| | In this edition, OpenAI makes a $100 billion bet on ads, and Alan Greenspan’s legacy is tested by AI͏ ͏ ͏ ͏ ͏ ͏ |

| |  | Business |  |

| |

|

- OpenAI’s $100B ad bogey

- Everything is TV

- Greenspan’s legacy

- PE makes insurance risky

|

|

AI is going to make a lot of things a lot cheaper. But not all goods want to be cheap. They’re called Veblen goods — products whose demand increases alongside their price. The canonical examples are handmade luxury items like Hermès bags. AI is likely to have limited effect on what they’ll cost to produce. But the category also includes products that are most vulnerable to AI: the knowledge-economy work that Wall Street sells. They’ll soon be able to offer it more cheaply, but I doubt they will. There’s been surprisingly little price competition for investment-banking advice over the years — you’ve never read about the Great Cola War of IPO underwriting because there wasn’t one. Clients don’t tend to buy more Goldman Sachs M&A advice when it’s cheaper. In part, Wall Street is immune to price pressure because the customers (corporate executives) are spending other people’s money (shareholders). But paying for top-shelf advice is a signal the same way that dropping $10,000 on a handbag is, and the stakes are a lot higher. When the last crop of rainmakers spun out of big firms to launch their own boutiques in the late 2000s and early 2010s, they didn’t win business by undercutting incumbents. In fact, the Goldmans of the world welcomed the arrival of the Centerviews precisely because these newcomers charged a lot, propping up fees in the industry’s upper ranks. “I hope not,” Lazard CEO Peter Orszag told me in April when I asked if his firm’s fees would shrink as AI automates grunt work. (I was thinking about all this as I read this Bloomberg story about Lazard cutting its fees to snake away a plum Venezuela assignment from a rival; white-glove service is rarely pitched as a red-tag special, even to broke governments.) If good-enough advice becomes cheap and ubiquitous through AI, the premium on the prestige alternative goes up, not down. Fast fashion made Hermès more valuable as a signal precisely because the baseline got cheaper. Commoditization at the bottom of a market brightens the halo at the top. The question now is whether investment banks can actively manage their businesses the way luxury houses do — resisting the temptation to expand downmarket and keeping the velvet rope up. There’s an argument to go the other way, to expand the pie of companies that might be willing to pay for the Goldman Sachs or Morgan Stanley imprimatur by pitching them a service that’s, say, 80% AI-generated and topped up by a human. But nobody confuses Harvard Extension School classes with the real thing. I don’t expect Wall Street’s elite to stoop. They’ll cut whatever costs AI allows and let more of those fees drop to the bottom line. |

|

OpenAI’s big bet on advertising |

Courtesy of OpenAI Courtesy of OpenAIOpenAI splashed down at Cannes, the advertising world’s annual gathering, with a $100 billion bogey: That’s how much the AI company expects to generate selling ads by 2030, about half of Meta’s annual ad revenue. The company’s press briefing Monday revealed an emerging technology powerhouse at a moment of awkward transition. Creative specialist Chad Nelson joked to sweaty reporters in a decidedly unglamorous (for Cannes, anyway) setting about his uncertainty around the event’s correct pronunciation, but showcased powerful creative tools that already have competitors on high alert and advertisers intrigued. OpenAI said it has thousands of advertisers in seven test markets for integrating paid spots into its products, including the US. An executive said users don’t seem alienated by new AI ads in test markets, noting that the frequency of users seeing an ad and navigating away was “far lower” than when the company began testing. |

|

Everything old, even TV, is new again |

Instagram InstagramEverything is TV now, and the competition is heating up. Instagram’s deal with Samsung will put the social-media app’s videos on more screens, challenging both YouTube for creator loyalty and Netflix, which has been moving into influencer content. All three continue to peel eyeballs away from cable TV. Instagram now has the distribution, via Samsung’s estimated 68 million smart TVs across the US, and the content, courtesy of influencers and creators, to compete for the middle screen. Its challenge is making Instagram a primary platform for creators, not just a way to funnel fans to their YouTube pages, where pay for personalities like MrBeast is higher. It’s also getting ready to introduce longer-form videos on Instagram. “We’re late to the game,” Instagram chief Adam Mosseri said last year on Semafor’s Mixed Signals. “There’s an immense amount of time spent on TV, where some of our competition is showing up with force.” The question is whether Meta will make its own content, as it tried to do several years ago when it financed high-quality production for shows like Jada Pinkett Smith’s Red Table Talks, or simply monetize what those influencers are already posting and split the money. A Meta spokesperson told Semafor “not yet” when asked about a renewed effort on original programming. Either way, Instagram’s push onto larger (notably, horizontal) screens signals a shift. For years, it was Netflix who gave cable companies heartburn. Now, podcasts are on our TVs, cable companies are trying to buy them, and YouTube is television for a younger generation. — Rohan Goswami |

|

Greenspan’s legacy tested by AI jitters |

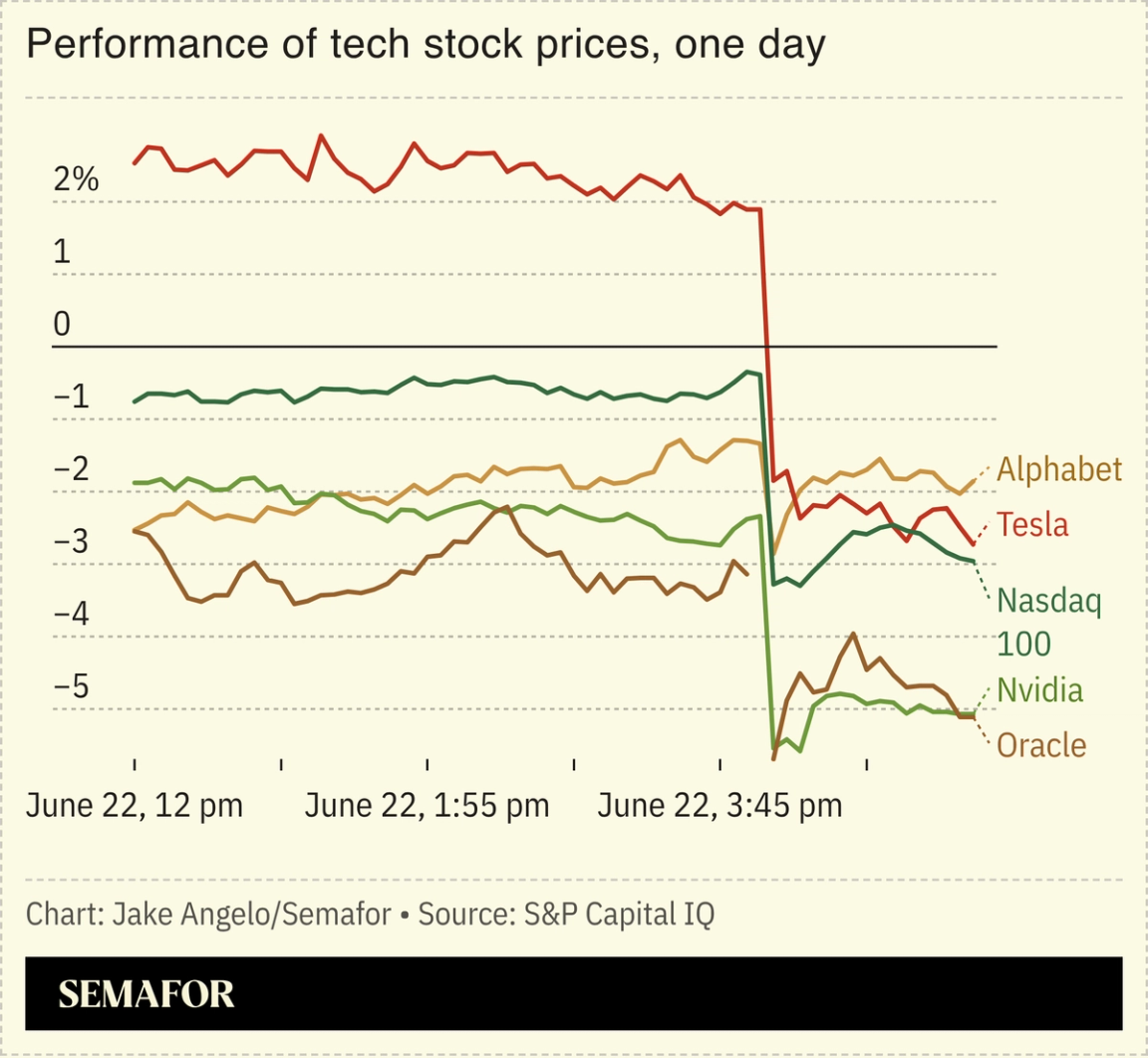

Alan Greenspan died Monday at 100 years old, and the obituaries have been kind. The former Fed chair lived long enough for his reputation to rebound from the 2008 crash, which was partly blamed on deregulation he encouraged. He’s being remembered as the Maestro of monetary policy. His less flattering legacy arrived on cue: Tech stocks are falling sharply as the market’s snooze button on AI spending fears times out again. Alphabet had its worst day in a year yesterday, and Nvidia, Oracle, and Tesla all opened sharply lower today — a slide that’s spilled over to South Korea’s electronics-heavy index. The question for permabulls and knife-catchers alike: Will the Fed bail them out? The “Greenspan put” — the easy-money policies that time and again protected stockholders from their worst mistakes — may be tested in the months ahead. Starting after 1987’s Black Monday, markets came to believe that the Fed would cut rates whenever equity prices wobbled seriously enough, which made risk feel cheaper than it was. The policies were continued by Greenspan’s successors, breeding “a generation of investors that really never learned the price of being wrong,” as Citadel Securities President Jim Esposito told Semafor this spring. Now Kevin Warsh runs the Fed, with the market pricing better than 60% odds of a rate hike by year-end and little to no chance of a cut. Whether investors have actually internalized that — or are still, somewhere, waiting for the Maestro’s ghost to ride to the rescue — is the question Greenspan leaves behind. |

|

Private equity pushes insurance to get risky |

Semafor/YouTube Semafor/YouTubePrivate equity’s headlong rush into the life insurance industry has misaligned incentives, inflated risky assets, and produced a crop of “zombie insurers” just waiting to blow up, according to one of the few insiders willing to say so out loud. “We know them, we see them, we whisper about them,” Anant Bhalla said on the latest episode of Semafor’s Compound Interest. “We need to speak more openly about it.” Bhalla warned that private equity’s pressure is “high-octane fuel” pushing what should be the safest asset people own — retirement guarantees and death benefits — into dangerous investment territory. Bhalla ran American Equity, a $50 billion insurer he sold to Brookfield in 2023, giving him a front-row seat to the transformation of life insurance from a sleepy, bond-oriented business into a multitrillion-dollar funding engine for exotic investments. He now runs 1823 Partners, a private investment firm backed by one of Europe’s richest families, and manages money for the family-owned life insurer. Apollo’s 2014 bet on its insurer Athene spawned a decade of copycats, and over the past few years, most big alternative asset managers have either bought a life-insurance company or launched dedicated businesses to manage their money. The few that didn’t have hustled to catch up. These firms steer policyholders’ money into their own financial products, which have higher risks and higher returns than the blue-chip corporate bonds favored by more conservative independent insurers. “Anything that has a cash flow or even the hope of a cash flow” is fair game, Bhalla said. Not that he’s opposed to alternative assets. “The question isn’t ‘can we go back to the good old days of having 100% plain vanilla bonds,’ because that ship sailed 10 years ago. To me, the fundamental question is, ‘can we make it work with a healthy mix… Can we do it with safer private assets?’” |

|

You can do a lot in 10 minutes… like make sense of the global economy. Each day, the Marketplace Morning Report podcast explains what’s happening in the economy, why it matters, and what it means for the way you live and work. It’s essential analysis from award-winning reporters you can trust. Listen now. |

|

➚ BUY: Front office. EQ wins in an age of AI: A new survey of hiring managers finds more than half have promoted an employee over the past year for their people skills over technical abilities. ➘ SELL: Back rooms. Japan’s new, generally pro-business prime minister has offended big companies by refusing to meet with them. Access is everything. |

|

Companies & Deals- Gimme the loot: Investors in Apollo’s flagship loan fund asked for 17% of their money back in its second quarter, the latest sign of distress in private credit. The company’s co-president John Zito pushed back against claims of a crisis: “There’s been no financial institution failing…the structure is right.”

Watchdogs- Command economy: The Trump administration’s tech-interventionist streak continues with an executive order to accelerate the development of quantum computing. It’s a first step toward commercializing a technology that, as Semafor’s Reed Albergotti said last year, needs a “NASA-like movement.”

Markets- Relaunch: SpaceX shares rebounded Tuesday but are still down about 20% over the past week, after the company’s $20 billion bond offering — just days after its $85 billion IPO — raised questions about what it needs all that money for. (Rockets, robots, AI, presumably buying a $1.5 trillion Tesla: The list is long.)

|

|

|