Did you know that the same company responsible for that delicious umami taste in your shrimp chips might also become the cause of a global bottleneck for AI chips? It’s true. Ajinomoto, the company that makes MSG, also makes an industrial film that goes into the chips. And some industry observers say supply of the film is running dangerously low.

The S&P 500, Nasdaq 100, and Russell 2000 managed a positive start to the week yesterday, shaking off a surge in the price of oil that was prompted by President Trump’s order to blockade the Strait of Hormuz after peace talks between the US and Iran over the weekend failed to deliver a deal. |

|

|

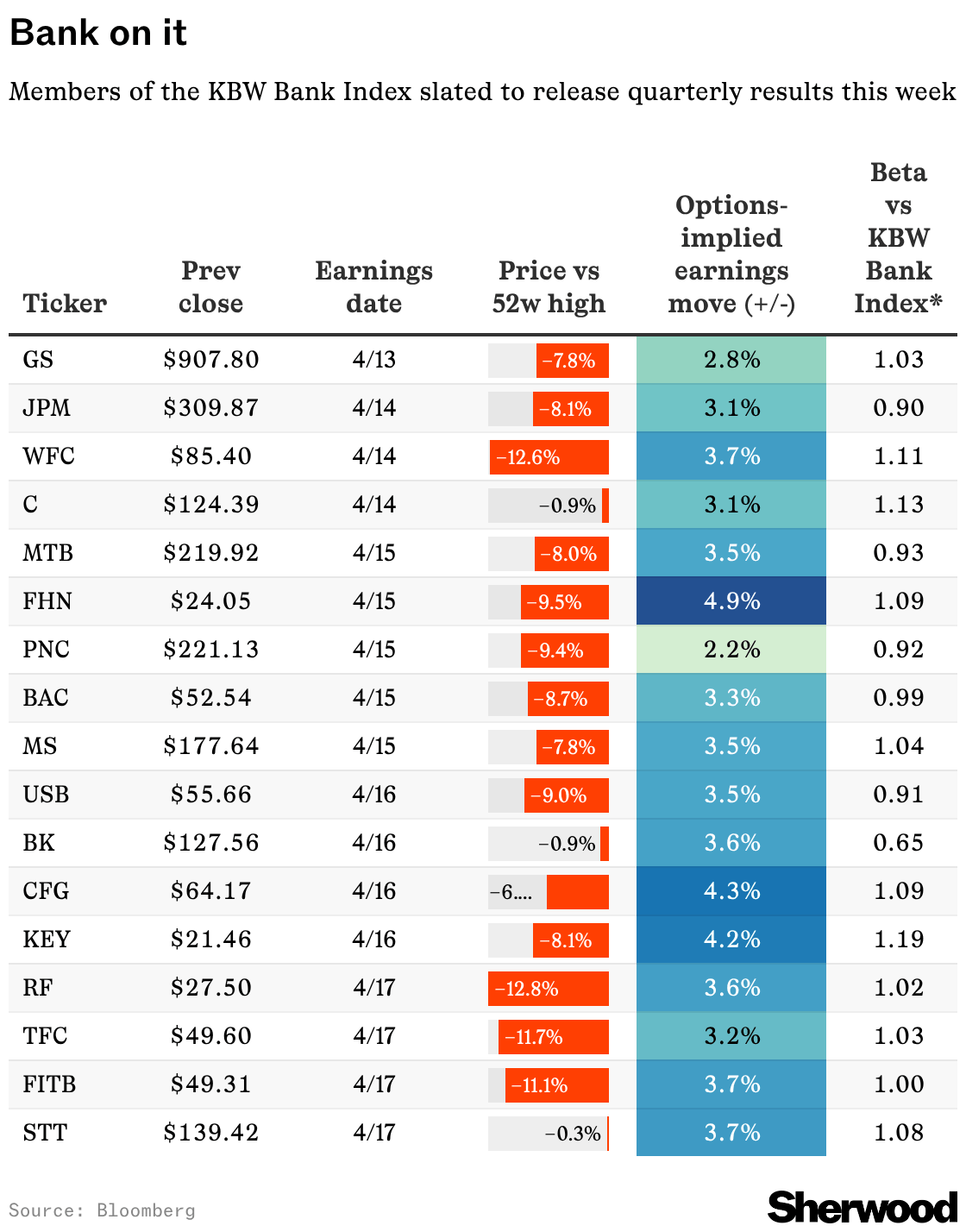

Financials ended 2025 on a tear, perhaps getting a bit over their skis in pricing in a global economic reacceleration thanks to continued fiscal stimulus and the waning impact of tariffs. Every morning this week, we’ll be inundated with news about how America’s banks — from the gigantic, systemically important ones to the small regional players — performed in the first quarter of the year.

Goldman Sachs kicked off the week and reported lower-than-expected sales and trading revenue for its fixed income, currencies, and commodities division. Oof. The stock was down as much as 4.6% in early trading before paring losses to 1.9% by the close.

Trading results may get the early headlines, but here’s what really matters to the market’s mood: |

- Management’s color on the economic outlook and whether they’re seeing impacts on consumers or businesses from higher fuel prices.

- Then there’s the issue of private credit and banks’ exposure to it.

- Private credit funds have been facing investor outflows in light of their elevated exposure to software companies. Anthropic has blown a Claude Cowork-shaped hole in the rosy assumptions about recurring revenue streams generated by software firms.

- In turn, the pricing of many of these funds indicates the market doesn’t believe the loans are worth what these asset managers say they’re worth.

-

…and banks are lenders to private credit funds. JPMorgan recently curbed its exposure to the space while marking down some of these loans, which aren’t publicly traded.

-

Last month, when Deutsche Bank revealed a $30 billion exposure to private credit in its annual report, the stock suffered its biggest one-day loss since April 2025.

|

But maybe the most important reason private credit will be a huge part of the narrative this week is because the media is obsessed with it. Peep this chart of monthly stories about the asset class versus the price of an ETF of business development corporations (BDCs) — the providers of private credit. |

|

|

So far, private credit’s problems have stayed mainly, well, private. Or, at the very least, it’s currently more a story of technological disruption than nascent financial contagion. Besides a few headline-grabbing days, that’s not what we’ve seen. The three-month correlation between bank ETFs and an ETF that holds BDCs is not particularly strong — as charted here. Quite simply, if the travails of private credit are A Big Deal, then it should be a driving force for not only the BDCs that extend this financing, but the banking industry as a whole.

|

|

|

How much do you really know about the Nasdaq-100®? |

The Nasdaq-100 is much more than a tech index – it is the foundation for a $1.4 trillion ecosystem — spanning ETFs, derivatives, structured notes, and more. All built on 100 of the world's most innovative large cap companies.

Since its launch in 1985, the index has evolved into what many are now calling the "Benchmark of the 21st Century." Nasdaq's latest research breaks it all down — the products, the liquidity, the growth, and the key characteristics that make NDX® a true large cap index. Get all the insights here → |

|

|

For years, Americans couldn’t get enough of Modelo and Corona, helping turn their US importer, Constellation Brands, into one of the fastest-growing companies in consumer staples. Now, that streak may finally be drying up. |

- Last week, the beer and wine giant reported a 10% decline in net sales for the year ended February 2026, driven by a 3% drop in beer sales and a 51% plunge across its wine and spirits — though the latter segment was largely dragged down by its divestiture of lower-end wine labels.

-

The company said that overall demand across beer, wine, and spirits “remained subdued” during much of the year as its core customer base, particularly lower-income households and Hispanic consumers, cut back on spending or traded down to cheaper alternatives amid economic uncertainty.

|

When Constellation acquired the full US rights to import and sell a bevy of Mexican beer brands, including Modelo, Corona, and Pacifico, in 2013, beer made up roughly half of its sales. Today, that share exceeds 90% of total revenue, with Modelo Especial now the top-selling beer brand by dollar sales in the US. Sounds good, right? |

- But the company’s beer sales growth streak reversed for the first time in 12 years in FY26, with shipments falling roughly 4% from the prior year, or just over 15 million cases. The slowdown has been showing up across beer coming from Mexico more broadly, too.

-

With Constellation accounting for a dominant share (about 93%) of Mexican beer imported into the US, the category’s total import value also fell 4.3% in 2025, marking the first annual decline at the border since 2009 after more than two decades of growth.

|

|

|

The slowing demand also reflects a longer-term shift in how Americans think about drinking. A 2025 Gallup survey found that US drinking rates hit a record low, with two-thirds of younger Americans saying even moderate drinking is bad for health, up from just 28% in 2005. Meanwhile, the rise of GLP-1s — which a growing body of research links to lower alcohol consumption — alongside the surging popularity of nonalcoholic alternatives have also been weighing on the industry. |

|

|

Tesla CEO Elon Musk has blamed the lack of Full Self-Driving approval for making Europe its “weakest market,” but approval from one country doesn’t mean Tesla’s European sales will immediately rebound: the Netherlands is a relatively small market, and there are key differences between the US and European versions of the technology.

|

|

|

|