Urgent. Unlikely to be around much longer...

Top 4.9% 1yr FIXED savings, the rate is guaranteed and unusually your money isn't locked in!

Plus more ways to boost your savings interest

It's the refrain we hear constantly... "Why can't I just get a savings account where I know the rate will stay high?" You can. It's called a fix, where the rate's guaranteed for a time. The cost of that guarantee is normally your money's locked away for that period and you can't withdraw it. Yet not right now...

| All accounts below have the full UK £120,000 per person, per institution savings safety protection. All interest rates listed are AER. |

Top 1yr fix 4.9% with access. Ending soon? The Marcus (part of Goldman Sachs) 4.9%1yr fix* (min £1) is the highest-paying 1yr fix right now - the next best is a decent whack less at 4.76%. Unusually, Marcus lets you close the account mid-term to withdraw your money, though it'll deduct 90 days' interest if you do (close it within the first 90 days and you lose all interest paid to that point).

This is a big advantage for anyone put off fixing as there's a small risk you might need the money in that time - this gives you a 'get-out-of-jail-free' card. As for how it compares to other fixes, see our full list of top fixed savings, but in brief...

Why do we say it may end? It's already been around a few weeks, and with fixes like this, providers usually want to bring in a certain number of accounts. Our best guess is it's close to that, so there's a real chance it could be pulled imminently.

Cash ISA fixes let you withdraw too. While what Marcus is doing is rare for normal savings fixes, it's not unusual for the top tax-free fixed cash ISAs. ISA rules say they must always allow you to withdraw without notice - though they can, and all do, charge an interest penalty.

Yet fixed cash ISA rates are lower than normal savings, so they're only worth it if you've not used your £20,000 ISA allowance this year and would likely pay tax on interest from normal savings.

Also remember you always have a right to transfer a cash ISA to a new provider. When these mature, you'll likely be moved to a poorly-paying easy-access account, so diarise to do a transfer then to up the rate. See how to do a cash ISA transfer.

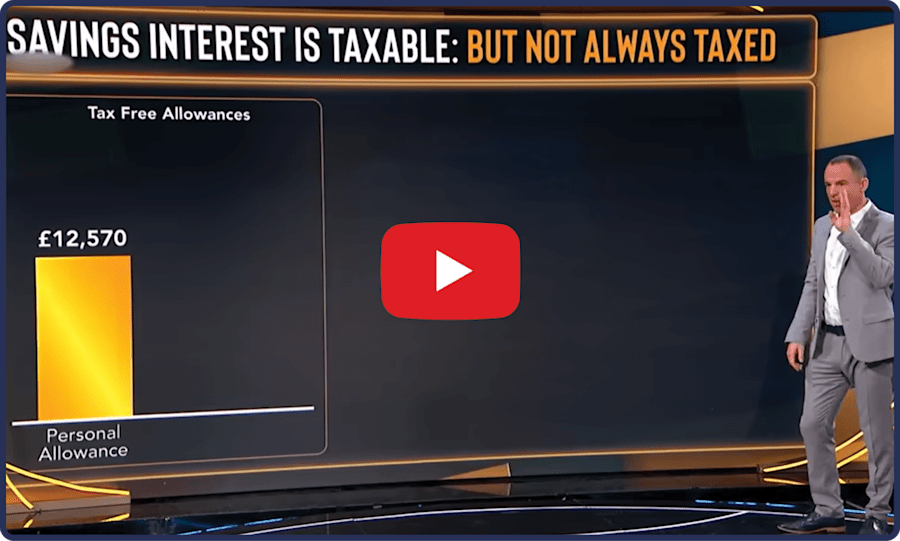

How does tax on savings work? It's easiest to just watch Martin's savings tax explainer...

How long should you fix for? Fixed rates normally get stronger the longer you fix. That's not really the case right now, which shows the market's long-term view is interest rates will be pretty stable. So if you want to save, you can comfortably lock money away, and you strongly value certainty, then fixing - and fixing for longer - looks a decent option at the moment.

But remember, if you go for a longer fix and rates rise in the meantime, your money's locked away, so you can't move it to up the rate (except in a long fix cash ISA). Yet don't think you need to pick just one fix length. You can hedge your bets with several fixes of different lengths.

If you can lock away money for a longer period, say 5+yrs, and you've already got a cash emergency fund, savings may not be right for you. Give Martin's beginner's guide to investing a read - you're in the sweet spot for that, and done right, it could be far more lucrative.