Brent crude initially rose on claims by Tehran at the weekend that it had re-closed the Strait of Hormuz. While traffic through the strait did drop on Sunday compared with an uptick on Friday, analysts still reckon movement is back up to about a quarter of pre-war levels, as the new 60-day ceasefire and talks get underway.

The positive signals out of Switzerland helped boost Asian markets on Monday, with Japan's Nikkei and South Korea's KOSPI both closing higher. U.S. futures were slightly lower before the bell, however, and European shares were muted.

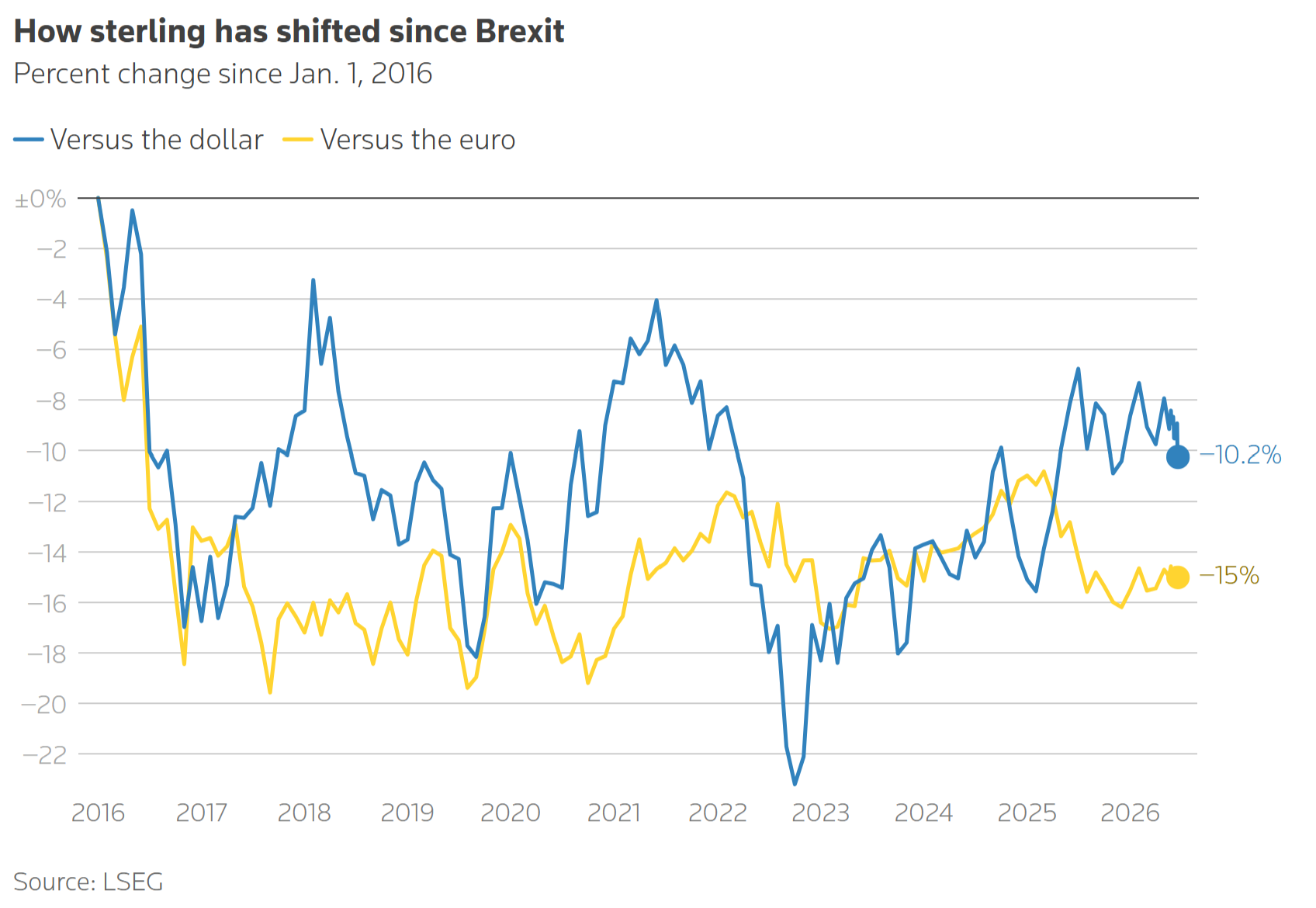

The other big development on Monday was the resignation of British Prime Minister Keir Starmer, whose political crisis deepened last week after a by-election win by his key Labour Party challenger Andy Burnham. Starmer will stay in his post until a new party leader - and prime minister - is selected, with Burnham seen as the overwhelming favourite. His successor will be the UK's seventh leader in 10 years.

UK stocks slipped on the news, while sterling edged up. Markets will watch Labour Party developments closely for signs of how the leadership process will unfold - as well as who may end up as finance minister.

Back on Wall Street, markets are still digesting Kevin Warsh's first meeting as Federal Reserve chief and the week-old SpaceX IPO. A hawkish takeaway from the former sapped some of the ebullience from the latter late last week - though Wall Street indexes still finished higher on the week and the rocket maker remains up more than 30% from its listing price.

Elsewhere, the yen continued to languish past the 160-per-dollar level, close to a 40-year low. Markets are looking for signals that Japanese financial authorities may be shifting their communications strategy in advance of another round of intervention.

A quieter week ahead on the events calendar includes the release of U.S. personal consumption expenditures (PCE) inflation data for May on Thursday, as well as June business surveys from around the world.