| |  | | | | | | Not a subscriber? Sign up here to get this newsletter in your inbox. In today’s issue: - Insurers launch a bid to rein in prior authorization amid Washington’s focus on affordability

- Lobbying spending among some insurers climbs to record levels as policy fights intensify

- New data showing coverage losses in state-based Affordable Care Act plans may revive debate around the expired enhanced tax credits

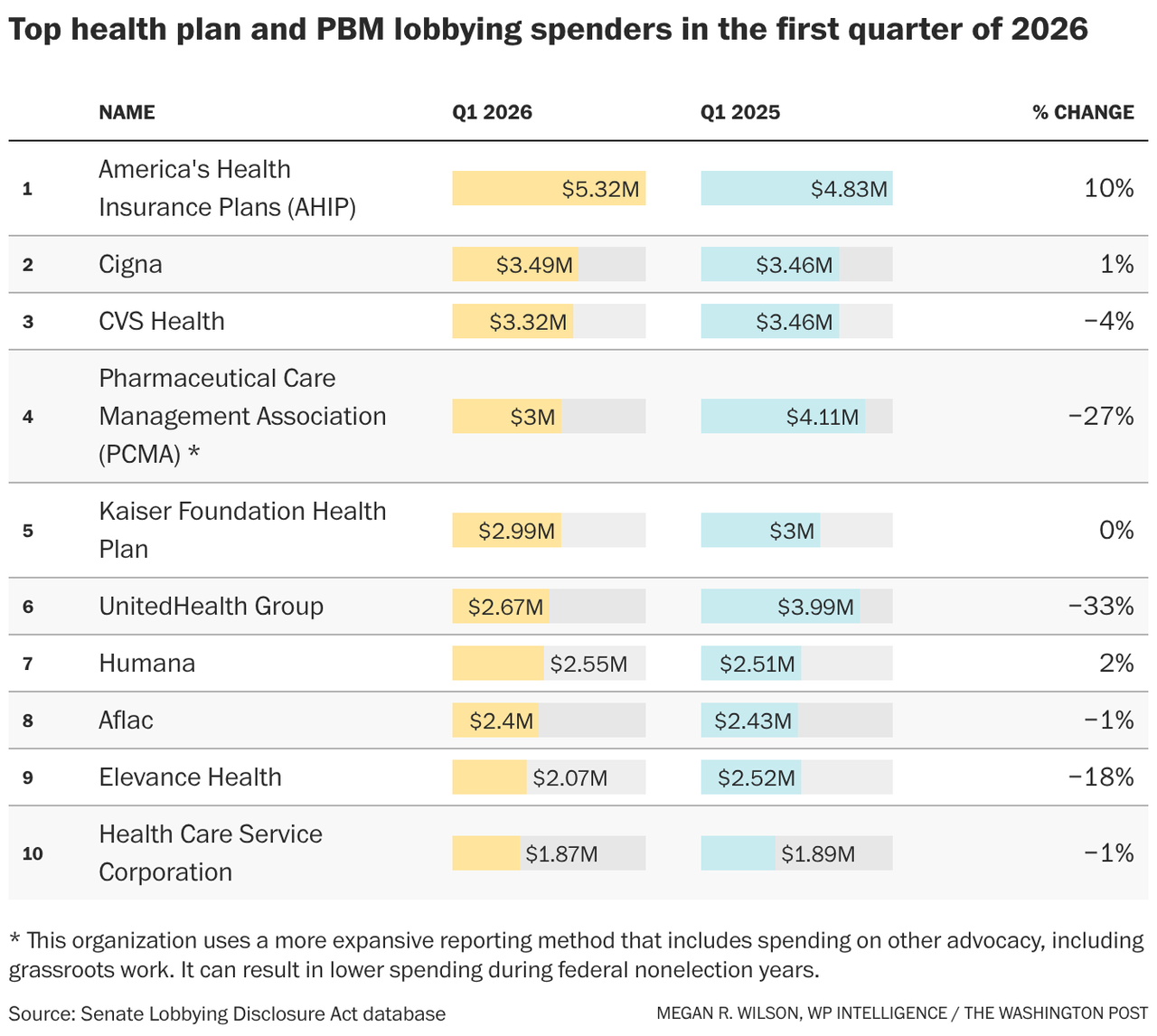

Good afternoon, and welcome to Health Brief. This edition continues our examination of early 2026 lobbying spending for health insurers, following briefs on the advocacy efforts of hospitals and the pharmaceutical industry earlier this week. It’s Feedback Friday. What’s on your mind? Don’t hesitate to reach out with your feedback and insights about the next big health policy fight. I’m at megan.wilson@washpost.com. Or, if you’d prefer to message me securely, I’m also on Signal at megan.434. |  | | Top insurance industry CEOs testify before the House Ways and Means Committee in January. (Demetrius Freeman For The Washington Post) | | | |  | The Lead Brief | Health insurers said Friday they’d be ramping up efforts to cut down on prior authorization requirements, one of the most unpopular areas of health care. It’s part of a broader offensive aimed at easing political pressure as policymakers in Washington sharpen their focus on health care affordability and patient access. The new commitment, signed by about 50 insurers and led by major insurance industry groups AHIP and the Blue Cross Blue Shield Association, aims to standardize electronic prior authorization requests for most medical services. UnitedHealth Group, which is not a member of either organization, came out with its own initiative Friday, saying it anticipates that more than 70 percent of all prior authorization requests will be part of its standardized submission process by the end of the year. Why it matters: The move comes as insurers clash with providers and face bipartisan scrutiny over delays and denials that providers say can jeopardize care — and it could help the industry cast itself as part of the solution on affordability and access. Next week, House lawmakers are set to grill hospital executives about their role in rising health care costs. “This is a meaningful step forward toward giving patients faster answers, more certainty, and fewer unnecessary delays in care,” wrote Mehmet Oz, who leads the Centers for Medicare and Medicaid Services, in a post on X about the newly announced measures. “I applaud these efforts from a collection of the largest health plans across most market segments as momentum builds,” Oz wrote in the post, which was reposted by a health insurance executive. “We look forward to continuing to work with health plans and providers on improving care for patients through this effort.” Companies have been working with the Trump administration on voluntary commitments to simplify and cut back on prior authorization requests that can delay treatments for patients, as regulators propose rules that would tighten prior authorization response time requirements for Medicare Advantage plans. | | | | | | Lobbying Ledger | That proactive posture is also showing up in how insurers are deploying their resources in Washington. Disclosures covering the first three months of this year show much of the industry lobbying on Medicare Advantage payment policy, the expired enhanced Affordable Care Act subsidies, and issues involving prior authorization, drug pricing, PBM reform and mental health parity. About half of the 21 insurance companies and pharmacy benefit managers (PBMs) — and their trade associations — that spent more than $250,000 on lobbying during the first three months of 2026 increased their advocacy compared to the year before, according to my analysis of federal lobbying disclosures. Even more — 15 in total — increased their spending this year compared to the first quarter of 2024. Earlier this year, top health insurance executives were called to testify before two House committees regarding how their business practices may be driving up the cost of care. Senate Democrats launched a long-term effort to craft legislation overhauling the health insurance system. The early-year lobbying spending underscores how insurers are pairing public-facing policy shifts with a broader advocacy push as they try to shape the contours of any coming reforms. |  | | AHIP, one of the industry’s major trade associations, spent more than $5.3 million lobbying during the first quarter of this year — the most it has ever spent on advocacy in a quarterly period. It disclosed lobbying on a broad slate of policy issues, including Medicare and Medicaid policy, health savings accounts, PBM oversight, and a range of issues involving transparency, prior authorization and drug pricing. Smaller plans also increased their lobbying: The Alliance of Community Health Plans Association spent $680,000 in the first three months of 2026, a 31 percent increase over the same period last year. The figure is the most the group has ever spent on lobbying in a quarterly period. The organization listed lobbying on Medicare Advantage and Medicare’s prescription drug program reforms, telehealth flexibilities, provider directory accuracy, and broad drug competition policies, including increased biosimilar adoption. → A Trump administration proposal to keep Medicare Advantage payment rates relatively flat prompted a forceful advocacy push. The pushback ultimately resulted in CMS finalizing a much higher Medicare rate than it had proposed in January, in addition to nixing some reforms that would have further cut into reimbursement rates. The Better Medicare Alliance, a group supported by health plans to advocate for Medicare Advantage, also broke its own lobbying spending record. The organization spent $680,000 lobbying during the first three months of this year, the most it’s ever spent in a single quarter. The figure is a more than 30 percent increase over the same time in 2025 and a 70 percent boost over the first quarter of 2024. | | | | | | Industry Rx | Here are three policy areas impacting insurers to watch this year: — PBM reform and the pushback: There is an appetite from some lawmakers to go further on PBM reforms following sweeping measures signed into law earlier this year, which could keep the industry on defense. Drugmakers, some employers and provider groups are fueling the push to further rein in the PBM industry, which negotiates discounts on medicines and chooses which drugs an insurance plan will cover. But PBMs plan to fight back, urging policymakers to tackle other players in the system. The Pharmaceutical Care Management Association, a PBM industry group, says it’s only going to increase its efforts to highlight what it argues are abuses by the pharmaceutical industry that keep costs high. “PCMA is entering a new era, following the passage of PBM reform, to aggressively promote the value of our industry and ensure lawmakers are focusing on the real obstacles to lower costs, such as the way big drugmakers are gaming the patent system,” said Greg Lopes, a PCMA spokesperson. — Surprise medical bills: Implementation of the No Surprises Act, the law meant to protect patients from massive medical bills if they unknowingly visit an out-of-network provider, has spurred a battle between providers and insurers. Each side argues the other is trying to game the system in their favor. A key priority for the Blue Cross Blue Shield Association (BCBSA) this year, according to David Merritt, the association’s senior vice president of external affairs, will be addressing the law’s “broken independent dispute resolution process.” BCBSA spent more than $1.5 million on lobbying during the first quarter of 2026, a 27 percent increase from the same period in 2025. A rule that aims to improve the process to mediate surprise billing disputes between insurers and providers is under review at the White House, and there are still several other provisions of the No Surprises Act yet to be implemented. — Health coverage reforms: Even though Democrats lost the battle to revive enhanced Affordable Care Act tax credits that helped Americans afford their insurance, with many Republicans arguing the money improperly went to enrich insurance companies, it could become a salient issue if Democrats regain a majority in the House or Senate in November. More on that below. | | | |  | State scan | More people who buy their insurance through state-based Affordable Care Act exchanges are dropping their coverage, according to an analysis from the State Marketplace Network, prompting concerns about affordability challenges following the expiration of enhanced federal subsidies. - Data from 17 state-based Affordable Care Act marketplaces shows disenrollment — people exiting the market — is accelerating, up 24 percent compared to March 2025. More than 900,000 people have dropped coverage since the start of 2026.

- At the same time, new sign-ups are lagging. New enrollees now make up just 18 percent of the market, down from 22 percent a year ago.

- Disenrollment or changes in plan selection — such as moving from more generous silver plans into lower-premium bronze coverage, often with significantly higher deductibles — is likely driven by costs. Monthly premiums vary widely but have increased, on average, by as much as 74 percent for some people, even after subsidies.

The analysis doesn’t include enrollment data from the HealthCare.gov federal insurance marketplace. It’s also missing data from a few other states that didn’t have information available. Why it matters: The 2026 data is an early warning sign for coverage stability in a way that impacts patients, insurers and health care providers. But it also could raise the policy stakes in Washington ahead of the midterms. Lawmakers are already debating affordability fixes, and the link between subsidy rollbacks and coverage losses could revive pressure to restore or replace enhanced premium tax credits. → Some states are trying to blunt the impact. In Washington state, a new policy led to a 16 percent decrease in net monthly premium costs. Ten state marketplaces are offering their own subsidies, though many are limited. New Mexico stands out, however, posting a 13.8 percent enrollment increase after fully replacing the expired federal subsidies. | | | | | | | | | | |

_tstmp_1756933376-1920-1080.png)