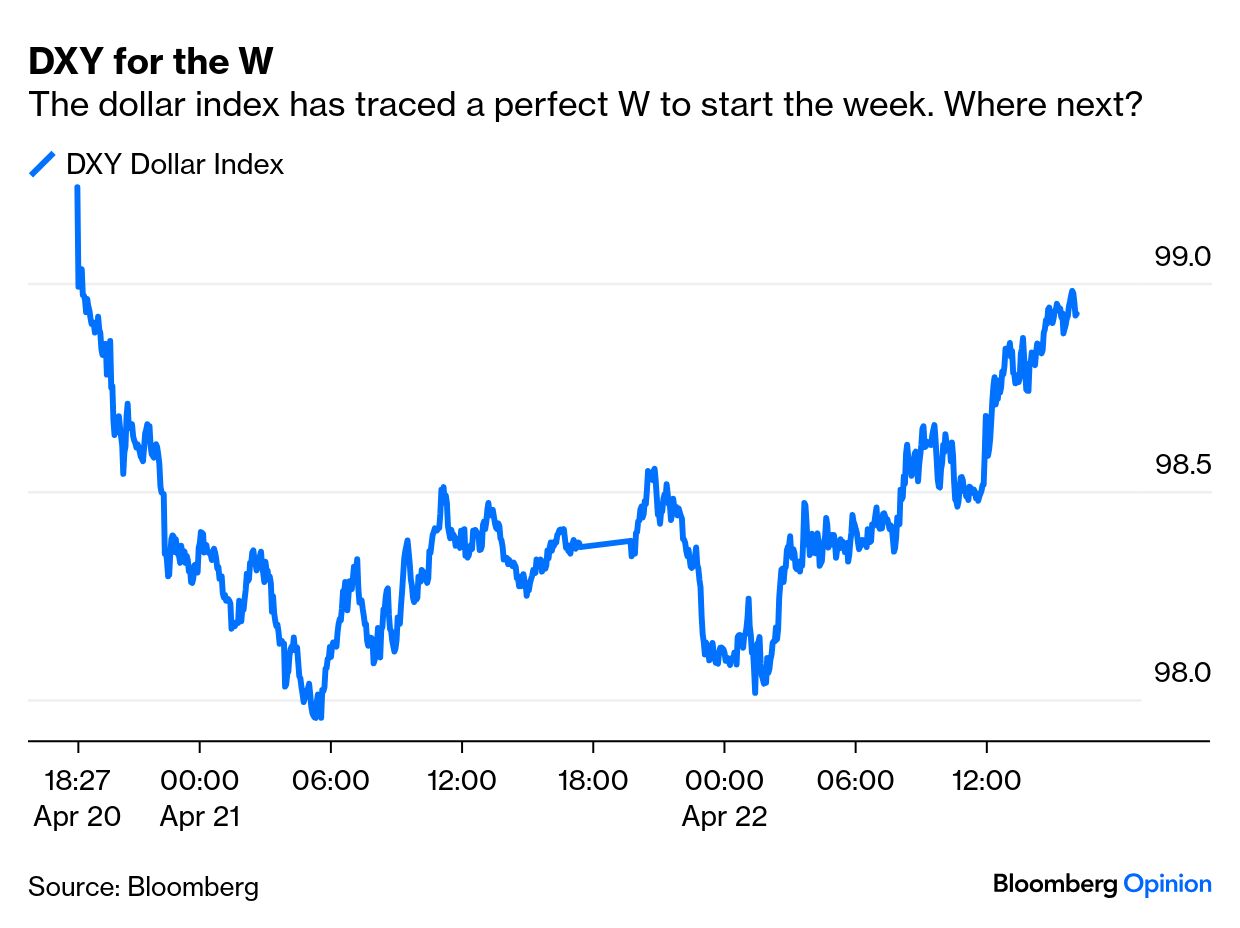

| Putting the brief Powell tempest to one side, is this a turning point for the dollar? And if so, in which direction? This week has already brought plenty to support any narrative you wanted. The DXY dollar index has spent two days sketching out a broad W to end almost where it closed on Friday. I drew this chart just before the Powell comments: It’s conceivable that this is a turning point, but it could easily be in either direction. We’ve explored the logic behind the fear of a drawn-out fall for the dollar and US assets at length. The rest of the world is heavily “overweight” the US, and the effect of pulling money back home could lead to a self-fulfilling reversal of US exceptionalism. But it’s ever-important in markets to guard against our innate tendency to extrapolate any trend before us into a straight line into the long-term future. Adam Parker, who heads Trivariate Research, makes the point that near-term price movement has typically impacted sentiment: The US markets have been performing worse than every major market so far this year. After the fact, many investors are now saying this is the beginning of a new long-term trend. We disagree, and our view is that this dynamic of US underperformance likely lasts less than one year.

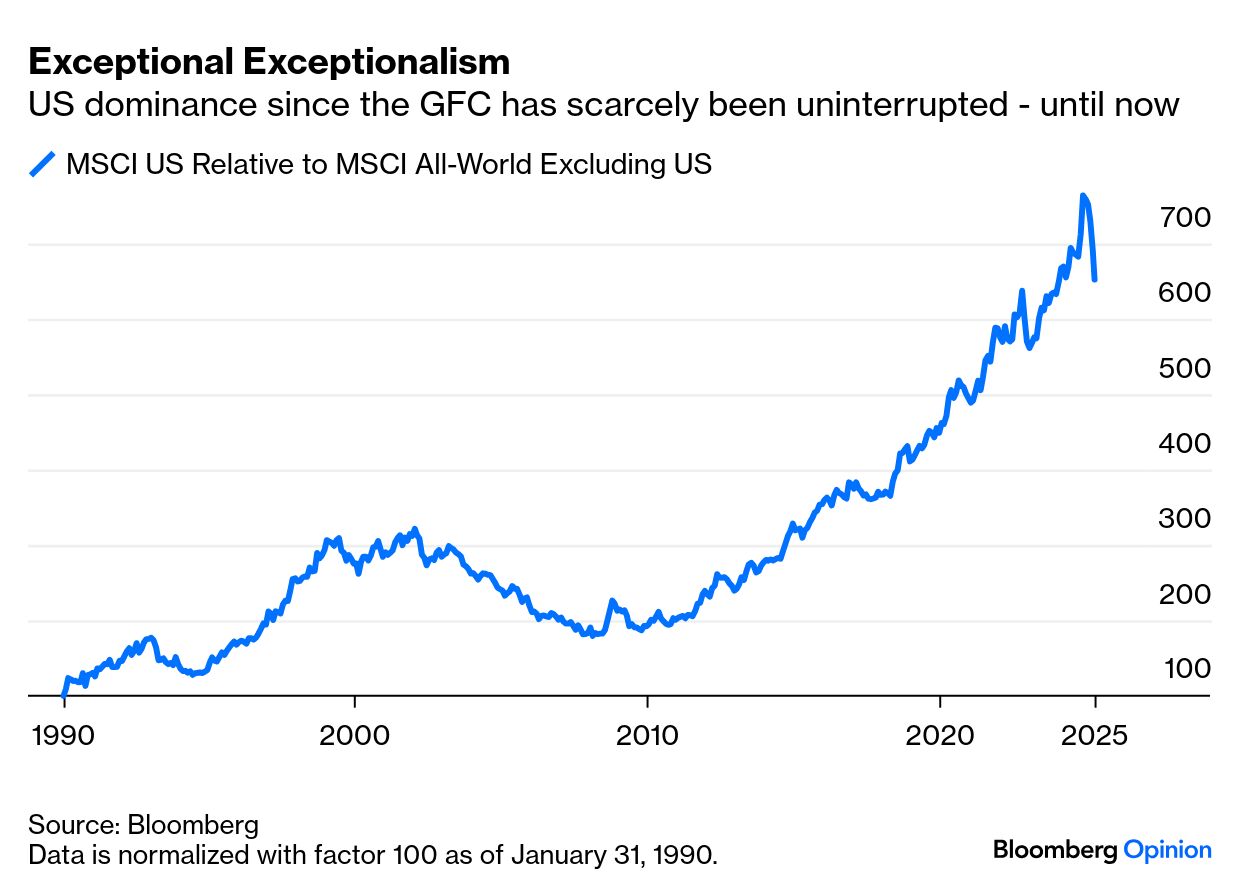

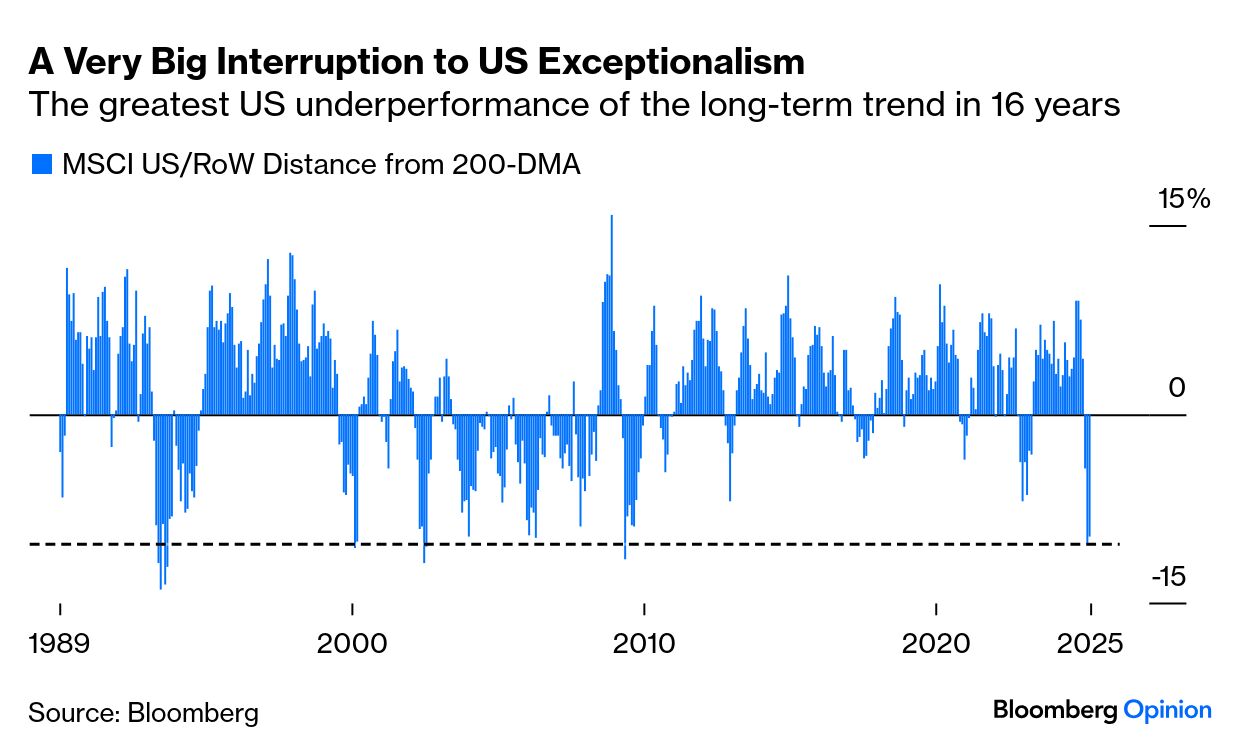

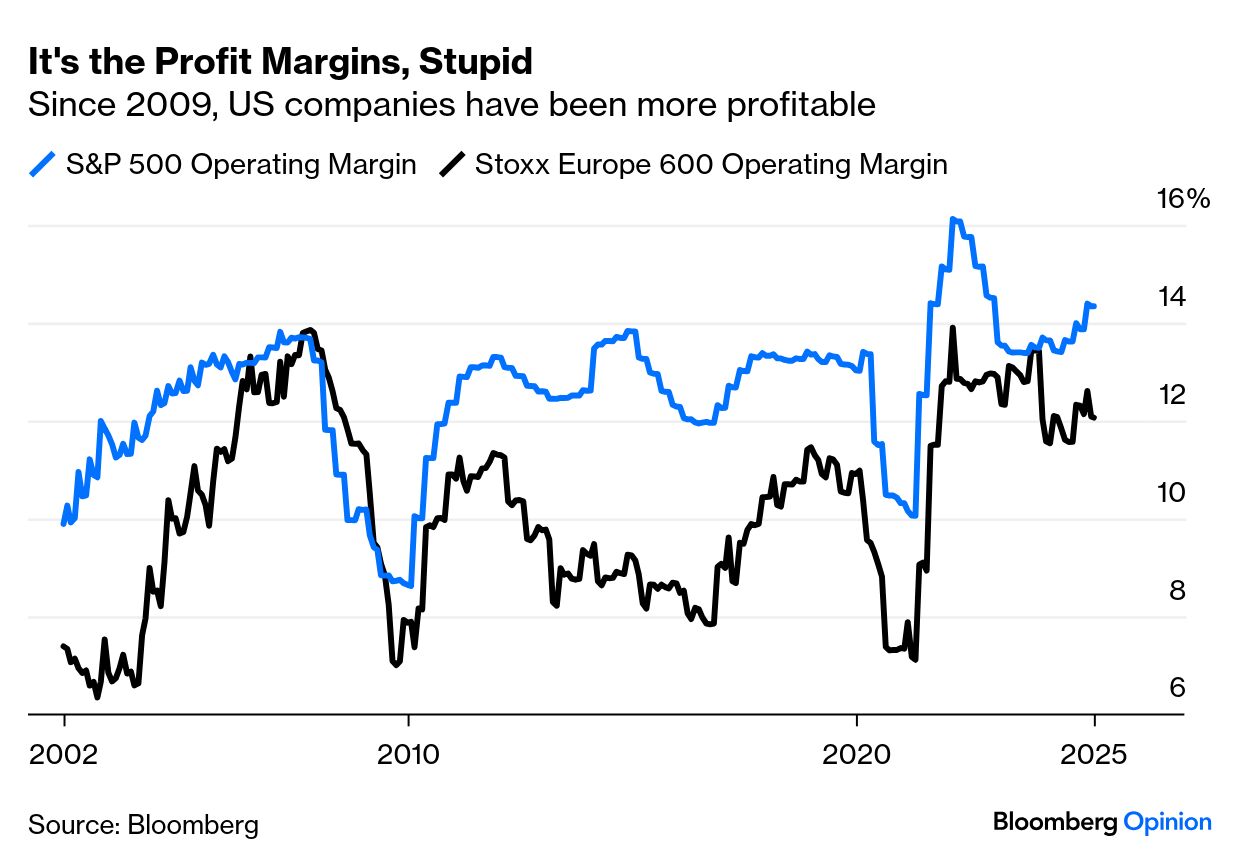

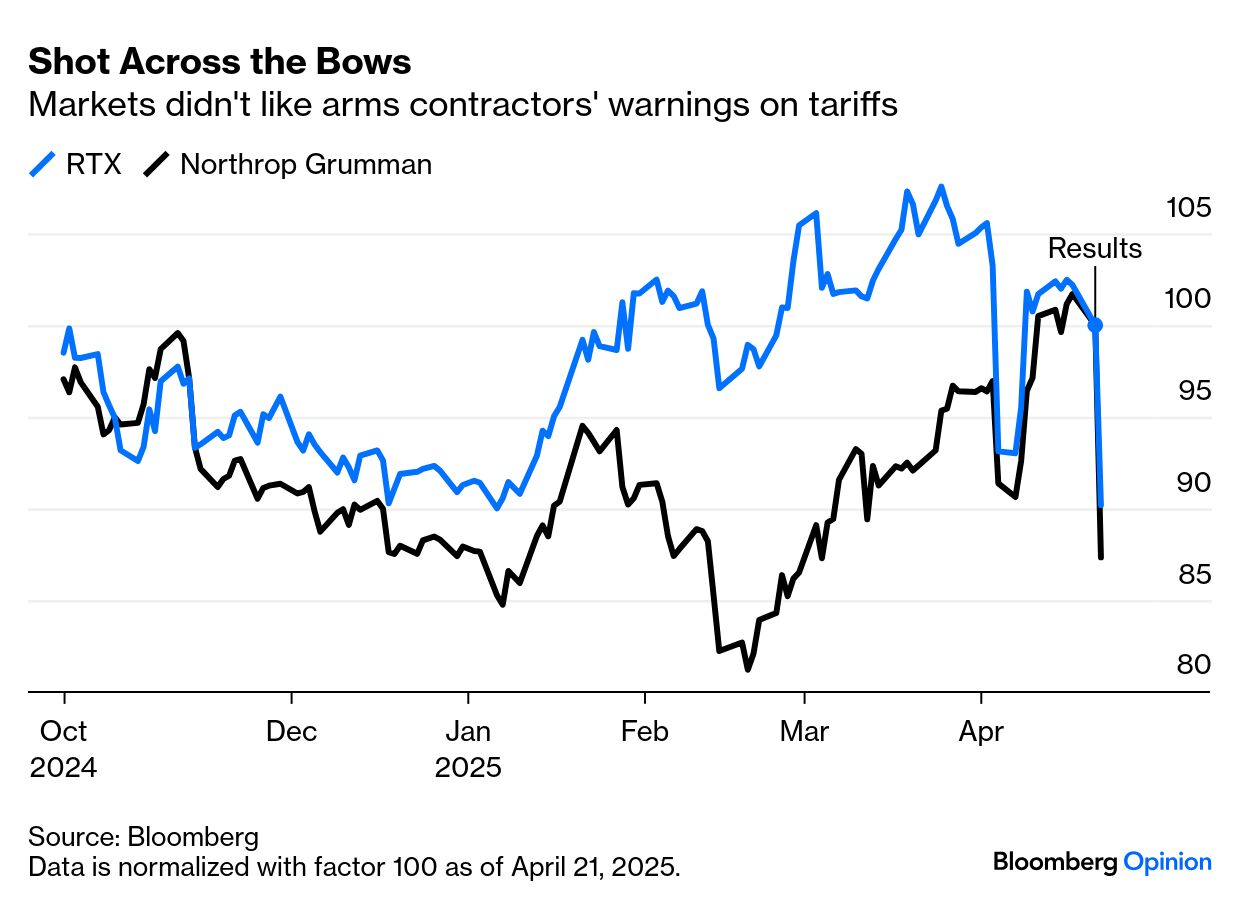

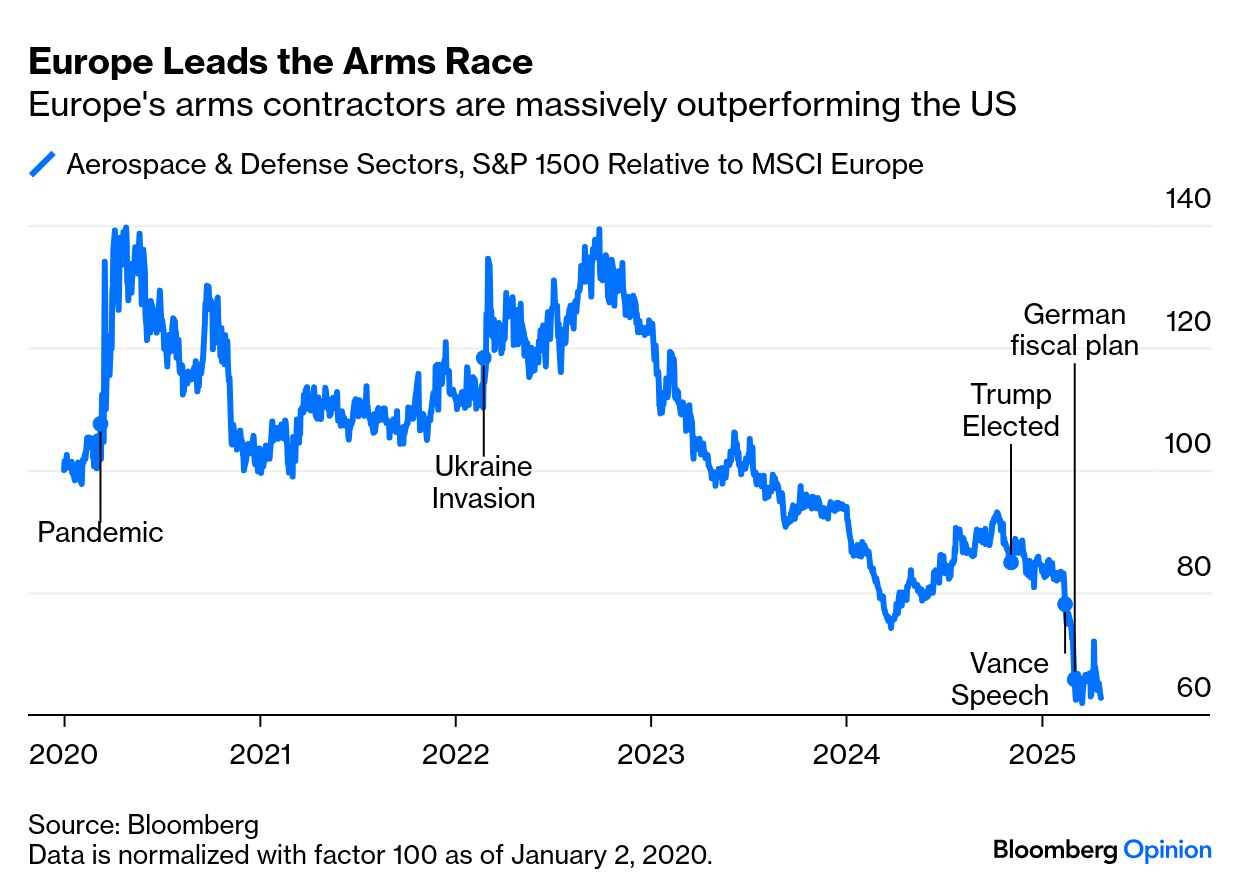

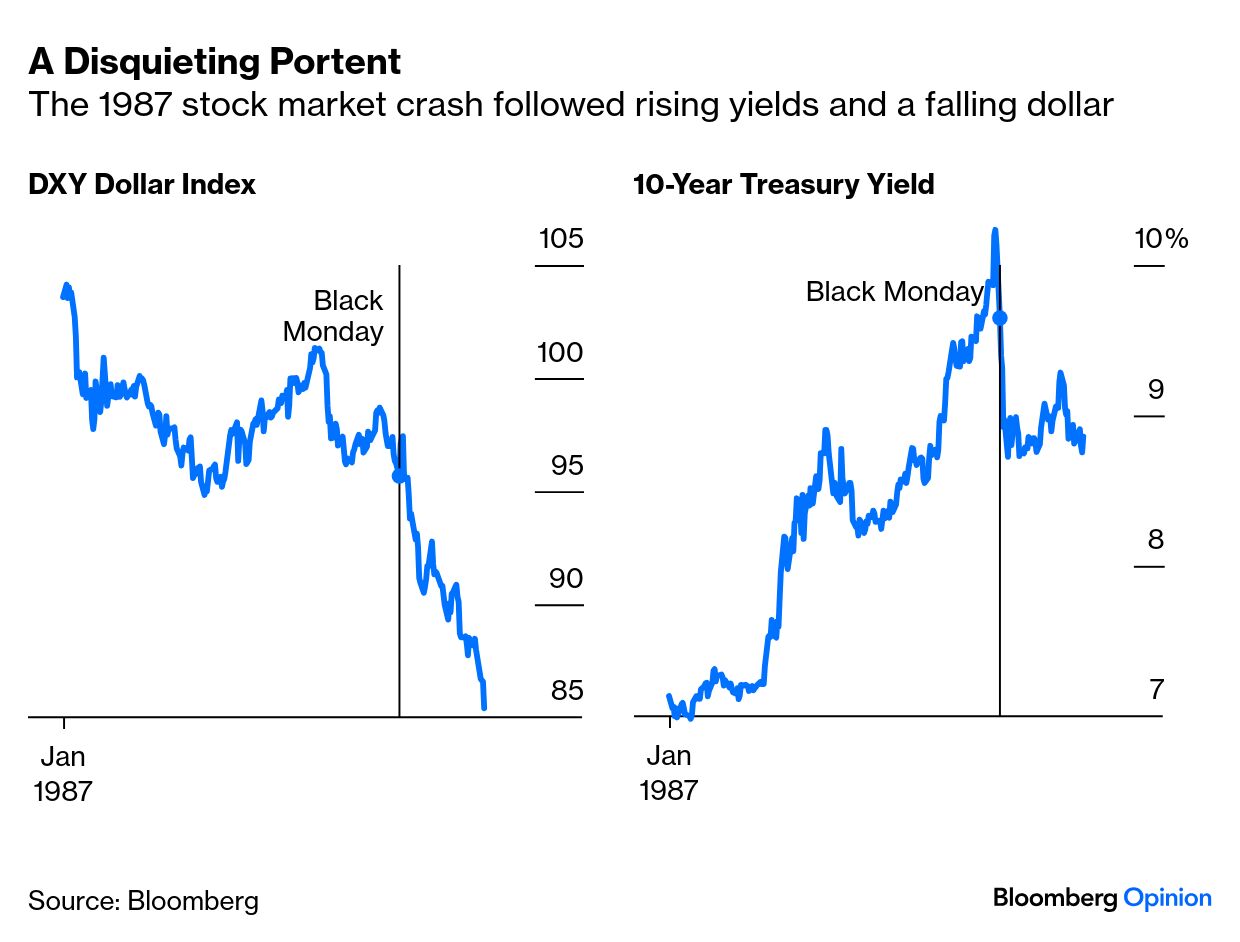

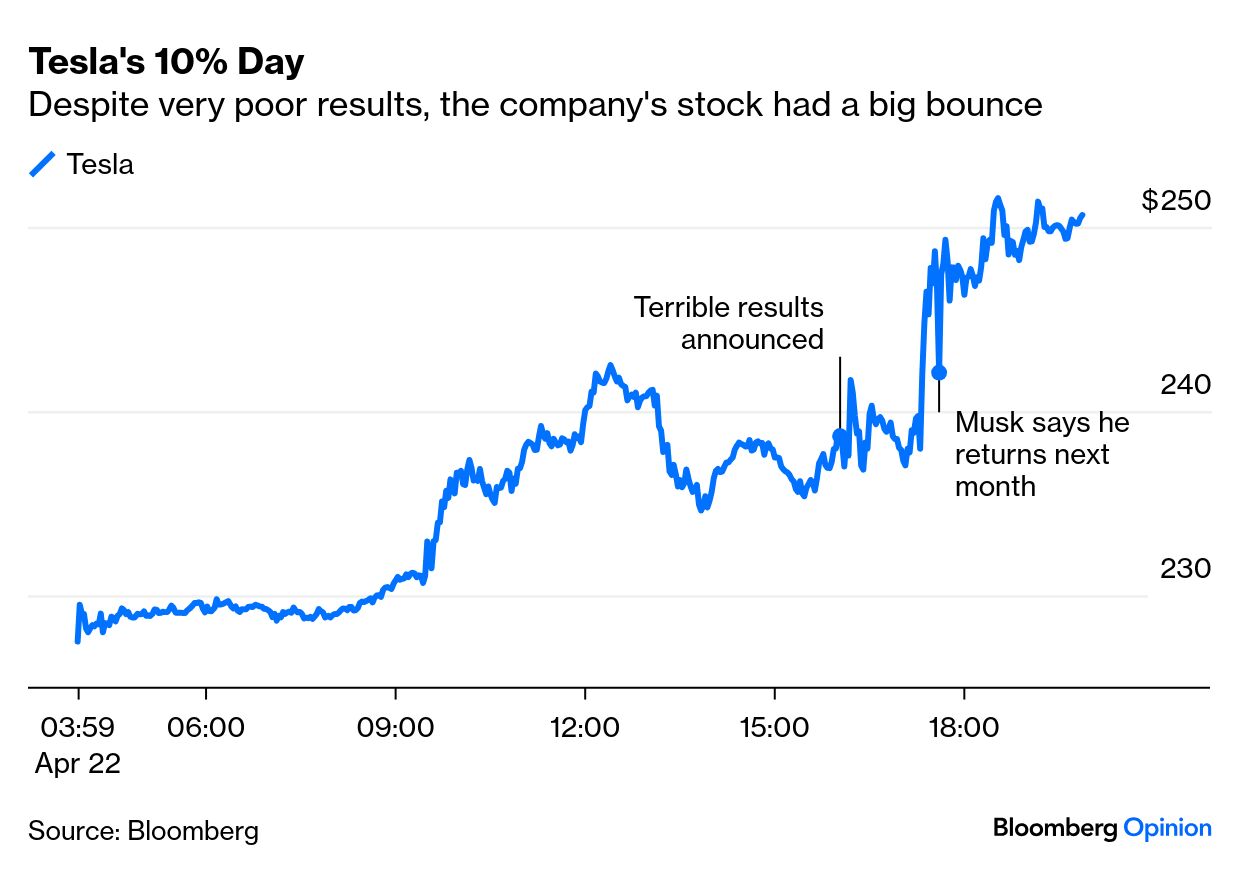

There are a number of points to his analysis. First, the dollar isn’t that weak. It’s had a sharp fall, but it remains close to its average for the last five years (and if we take inflation into account, it’s still almost as strong as in 1985, when central banks felt it necessary to coordinate to weaken it): Further, US exceptionalism was due a correction. This is how MSCI’s index for the US has performed compared to the rest of the world since 1990: Terminal users might press the button to open this chart in G, so you can view it on a log scale. Even then, the length of US dominance and the brutal way it’s been interrupted stands out. To view this data another way, this is how much the US/Rest of the World ratio has varied from its own 200-day moving average over this time. It’s now at the biggest downward departure from the long-term trend in 16 years: It’s the persistence of US outperformance since the Global Financial Crisis that stands out as unusual, more than the current interruption. But this does look like a massive bout of underperformance by standards that go back decades. By Parker’s reckoning, since World War II only the 1972-74 and 1976-78 stagflation episodes and the 1987 crash have been worse. So it’s reasonable to doubt that it will go on much longer. In part, the US stock market has been so exceptional because money has been flowing in from investors using it as a piggy bank. But there’s also a fundamental reason: US companies are more profitable. Here is how operating profit margins compare for the S&P 500 and the Stoxx Europe 600: According to Parker, if tariffs were to cause profit margins to shrink back to 2018 levels, “that could cause enough multiple contraction for the US market to continue to underperform.” That’s not a given. It’s certainly possible, but it would be remarkable if the administration were to persist with the a policy doing that much damage. It’s also not an issue that can be resolved quickly. In the last quarter, tariffs caused many purchases to be brought forward, so this earnings season won’t be a good guide to their eventual impact. To a greater extent than usual, how CEOs predict the future matters more. The defense groups RTX (formerly Raytheon) and Northrop Grumman both announced results better than expected Tuesday, but briefed that they expected tariffs to affect their profits. This is what happened next: (Incidentally, the way the US arms manufacturers have counterintuitively lagged their European counterparts since the invasion of Ukraine is stupefying): Another reason for optimism, Parker points out, is the US concentration in companies well positioned to benefit from the growth trends of the next decade, such as artificial intelligence, the power technologies to fuel it, and life sciences. One final concern is the way that this selloff has happened. Away from the stock market, there’s been a rare combination of rising bond yields and a falling dollar. As higher yields generally attract money into a currency, that’s a bad sign that confidence is dwindling, and it can signal trouble for equities. For a potent example, one reader pointed that the great Black Monday crash of 1987 was preceded by just that combination: If the divergence persists much further, it will provide more evidence that investors really do require a bigger risk premium to invest in Treasuries. But overall, Parker’s arguments are well taken. There’s good reason to fear that the policy missteps of the last few months have ended US exceptionalism, but it’s way too soon to be sure.  Anywhere but here. Photographer: Roberto Schmidt/AFP/Getty In a masterpiece of parliamentary disdain, a minister under pressure to resign once heard this statement from the Westminster back benches: “I have nothing against his wife and children, but I think he should spend more time with them.” Similarly, investors don’t have anything against Tesla’s workers and executives, but they think that Elon Musk should spend more time with them. It’s hard to find any other explanation for Tuesday, when Tesla Inc. announced objectively awful results after the market closed — bad in absolute terms and worse than expectations — and its stock exploded upward 90 minutes later when CEO Musk told the earnings call that he’ll return to spend most of his time at the company next month: Liam Denning has taken a typically ruthless scalpel to the results. The company isn’t even prepared to say it will return to growth this year. Musk’s big message on the call was to ignore electric vehicles (which already exist), and instead focus on robots and robotaxis (which don’t, at least in a form that can safely be sold to the public). Musk’s return is also not full time, as he said he expects to spend a day or so per week at DOGE for the rest of Trump’s term. And he still sounded to me (and Liam) as though he was far more preoccupied with the government than with the great company he runs. Despite the share price reaction, analysts’ immediate views were negative. The market response shows that a lot of very bad news was in the price, and that the CEO’s loss of interest for the last quarter was a real problem. If in five years we’re taking robotaxis and being waited on by robots, Musk will get the last laugh. He may find that getting there is a full-time job. |