated much of President Donald Trump’s signature economy policy, an early sign that importers are going to demand their money back even if they risk political blowback from a White House that wants to keep it. The shipping giant joins earlier litigants including Costco in seeking a repayment. The White House is fighting refunds, with Treasury Secretary Scott Bessent framing them as “the ultimate corporate welfare,” and reintroducing a new 10% tariff effective today, which could rise to 15% once the paperwork goes through. The result is renewed uncertainty, but companies are better prepared this time, Marc Gilbert, who runs the Boston Consulting Group’s Center for Geopolitics, tells Semafor. Dumbstruck and flat-footed on “Liberation Day,” executives now know “if not exactly what to do, where to look, and what questions to ask.” One key question that’s new in Gilbert’s meetings since Friday: “How can I benefit from this?” When Trump’s tariffs forced companies to scramble last year, what emerged was a diverse set of playbooks. Companies that were slower to shift away from China, whose tariff rate falls from 36% to 27% (for now, according to BCG’s calculations), are better off. Those with spare trade credit can frontload shipments. A trench mentality of “what just happened to all of us?” has shifted to “am I harder hit than my competition?” Gilbert said. |

|

Wall Street’s SOTU checklist |

Kevin Lamarque/File Photo/Reuters Kevin Lamarque/File Photo/ReutersTrump has promised “a long speech” for tonight’s State of the Union. Here’s a cheat sheet for the business world. - Affordability: Trump’s series of populist pronouncements haven’t turned into firm policies. More details on credit-card interest rate caps, a ban on institutional investors owning homes, or more direct stimulus measures are high on Wall Street’s watch list.

- Tariff body language: An all-out attack on the Supreme Court justices in attendance will likely reveal a Trump determined to rebuild the most robust version of his tariff policy. It could also portend a tough fight over refunds, if the high court decides they are warranted.

- Retirement free-for-all: The White House is considering an expansion of its kids’ retirement accounts to adults, Semafor’s Eleanor Mueller scoops. The move would sweeten an asset-management mandate that firms including Charles Schwab, State Street, Robinhood, are talking to Treasury about.

- Fed talk: Will Trump take the off-ramp floated by Bessent to wind down an investigation of Fed Chair Jerome Powell and clear the way to confirmation hearings for his nominee, Kevin Warsh?

- A grand unified theory of AI: Will we see a clear push for federal, rather than state regulation? We’re also looking for a formal Pentagon procurement plan, or, just spitballing here, a government financial backstop.

|

|

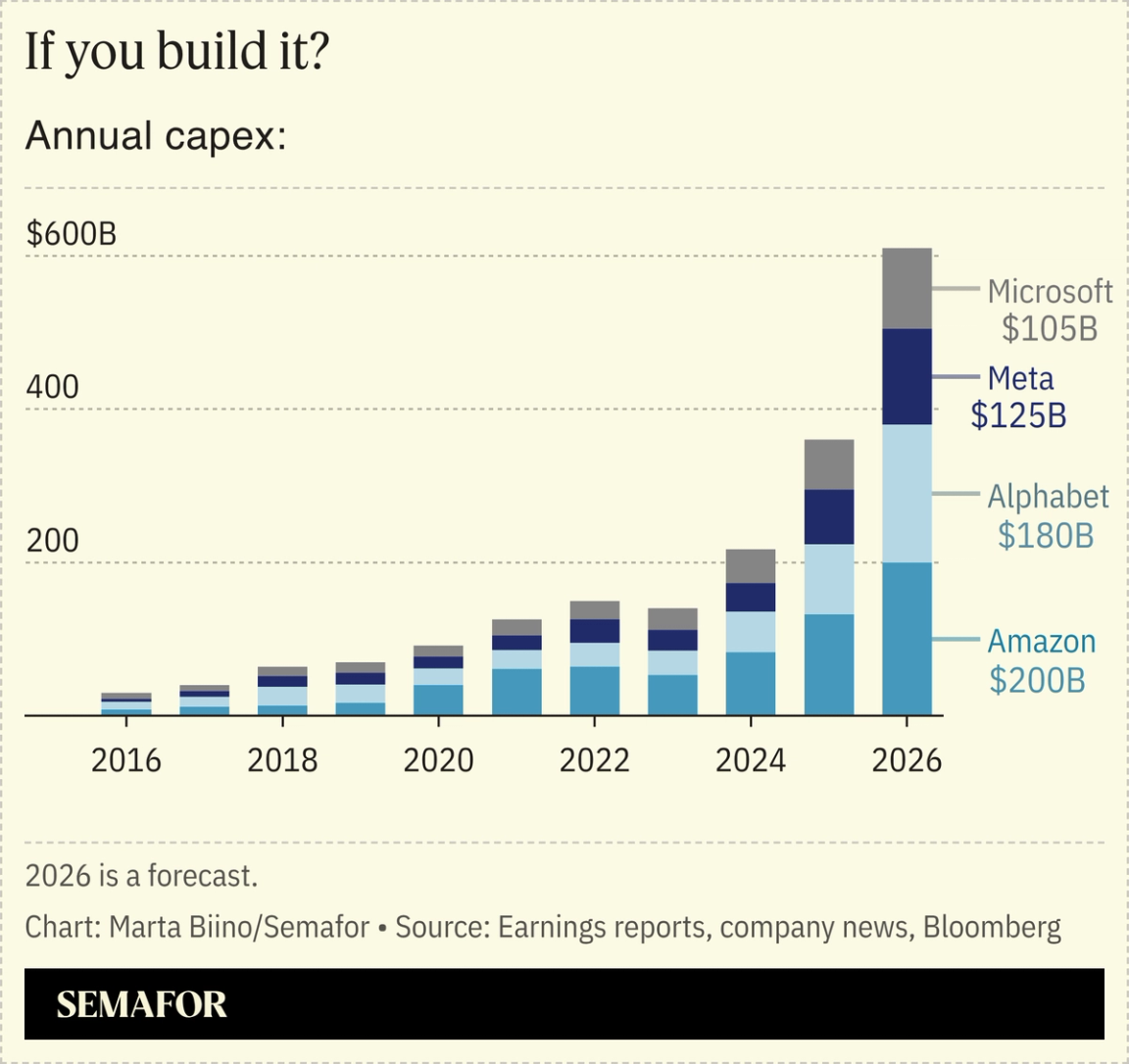

Meta spreads its chip bets |

Meta investors gave the tech giant the green light to spend like crazy on AI, and CEO Mark Zuckerberg is taking advantage. A week after striking a deal to buy tens of billions of dollars’ worth of Nvidia chips, Meta announced a fresh partnership with AMD that would give Meta a stake in the chipmaker in exchange for a pile of chips big enough, in energy-consumption terms, to power 4.5 million homes. The deal is nearly identical to one AMD struck last year with OpenAI, and shows AMD using the potential appreciation of its stock as bait to land big chip customers. Meta can buy up to 10% of AMD — for a penny a share — as AMD fulfills its chip orders. It’s the latest bit of circular financial engineering that tethers the contestants in the AI race to each other. — Rohan Goswami |

|

We are ramping up our global coverage: We’ve just launched Semafor China, an ambitious briefing for leaders on how the world’s second-biggest economy is changing the world around it. Helmed by Andy Browne — a Pulitzer Prize-winning reporter and editor who has covered the country for decades — and featuring a new CEO interview series by Clay Chandler, a decorated Asia-focused journalist who has covered the region for The Wall Street Journal, Washington Post, and Fortune, our weekly briefing will tackle the vast financial, economic, and technological impact China is having across the globe, from Africa to the Americas. Our inaugural edition had scoops on a Chinese industrial giant’s expansion into Europe, AstraZeneca’s strategy in China, and the extent of US allies’ courting of Beijing over the first year of US President Donald Trump’s second term. Subscribe to Semafor China for your weekly look at the biggest stories and best analysis on the country, and its huge impact on the world. |

|

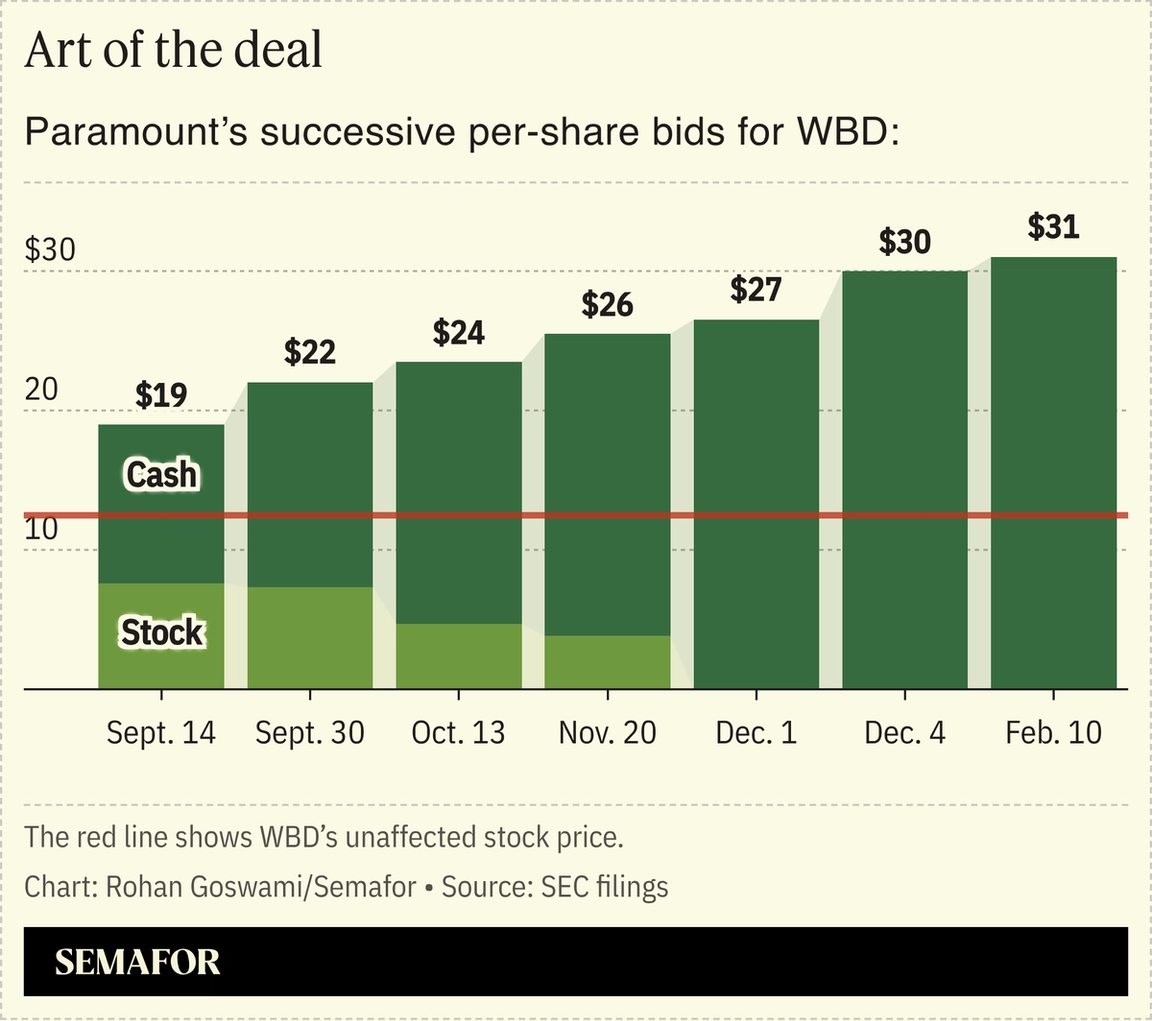

Paramount is back in the game. David Ellison’s new bid for Warner Bros. Discovery — at what Semafor hears is above the $31 starting point — puts the media scion back in the running for a company that should have been his from the start. It also puts Netflix on the defensive, forcing it to either bump or defend its more complicated agreement to buy Warner and its franchise-rich library. Ted Sarandos can afford the price, but the politics are closing in. Trump has taken direct aim at a Netflix board member who said Democrats would look to punish companies that kowtowed to Trump once they took power again. Sarandos went on the BBC — which is itself being sued by Trump — to dismiss the president’s comments as social-media noise. “This is a business deal, it’s not a political deal,” the Netflix co-CEO said. But everything is political these days: The president is keen to see Warner-owned CNN neutered. Senate Republicans want to see Netflix humbled. Senate Democrats want to make Ellison the face of influence-peddling in Trump’s Washington. And state attorneys general are worried about anticompetitive effects and job losses. The growing political noise raises questions about whether Netflix, which has had one of the cleanest business strategies and investment stories in media, blundered into its first big M&A swing. — Rohan Goswami |

|

View: Detroit’s EV ‘salvation’ lies in China |

Rafael Martins/File Photo/Reuters Rafael Martins/File Photo/ReutersUS restrictions on Chinese EVs are misguided and, in fact, the vehicles’ entry into the American market could offer a salvation for Detroit’s automakers, Semafor’s China columnist Andy Browne argues. Wary of the security risks Chinese internet-connected cars might pose, and of howling in Detroit, Trump has maintained sky-high tariffs on EV imports. Solar panels, drones, and surveillance cameras have all met a similar fate. The problem, Andy writes, is that Chinese EVs are cheaper and often better and the secret is already out. To compete with cars like the Xiaomi SU7 Max, Detroit will have to learn from Chinese carmakers. Keeping out Chinese players risks American firms languishing, failing to innovate against the products that are setting the standard worldwide, and closer to home in Canada, where Chinese EVs are now starting to be sold. There is some prospect of a shift on the horizon. Ahead of a meeting with Chinese leader Xi Jinping in Beijing in April, Trump said he’d “love” to see Chinese carmakers opening factories and creating jobs in the US. |

|

➚ BUY: Soda. Keurig Dr Pepper’s strong earnings results provided at least a temporary corrective to the idea that GLP-1s are sapping Americans’ bubbly habit. Watch Coca-Cola’s bet on smaller serving sizes. ➘ SELL: Pop. Universal, Sony, and Warner have lost more than $9 billion in market value since Google introduced AI music generation to Gemini last week. |

|

Companies & Deals- Not wrong, just early: Six years after its attempt to build a cryptocurrency flopped, Meta is trying again, this time with stablecoin adoption and Washington on its side, Coindesk reports.

- Read ’em and reap: Political candidates are now pasting screenshots of their betting odds in their fundraising emails.

- Good to go: Data center developers are seeking credit ratings from Moody’s and others long before they’re finished, suggesting they are hitting the limits of private investors willing to forgo Wall Street’s CYA seal of approval.

Watchdogs- Tête-à-tête: Anthropic’s CEO meets today with Defense Secretary Pete Hegseth to discuss tensions over how the Pentagon uses its AI, which has spiraled into a major feud.

Markets- Downsizing: Novo Nordisk, losing the battle to develop the next generation of weight-loss drugs, is turning to price cuts on the ones it has.

|

|

|