| I’m Chris Anstey, an economics editor in Boston, and today we’re looking at the benchmark US cost of borrowing. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X via @economics. And if you aren’t yet signed up to receive this newsletter, you can do so here. Treasury Secretary Scott Bessent has repeatedly made clear since taking office in January that the most important gauge of borrowing costs for the Trump administration isn’t the Federal Reserve’s overnight rate, but 10-year Treasury yields. And, unlike the Fed’s benchmark, those have been going down lately. Tuesday saw that key metric of longer-term borrowing — which is used as a baseline for contracts such as 30-year fixed-rate mortgages — go as low as 4.13%, well down from the mid-January high of 4.81%. That’s the equivalent of almost three rate cuts for the Fed, which hasn’t moved this year and isn’t preparing for action anytime soon. The scenario Bessent has sought is one where investors are bidding up Treasuries prices (bringing down yields) as they gain confidence in Trump’s agenda of deregulation, extended tax cuts and energy-industry expansion, which would all boost the supply side of the economy and bring down inflation. But that’s not the narrative bond market participants are weaving. Instead, the drop in yields appears mainly to reflect a weakening in growth prospects, propelled by Trump’s tariffication policy. Supporting that argument: as Treasuries logged a near-3% gain for the first quarter, the S&P 500 Index slid 4.6%. Ian Lyngen at BMO Capital Markets calculates that it was the biggest quarter for Treasuries to outperform stocks since the April-to-June period of 2022, when the Fed was launching its most aggressive monetary tightening campaign in four decades — in other words, hardly a happy time for the economy. Does it matter whether borrowing costs come down for the “right” or “wrong” reason? Arguably it does very much. If it’s cheap to borrow but businesses and households’ sentiment about the economy is poor, they are less likely to take on credit and power ahead. And recent surveys aren’t exuding optimism on that score. Tuesday’s ISM manufacturing report for March showed a slide in new orders to the lowest level in almost two years, with a gauge of prices accelerating sharply. Separate surveys from across the country have shown that uncertainty around how and when Congress will enact tax legislation, on top of Trump’s tariff plans, have hurt expectations for investment. The bond market’s narrative will doubtless evolve as the year progresses. For now, yields are down but worries are up. The Best of Bloomberg Economics | - Chicago Fed President Austan Goolsbee warned of the negative impact of weaker consumer spending or business investment due to uncertainty.

- Britain’s Labour government hiked the minimum wage this week but for many of the country’s low-paid workers, raises have been on the decline.

- Inflation is casting shadow over Japan’s cherry blossom season.

- Mexico’s government pledged to narrow the fiscal deficit next year.

- Millions of young Chinese graduates are becoming delivery drivers or “professional children” who move back home.

- How Spain became big pharma’s new hotspot in Europe.

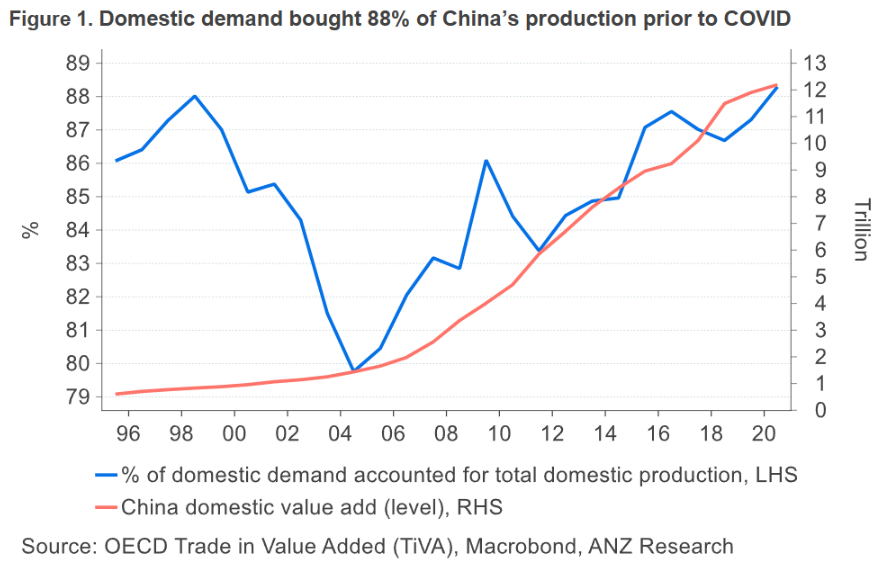

China’s labor market faces a blow from Trump’s tariff hikes on the country — but not due to the hit to exports, as many observers might assume, according to Raymond Yeung, chief greater China economist at ANZ Bank. “Trump’s tariff plan will likely cause job losses in China because of technological progression,” Yeung wrote in a note Tuesday. “China’s immediate issue is unemployment due to AI and robot adoption rather than a decline in exports,” he said — and this worker displacement “will reduce household income and private consumption, at least initially.” A look back at tariffs in Donald Trump’s first term shows that China moved to accelerate its “shift from low-value manufacturing sectors to higher-value sectors,” Yeung wrote. Workers transitioned to emerging industries like software development. This time, authorities are prioritizing advanced technology and “leveraging the momentum of homegrown AI,” he said. That’s where the job market comes in. |