Stumbling megacaps dragged the S&P 500 and Nasdaq lower on Monday, though chipmakers did much better, ahead of memory chipmaker Micron's results due out Wednesday. A recent theme seemed to play out again: buying stocks that benefit from the AI spending splurge and selling those doing all the spending.

However, the hawkish Fed interest rate outlook weighed on stocks at large, with a rate hike now fully priced in for September and a more than 50% chance of two by year-end.

Tech stocks around the world fell overnight in the slipstream, with South Korea's high-flying KOSPI index off nearly 10% on Tuesday, partly on warnings about the ongoing weakness of the Korean won. Stateside, Wall Street futures were in the red before the bell, with Nasdaq futures tumbling more than 2%.

Elsewhere, in currency markets, the yen continued to flirt with 40-year lows set two years ago, with Fed-fuelled dollar strength trumping the impact of last week's Bank of Japan rate hike. There were reports of contact between Tokyo and Washington officials on the issue of yen stability, keeping intervention fears on the boil.

On the energy front, oil prices continued their slide under $80 per barrel, with Brent crude trading at around $77/bbl early on Tuesday. That came amid more signs of returning oil flows through the Strait of Hormuz and as the U.S. waived sanctions on Iran for 60 days on Monday after initial peace talks.

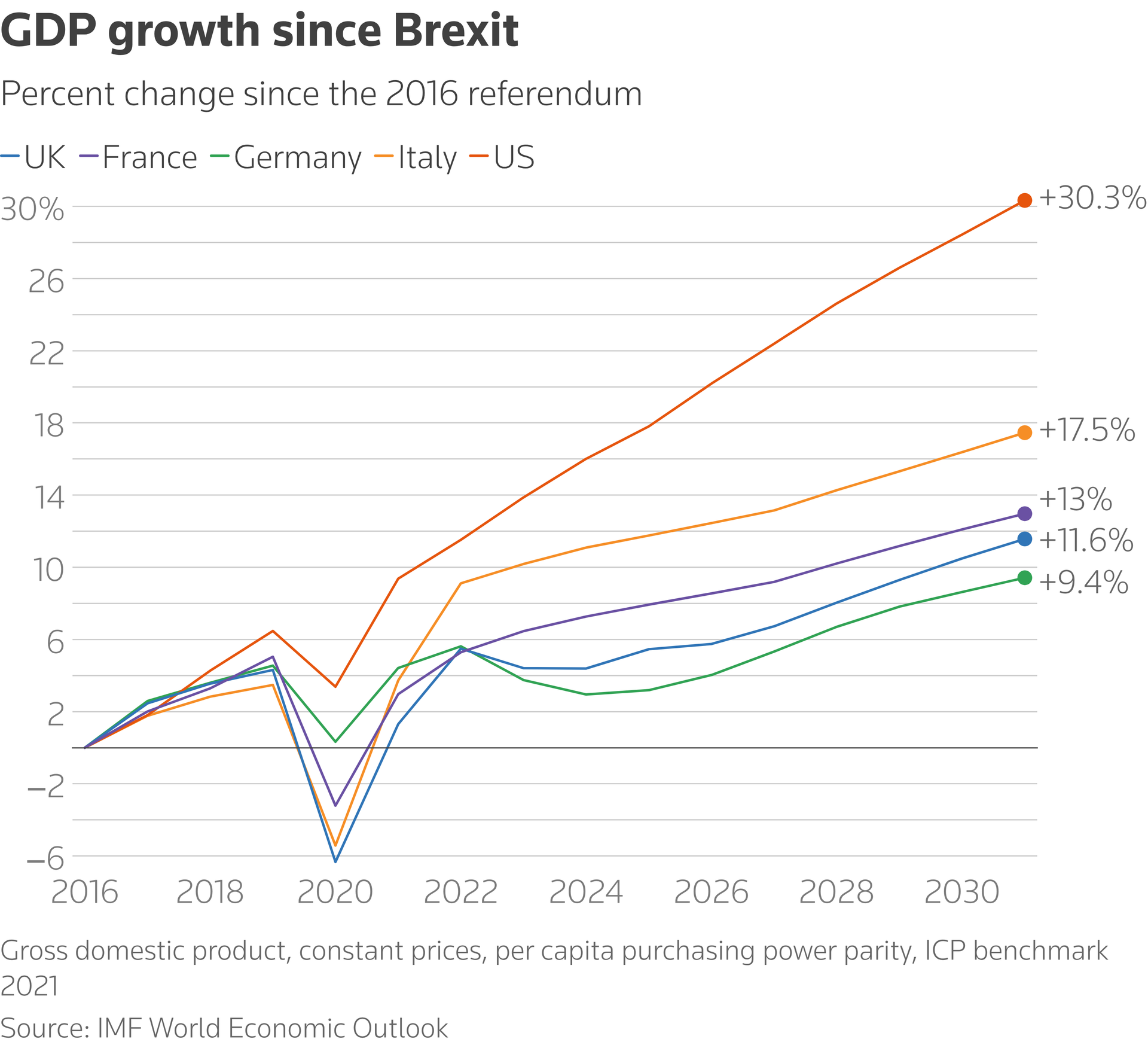

In Europe, British Prime Minister Keir Starmer's resignation on Monday left UK markets relatively unperturbed. Focus is now shifting to how quickly his likely successor Andy Burnham can be appointed - and who Burnham might choose as finance minister.

The data slate for Tuesday will include the release of flash U.S. and global business surveys for June, though the big retreat in oil prices since last week's U.S.-Iran memorandum of understanding came after those polls were conducted.

With that, onto today's column.