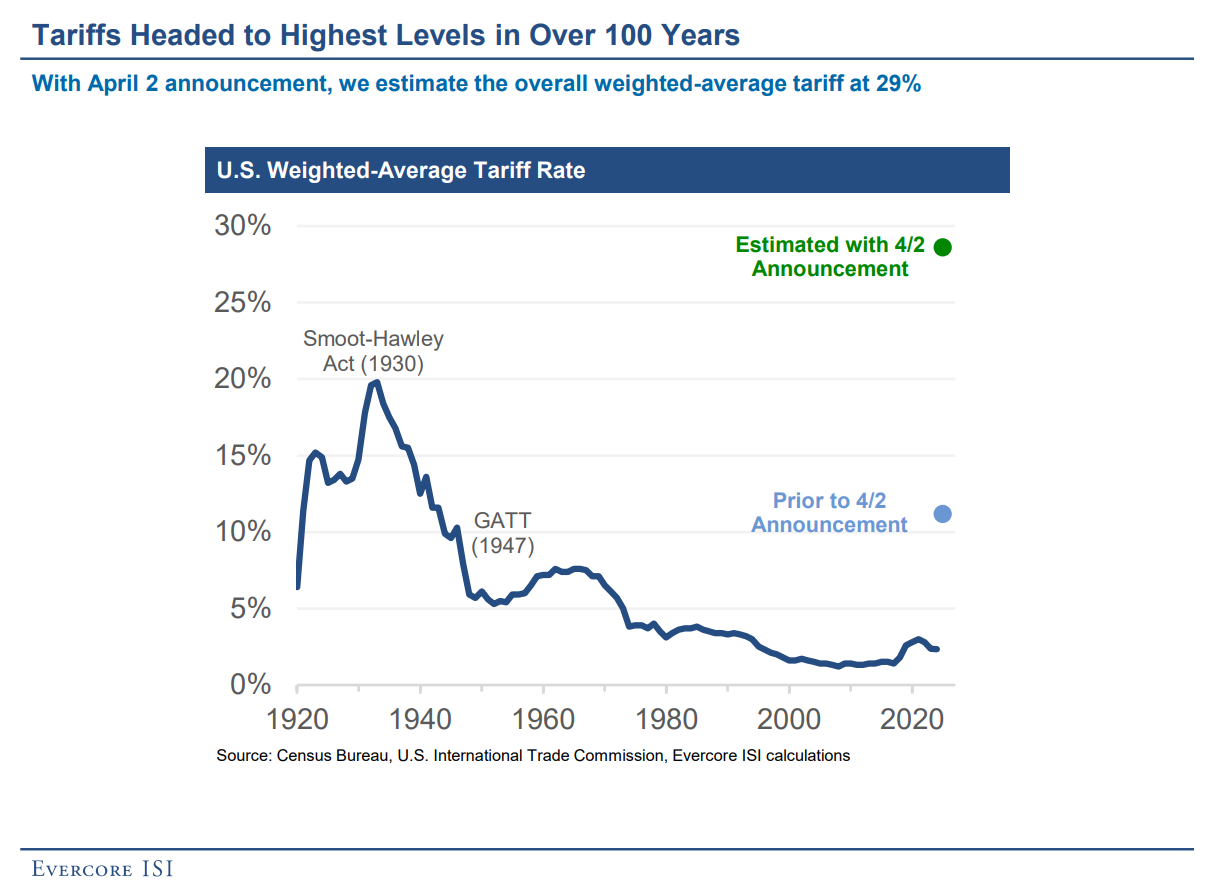

| I’m Chris Anstey, a senior editor in Boston. Today we’re looking at Washington’s new reciprocal tariffs. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X via @economics. And if you aren’t yet signed up to receive this newsletter, you can do so here. Trump sought to wind back the economic clock of the US on Wednesday, to a time when it was a “tariff-backed nation” that was able to forgo income taxes and was brimming with wealth. Far from sharing the orthodox interpretation of the 1930 Smooth-Hawley Tariff Act as a major contributor to the economic pain of the Great Depression, Trump said it was an effort to “save our country.” In fact, the depression “would have never happened if they had stayed with the tariff policy,” he said. With that conviction, Trump unveiled in a White House Rose Garden ceremony a package of tariff hikes dwarfing even those of 1930. Nations were assigned rates ranging from near-50% on some Southeast Asian economies to a “baseline” rate of 10% for the UK, Brazil, Turkey and others. China’s 34% reciprocal rate will combine with a previous 20% surtax to make 54%, while European Union goods face a new 20% levy. The figures are complicated, in the context of sectoral tariffs either in place or forthcoming on products including automobiles, aluminum and steel. Bloomberg Economics estimated the announcement could, with a previous auto-tariff hike, add around 16 percentage points to the average US tariff rate. Evercore ISI calculated the average rate getting to 29%, compared with the Smooth-Hawley level of 20%. Whatever the final tally, it’s much higher than most economists and investors anticipated. That was seen in the immediate nosedive in equities. The bond market started to price a small chance of four Federal Reserve interest-rate cuts this year, though the inflationary impulse from tariffs puts policymakers in a tough spot. Joseph Brusuelas, chief economist at RSM US LLP, cautioned that the moves raise the probability of a recession, in a view likely to be shared by many in coming days. For other nations, Trump’s moves forbode major hits to exports, and escalation pressure on governments to bolster domestic demand in their own nations. In the US, too, stimulus will be needed, and Treasury Secretary Scott Bessent said on Bloomberg TV that his main focus will be working with Congress to extend and expand the 2017 Trump tax cuts. As for trade deals to negotiate down the new tariff rates? He indicated the administration would “let things settle for a while.” Meantime, he warned that “I wouldn’t try to retaliate,” and hinted that Trump may take yet further action. “This is the high end of the number barring retaliation,” he said of the new tariff rates. Don’t Miss the Latest Trumponomics Podcast | Host Stephanie Flanders, Bloomberg’s head of government and economics, is joined by Martin Wolf, chief economics commentator at the Financial Times and author of several books, most recently The Crisis of Democratic Capitalism. They discuss whether the countries now in the firing line of America’s tariffs (and primed to retaliate in kind) should have seen Trump’s trade war coming. They also explore how the trade imbalances the US administration is targeting aren’t an accident and can potentially lead to an unstable global economy. Listen here and subscribe on Apple, Spotify, or wherever you get your podcasts. The Best of Bloomberg Economics | In his confirmation hearing to become Treasury secretary, Scott Bessent suggested that 40% of the price impact of a tariff hike would be offset by an appreciation of the dollar. In the case of a 10% universal import duty, “the currency appreciates 4%, he said. That may be too low, Evercore ISI says. “Our baseline assumes 50%” in cases where there isn’t one-for-one retaliation, the research group’s analysts including Krishna Guha wrote in a note Wednesday. But that’s when it comes to modelling. The curious thing is that the dollar has actually weakened as Washington stepped up tariffs. The group says that the severity of the tariffs, and uncertainty around them, may be causing this unexpected exchange-rate reaction. “Beyond a certain point, tariff escalation may have a larger relative effect on the US than the rest of the world,” given that the Trump administration moves affect all of US trade, but in other countries only a portion of their trade is affected, the team wrote. The deteriorating US growth outlook has taken down US yields and stock — consistent with reduced demand for dollars, they wrote. |