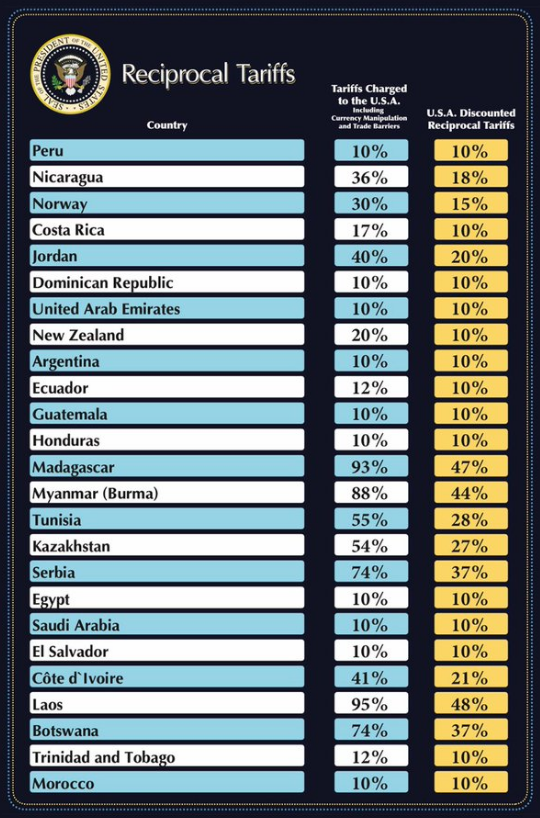

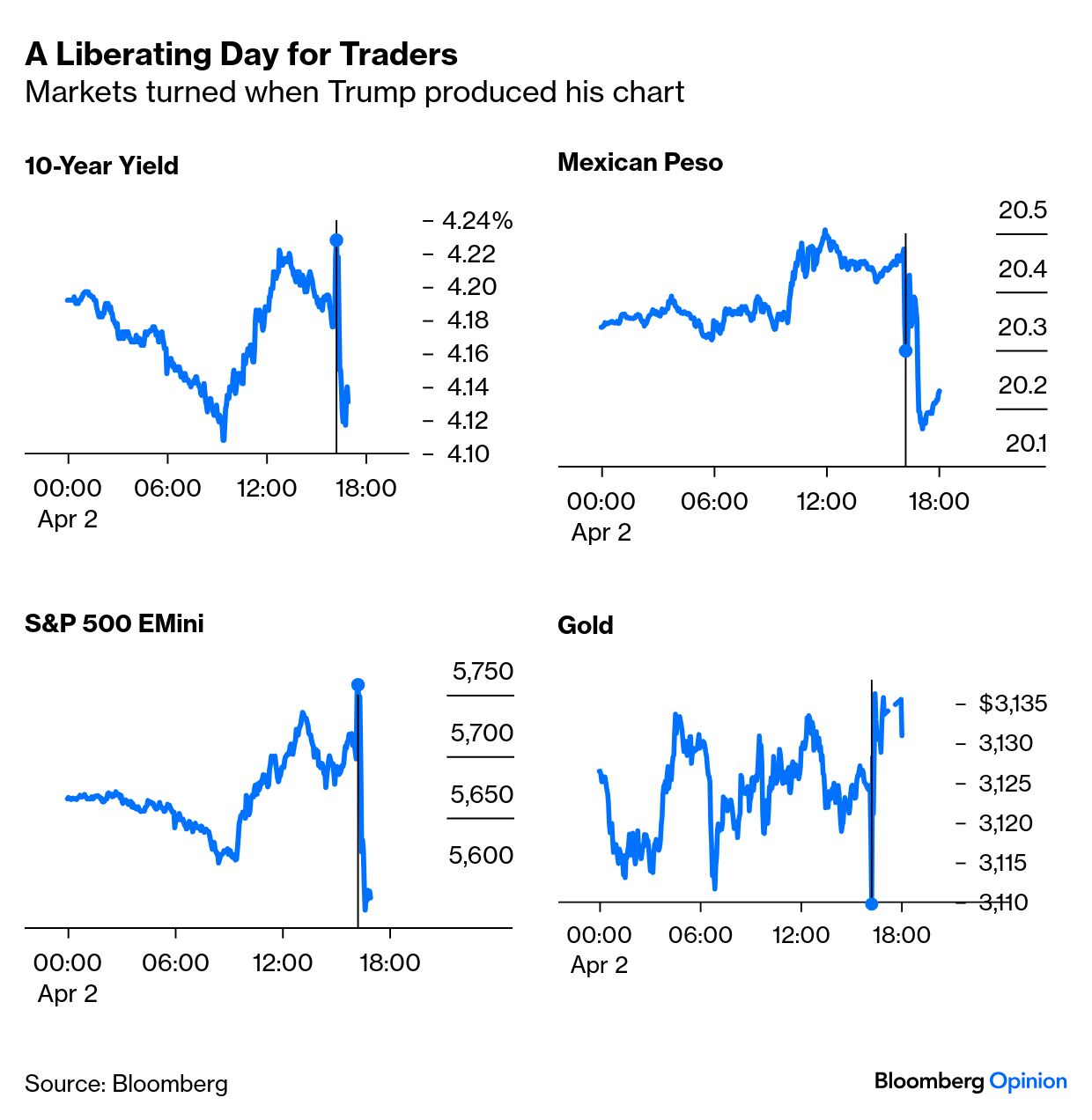

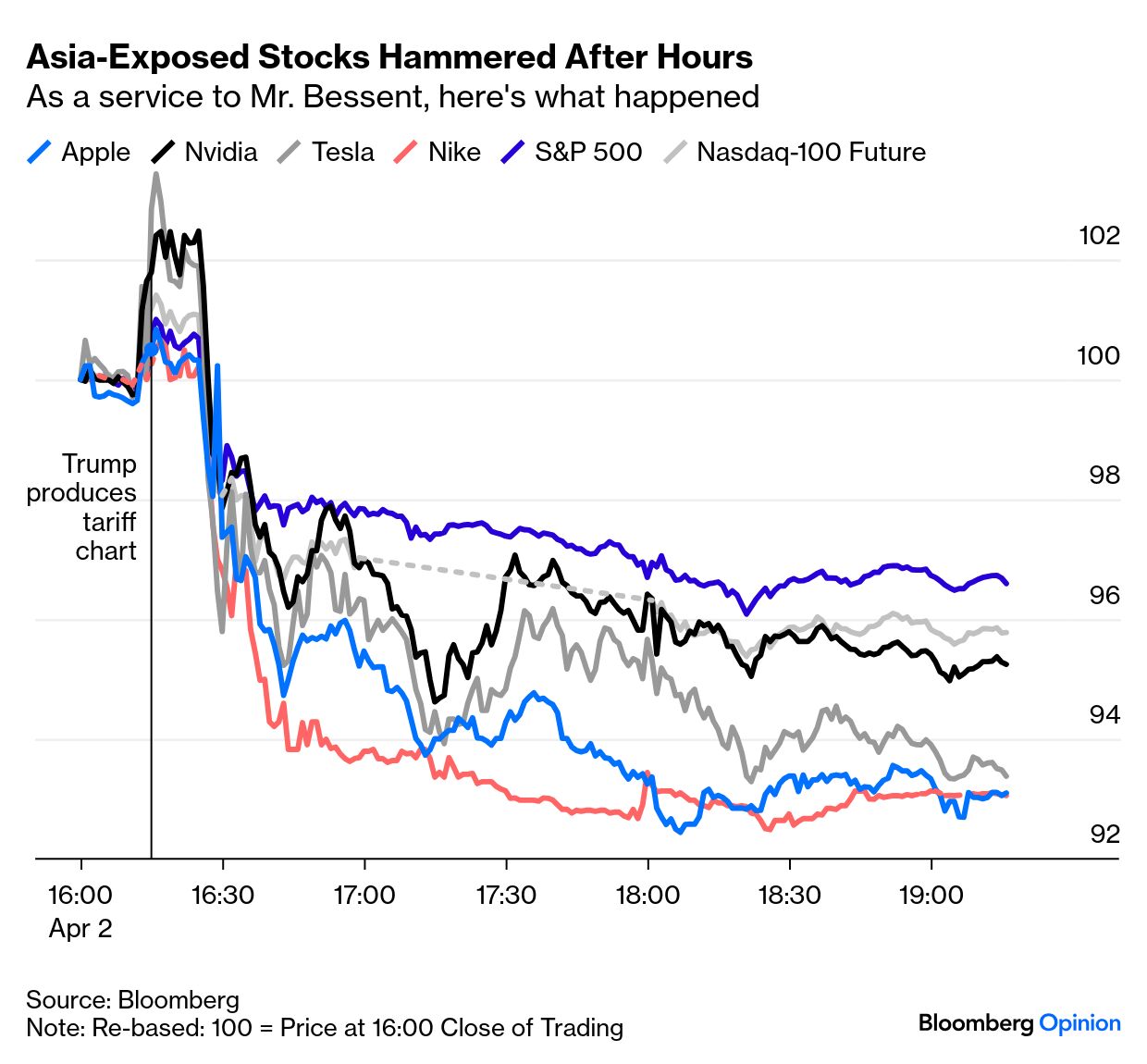

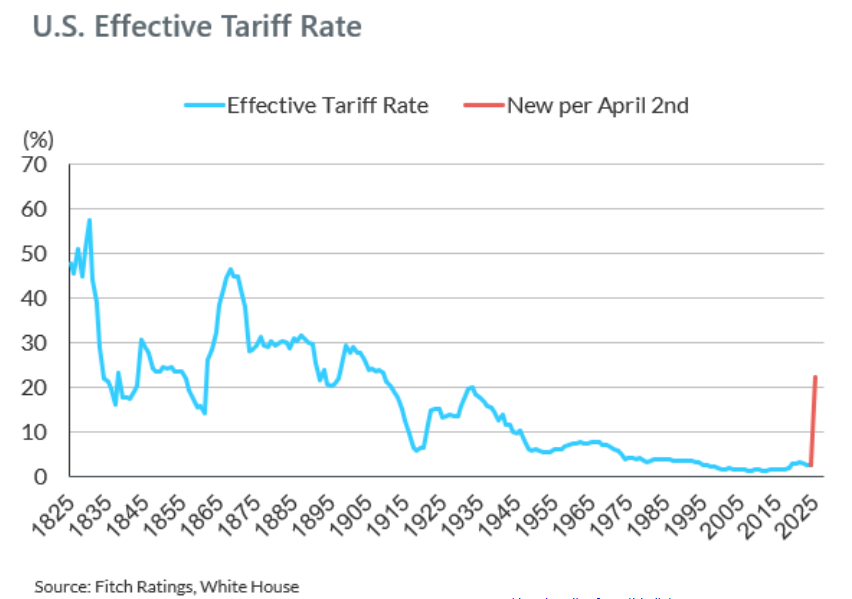

| The most immediate response to Donald Trump’s Liberation Day tariff announcement must be to channel another son of Queens. As John McEnroe once said to a Wimbledon umpire: “You can NOT be serious!” The main headlines are bullet-pointed above. The official White House fact sheet can be found here. The tariff rates that the president chose to announce in the style of a game-show host appeared on this chart: The market reaction was extraordinary, if unsurprising. As Trump started his speech with the blanket 10%, there was a tentative reaction that the tariffs would be more lenient than feared. Once he produced his chart to show the “reciprocal” levies on top of that, the exodus from risk was dramatic. At least the Mexican peso, spared any new levies, could stage a rally: Asia has come out far the worst. The biggest victims in the US are the companies most-exposed and that source a lot of their products from there, such as Apple Inc. and some of its Magnificent Seven brethren, or Nike Inc., which makes many of its sneakers in Vietnam. Scott Bessent, the Treasury secretary, told Bloomberg that he’d learned never to look at after-hours trading, and he had a point. But an after-hours selloff like this is hard to ignore: It’s hard to call this an overreaction, but how to describe all of this? Jean Ergas of Tigress Capital Partners said this week that it wasn’t “rebalancing” trade: “This is verticalizing the US economy!” That appears to be right. Tariffs at these levels would turn America into its own economic island, trading only with itself. Horizontal links with the rest of the world are out. Yes, the globalized status quo isn’t working, but it’s difficult to see how this will be any better. Clarity is still lacking — even excluding the possibility that some of these rates are never levied after a few days of negotiation — but back-of-envelope math suggests that this is even bigger than the Smoot-Hawley tariffs at the beginning of the Great Depression. Omair Sharif of Inflation Insights LLC calculates as follows: I looked at imports from 50 countries shown on the White House chart. Together, they made up 68% of total US imports in 2024. Applying the tariff rates shown on that chart and assuming a flat 10% on the remaining 32% of imports gets you a weighted average tariff rate of 23%. We’ll likely end up somewhere between 25% and 30%. Note that this would be higher than the average effective tariff rate of about 20% in 1933 under Smoot-Hawley.

Fitch Ratings’ Olu Sonola reckoned the new effective tariff rate at 22% (up from 2.5% last year). That would be the highest since 1910. Sonola described the announcement as a “game changer” for the US and the rest of the world: “Many countries will likely end up in a recession. You can throw most forecasts out the door, if this tariff rate stays on for an extended period of time.” Alternatively, if we look at this package as a revenue-raising measure, then it should raise some $600 billion — if all trade continues as before. Dan Clifton of Strategas Research Partners said: “Trump said he wanted $600 billion and he got it. This represents 2.2% of GDP and twice the size of the largest tax increase in modern US history.” Recall that three months ago, everyone was looking forward to tax cuts. A further problem is the bizarre mathematics behind the estimates of countries’ overall tariffs, which include currency manipulation and non-tariff trade barriers. No explanation of how these can be combined into one tariff rate has been offered. Peter Tchir of Academy Securities commented that this “seems like the sort of thing you turn in when you watched college hoops all weekend and need to get the assignment turned in or you fail.” He drills into it: Currency Manipulation as a percentage seems difficult to calculate? What portion of a currency move is “manipulation” as opposed to market forces? Trade barriers, includes VAT? Currency restrictions (or is that included in manipulation?) No idea. Average Tariffs. Presumably there is some average tariff level. Is it trade weighted? Is there any weighting at all? Or is it simple average? 20% on eggs and 5% on autos is 12.5%? For tariffs attached to quotas (which many are), is it based on the average or the highest? There is no way to tell.

This is not a serious way to proceed, and it’s insulting to put such huge restraints on allies’ trade with such weak explanation — particularly in a speech that accuses the rest of the world of “raping and pillaging” the US. Under the common understanding of reciprocity, trade negotiators would go through product by product (involving many difficult definitions), and make sure that each individual tariff is balanced. That would have been very difficult, but would appear fair. This appears arbitrary, because it is. Presenting it as “kind” adds salt to the wound.  Japan’s stocks plunged on news of 24% tariffs. Photographer: Kiyoshi Ota/Bloomberg World leaders will have to keep their cool better than McEnroe did. But taken together, this isn’t the action of serious people, even though its consequences could be very serious indeed. |