|

|

|

|

Good morning. U.S. President Donald Trump says he has agreed to suspend attacking Iran “for a period of two weeks.” In focus today, we look at the forces that might have guided his last-minute pullback after he warned that “a whole civilization will die.” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade: The White House’s top trade official said he expects the core of the United States-Mexico-Canada Agreement to remain in place, referring to “a bunch of load-bearing pillars” in the pact that will form the basis for two side deals with Canada and Mexico. |

|

|

|

|

Travel: Air Canada is trying out a new way to resolve claims for compensation filed by unhappy passengers by using third-party arbitrators, a test project intended to avoid long waits for decisions from the Canadian Transportation Agency. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A customer fills up his vehicle at a gas station in Miami, where gas prices have risen to more than US$4 a gallon. Joe Raedle/Getty Images

|

|

|

|

|

|

|

|

|

|

|

How the U.S. found an off-ramp |

|

|

|

|

Donald Trump pulled over. |

|

|

|

|

After issuing a warning that “a whole civilization will die” if Tehran did not strike a deal to reopen the Strait of Hormuz by 8 p.m. ET, the U.S. President agreed to suspend the bombing of Iran for two weeks while he negotiates a truce proposal from mediators in the Iran war. |

|

|

|

|

|

|

|

|

Still, on a day that saw the U.S. and Israel strike Iranian railways, an airport, and targets on Kharg Island − home to Iran’s main oil export terminal

− the ceasefire was a reminder of how exposed the Persian Gulf’s critical infrastructure remains. The nature of the attacks, and the targets under threat, drew shock and condemnation worldwide but little in the way of real resistance. |

|

|

|

|

Earlier, Iran said it would plunge Gulf states – including Saudi Arabia – into darkness, attacking major infrastructure such as water desalination plants and energy sources that keep desert cities habitable. For those regions, which count on energy production and trade as economic drivers, attacks on key infrastructure would be devastating, and could shift spending from oil-rich countries toward rebuilding rather than foreign investment. |

|

|

|

|

But the scale of Trump’s threats, which have a habit of being dusted off for fresh reprisals,

amounted to such a colossal disruption to the global economy that most of the world’s population – including the U.S. – would immediately see a sharp spike in oil prices, which would quickly spill into stocks, bonds and inflation expectations. That might explain why markets moved mostly sideways yesterday. “There is belief that the President will not want to cause serious market disruption,” said Douglas Porter, chief economist at Bank of Montreal. |

|

|

|

|

Perhaps owing to the scale of those threats, in other words, no one believed him. Stocks and bonds are often Trump’s tipping point on major threats to the world order. But oil puts pressure on shipping, food and all sorts of things that could upset American voters. |

|

|

|

|

The markets: Financial markets “are one of the constraints” on the President’s actions, Porter said in an e-mail. Bond yields – a key signal of investor stress – have preceded some of Trump’s most notable challenges to the global order, including his recent threat at a NATO summit to annex Greenland. Yields would likely spike in the short term under an escalated oil shock, Porter said, and “another dramatic run‑up in oil prices could quickly spill into stocks and bonds,” before longer‑term growth worries begin to temper the move. |

|

|

|

|

Today, markets might imagine the ceasefire is a sign of happier times over a longer horizon. News that Trump had spotted an off-ramp from war, even if it’s for a temporary pit stop, sent the price of U.S. crude oil down more than 15 per cent to US$95 a barrel, after trading north of US$117 earlier in the day. |

|

|

|

|

Shipping, fertilizer, food: Even limited escalation would send higher oil prices racing through the global economy, pushing up the cost of moving goods, producing food and setting interest rates. |

|

|

|

|

At the top of the supply chain, oil price spikes feed into higher transportation costs. In wholesale diesel markets – the fuel that powers trucks, trains, cargo ships and heavy machinery – those increases quickly raise the cost of moving goods across supply chains, well before consumers see it at the pump. |

|

|

|

|

Shipping costs were already climbing as insurers raised war‑risk premiums in and around the Gulf, with risk zones expanding into the Red Sea and nearby corridors. Higher insurance costs, longer routes and tighter vessel availability raise freight prices worldwide. For Canadian businesses and consumers, that translates into higher prices for imported goods, pressure on airfares as jet fuel costs rise, and longer delivery times. |

|

|

|

|

Those dynamics already put pressure on the cost of anything that needs to move. But higher energy prices force food prices even higher. Because fertilizer depends heavily on natural gas before it even gets loaded into diesel-powered vehicles, higher production costs are passed along to grocery bills through more expensive grains, meats and packaged foods. |

|

|

|

|

Longer term: Together, higher transport and food costs are what turn an oil shock into a sustained inflation problem. That complicates decisions for central banks, which often try to look past geopolitical shocks on the assumption they will fade quickly. |

|

|

|

|

But energy‑driven price spikes have a record of lasting longer than conflicts themselves. The Bank of Canada is among the institutions warning that an energy shock from a wider Iran war would lift inflation in the near term, particularly in food and transportation. |

|

|

|

|

Some economists still expect the U.S. Federal Reserve to cut interest rates later this year, while the Bank of Canada is seen as more likely to remain on hold. A prolonged rise in oil prices, however, would narrow the path to rate relief – even as higher costs weigh on economic growth. Trump, who has repeatedly demanded the Fed cut rates further and faster, hasn’t been helping his case. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

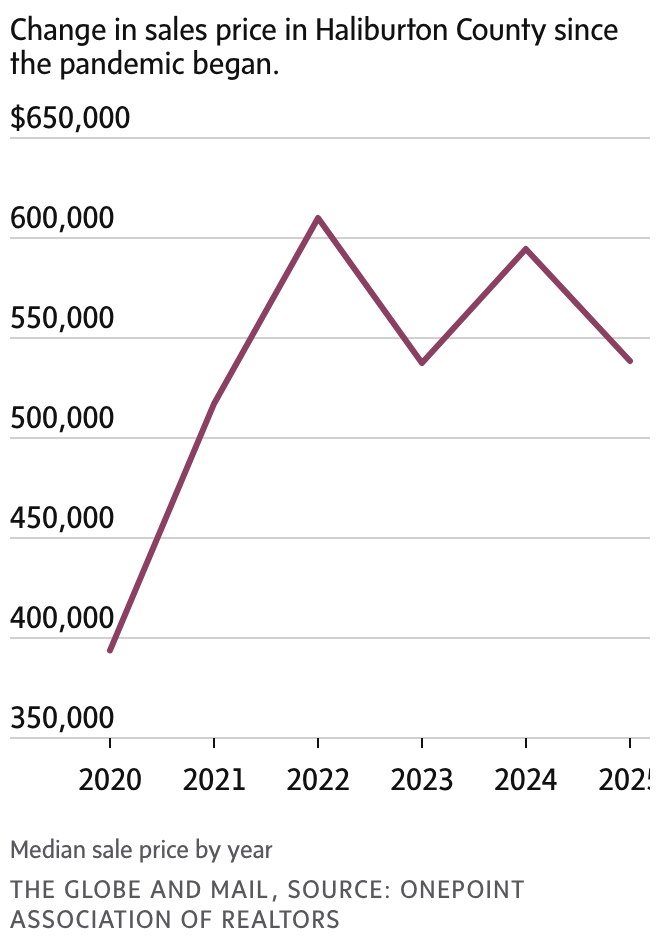

Let’s just think about cottages now |

|

|

|

|

|

|

The cottage market in Ontario could finally be stabilizing after a period of volatility since the onset of the pandemic, in which prices jumped and then dropped by more than 30 per cent in some areas. But some realtors say a continuing wave of mortgage renewals to higher rates could drive owners to sell and |