| | In today’s edition: Ceasefire deal sends oil price down and regional bourses up, and Türkiye sees ec͏ ͏ ͏ ͏ ͏ ͏ |

| |  Islamabad Islamabad |  Riyadh Riyadh |  Istanbul Istanbul |

| Gulf |  |

| |

|

- Iran war ceasefire agreed

- Markets react with relief

- Gulf gatherings at risk

- Erdogan touts financial hub

- A moment for truckers

- Gulf employment push

An underwater theme park ride on the outskirts of Riyadh. |

|

Ceasefire prompts relief, and doubts |

Majid Asgaripour/WANA via Reuters Majid Asgaripour/WANA via ReutersUS President Donald Trump backed down from his threats against Iran with the two sides agreeing to a temporary ceasefire. Talks on a longer-term deal are scheduled for Friday in Pakistan. Both sides have claimed victory, as has the UAE. While the pause will be a relief to everyone after weeks of escalation, there are myriad reasons for caution. Trump said a 10-point Iranian proposal was “a workable basis on which to negotiate” but it contains elements likely to be rejected by Washington and its allies, including Iranian control of the Strait of Hormuz and the withdrawal of US forces from the region. There are other problems too: Pakistan’s Prime Minister Shehbaz Sharif said the deal applied everywhere “including Lebanon,” but Israel swiftly, and publicly, contradicted that point. And Gulf nations including Bahrain, Kuwait, and the UAE said on Wednesday that they were still intercepting Iranian attacks. Ahead of the Friday talks, Iran’s Supreme National Security Council said it had “complete distrust” of the US — understandable, given Trump has twice before bombed Iran in the middle of negotiations. The difference now is Iran has shown how easily it can close the Strait of Hormuz and damage the global economy. — Dominic Dudley |

|

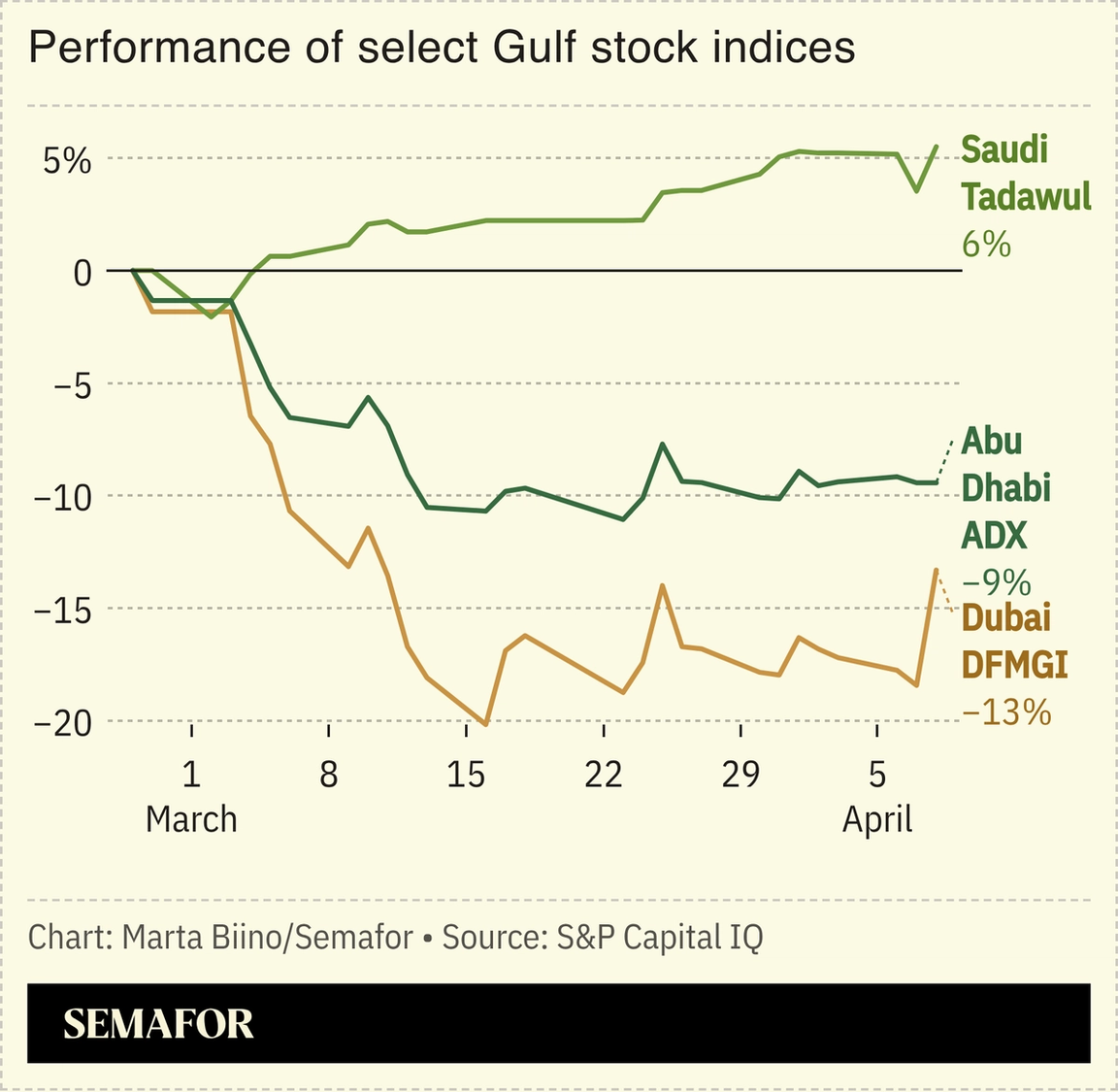

Gulf stocks surge, oil falls |

Gulf stocks surged along with global markets and oil fell below $100 a barrel as investors digested the news of the two-week ceasefire. Dubai’s benchmark index rose more than 6% as real estate stocks rebounded and Abu Dhabi’s was up around 3% on Wednesday, although both markets are still lower than before the war started. Other regional bourses jumped on optimism about an end to Iranian attacks on the region that have caused significant damage to infrastructure and disruption to business activity. Saudi Arabia’s main index is the one regional exchange that has posted gains since the conflict began and was up a further 1.8% on Wednesday. The kingdom has not suffered the same level of disruptions from Iranian attacks as its neighbors and has used its Red Sea ports to boost its role in regional supply chains disrupted by the closure of the Strait of Hormuz. As of early afternoon Gulf time on Wednesday, there were no signs of more traffic heading for the strait and large shipping companies remained cautious. The ceasefire is also a positive for airlines and all the other sectors damaged by the war but, even if it holds, a full recovery could take months, if not years. — Matthew Martin |

|

Gulf conferences in limbo |

The 2024 Qatar Economic Forum. Qatar News Agency/Handout via Reuters. The 2024 Qatar Economic Forum. Qatar News Agency/Handout via Reuters.For nearly a decade, Gulf states have been building tentpole conferences to draw global money. The war in Iran is threatening those gatherings and the global power they project, Semafor’s Liz Hoffman reports. Bloomberg is likely to delay the Qatar Economic Forum it runs with the country’s commerce ministry, slated for May, people familiar with the matter said ahead of the latest ceasefire announcement. Billionaire Steve Ross, a megabooster of Florida as a new “Wall Street South,” held early discussions about whether the event might be shifted to West Palm Beach, which would have been another coup for the Miami area’s conference circuit. (A Bloomberg spokesman declined to comment on specifics but said the company is committed to hosting the event in Doha, which has been running since 2021.) The longer the war drags on, the harder these decisions get. Saudi Arabia’s Future Investment Initiative and its Emirati answer, Abu Dhabi Finance Week, are typically held in the fall and draw global CEOs whose schedules book up months in advance. Losing these events, or being forced to host them elsewhere, hurts the narrative the Gulf has been painstakingly trying to project as a stable region open for business. |

|

Türkiye’s chance to take on the Gulf |

Turkish President Recep Tayyip Erdoğan. @RTErdogan/X. Turkish President Recep Tayyip Erdoğan. @RTErdogan/X.Türkiye seems to be positioning itself to benefit from a war that has shaken confidence in the Gulf as a haven for business. President Recep Tayyip Erdoğan said this week that the crisis, like the pandemic, would create an opportunity to make the country a regional base for multinational companies and a trade transshipment hub, and could elevate the Istanbul Financial Center among the ranks of global hubs. Although he didn’t name the Gulf states as competitors, Erdoğan appears to be pitching Türkiye as an alternative to Abu Dhabi, Dubai, Doha, and Riyadh. Like them, his country offers modern infrastructure and extensive aviation links, and it also has a large military and a growing domestic air defense system. But it still lacks what has made Gulf cities magnets for investors: trillions of dollars in sovereign wealth funds, vast oil and gas resources, business-friendly regulations, and zero income taxes. — Mohammed Sergie |

|

A cargo truck in the Empty Quarter of Saudi Arabia. Hamad I Mohammed/Reuters. A cargo truck in the Empty Quarter of Saudi Arabia. Hamad I Mohammed/Reuters.UAE trucking company TruKKer was enabling the movement of more than 1,200 loads a day for petrochemical producers, steel manufacturers, and consumer goods companies when Iran closed the Strait of Hormuz. Within a month, the company — which calls itself an “Uber for trucks” — saw volumes surge 30%, CEO Gaurav Biswas told Semafor, as customers scrambled to adjust to port and shipping lane disruptions. TruKKer has seen the supply of construction materials continue, but disruptions in other industries, including aluminum and petrochemicals, have been more pronounced, according to Biswas. Under normal circumstances the company runs predictive algorithms to estimate demand, but the conflict has rendered such predictions useless. Meanwhile, the rules governing the flow of goods through the Gulf have changed. Saudi Arabia has begun allowing UAE-registered trucks to enter the kingdom empty — practically unheard of prewar — and new corridors for expedited freight border crossings have been formalized between Oman, Saudi Arabia, and the UAE, while smaller ports are absorbing volumes they were never built for, according to Biswas. — Kelsey Warner |

|

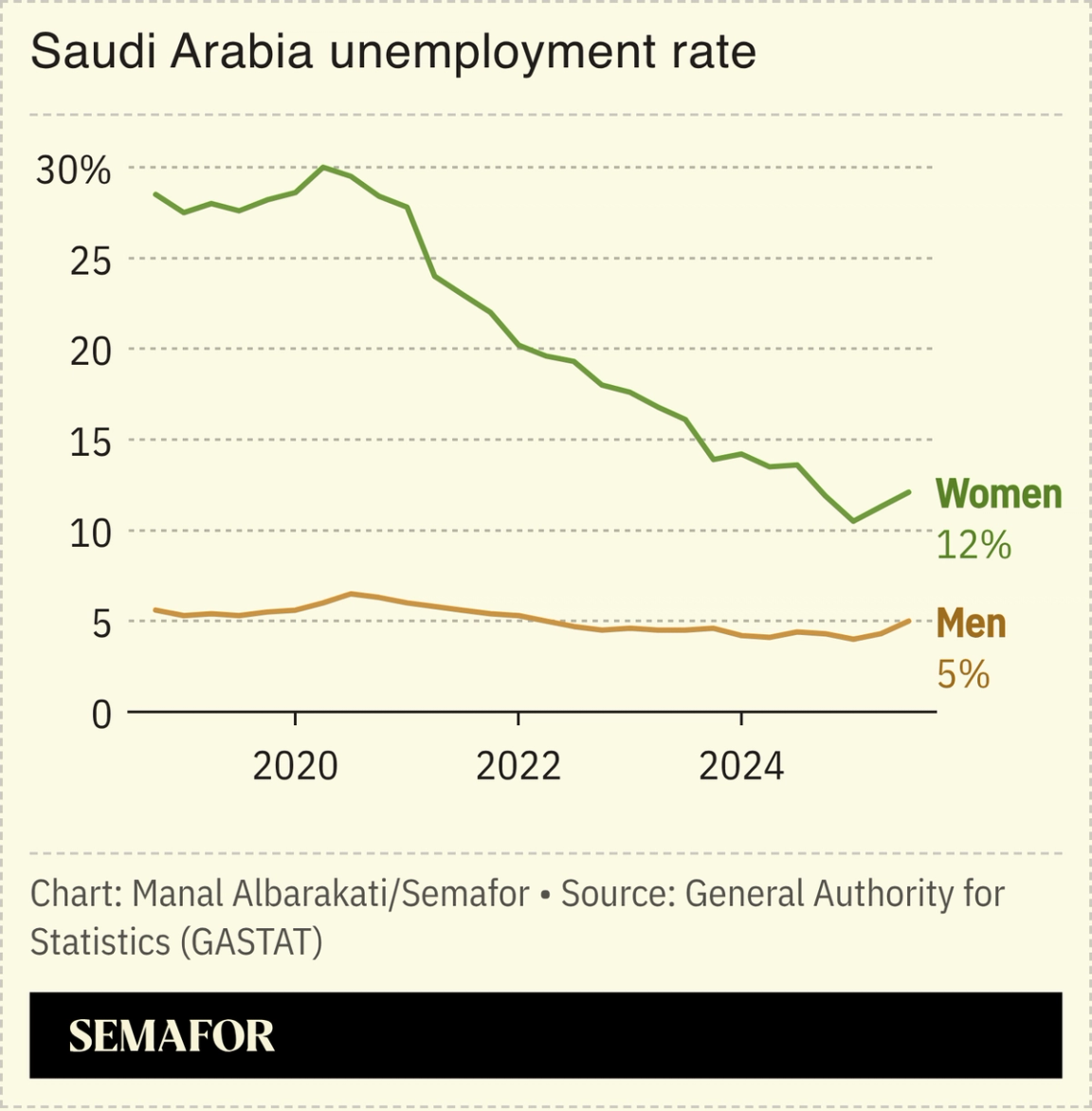

Pushing Gulf nationals to the private sector |

For years, Gulf countries have tried to persuade citizens to take private sector roles rather than rely on government jobs; this week Saudi Arabia and the UAE intensified those efforts. Saudi Arabia expanded its Saudization program — requiring companies to hire only Saudis for certain roles or face penalties — to cover 69 additional job types, including data entry, secretarial work, and translation. The move further tightens the Nitaqat system, which has imposed quotas for Saudi hires since 2011. Meanwhile, the UAE extended its Nafis Emiratization program to 2040, well beyond its original deadline of this year, sweetening the deal for citizens who take private sector jobs with expanded financial benefits. Both programs have shown results: Nafis has brought 152,000 Emiratis into the private sector since its 2021 launch, while Saudi unemployment has fallen steadily to 7% by the end of 2024. — Manal Albarakati |

|

Henry M. Paulson Jr., Chairman, Paulson Institute, Former US Secretary of the Treasury; Georges Elhedery, Group CEO, HSBC; Jenny Johnson, CEO, Franklin Templeton; Sim Tshabalala, CEO, Standard Bank Group; La June Montgomery Tabron, President & CEO, W.K. Kellogg Foundation; and more will join the Future of Capitalism session at Semafor World Economy. This session will examine how the notion of capitalism and free markets as the best system for economies is being challenged in the US and elsewhere. April 14, 2026 | Washington, DC | Apply to attend |

|

Defense- The Iran war may have cost the US up to $31 billion over the first five weeks, according to one analyst, perhaps more once the cost of damaged equipment is included. — Financial Times

Finance- Mubadala Capital, the asset management arm of the Abu Dhabi sovereign wealth fund, raised almost $1 billion for its third Brazil fund. Mubadala Capital and its parent company have been investing in Brazil for years and the latest fundraise shows they are not slowing down investment plans despite the Iran war. — Financial Times

Real Estate- Saudi Arabia’s Kingdom Holding has announced plans for a $1 billion real estate development covering a three-square-kilometre plot in Riyadh — perhaps spurred on by regulations designed to stop land being left vacant. — AGBI

Media- Abu Dhabi-backed Redbird IMI has merged the UK’s All3Media and France’s Banijay Entertainment into what CEO Jeff Zucker calls the world’s largest independent production company, with $5 billion in revenue and 260,000 hours of content, positioning it to challenge Netflix, Amazon, and Apple. — The National

|

|

|