| The great boxer Mike Tyson and once said that everyone has a plan until they’re punched in the face. Similarly, the Trump administration had one for rebuilding the world economy with tariffs. It’s been a rough first round. The plan was Stephen Miran’s A User’s Guide to Restructuring the Global Trading System, which must have been the most-viewed document by the financial world over the last six months. Stunningly ambitious, it helped earn its author a gig as chairman of the president’s Council of Economic Advisers, birthed the concept of the “Mar-a-Lago Accord,” and was widely taken as the road map for Trump 2.0’s bid to reshape the world using tariffs. Approaching the administration’s 100-day mark next Tuesday, the “User’s Guide” reads differently now. Some of it has come to pass, Trump has deviated sharply from important recommendations, and certain assumptions now look tenuous at best. To help navigate where the global trading system is heading, it’s a good time to pull over and return to the map. European Rearmament Countries that want to be inside the defense umbrella must also be inside the fair trade umbrella… Suppose the US levels tariffs on NATO partners and threatens to weaken its NATO joint defense obligations if it is hit with retaliatory tariffs. If Europe retaliates but dramatically boosts its own defense expenditures and capabilities… it will have accomplished several goals.

This is coming to pass — with the key difference that the administration needed only to threaten tariffs, as this was combined with outright hostility to Ukraine and western Europe and an intent to annex Greenland. If Europe has already decided that it cannot rely on US protection, as seems likely, then that makes life much easier for the US — but also that the hope to use the defense umbrella as an inducement is unlikely to work. Instead, allies are responding to the notion that commitments once freely given must now be paid for by seeking new allies. There’s a Risk That Long Yields Could Rise If an expected change in currency values leads to large-scale outflows from the Treasury market, at a time of growing fiscal deficits and still-present inflation risk, it could cause long yields to rise. This risk will be somewhat compounded if inflation remains elevated.

Miran expected the currency to rise to offset the imposition of tariffs — which he argued would have the effect of putting the burden on to the tariffed country. But he acknowledged that it might not, and that if the dollar were to weaken, then continuing inflation worries and the high budget deficit would put pressure on Treasuries. That has happened so far. The good news is that inflation numbers have improved in the last few months, but they don’t yet take account of tariffs. Proceed Gradually To help minimize uncertainty and any adverse consequences of tariffs, the Administration can use credible forward guidance, similar to what is used by the Federal Reserve across a range of policies, to guide expectations. The US Government might announce a list of demands from Chinese policy — say, opening particular markets to American companies, an end to or reparations for intellectual property theft, purchases of agricultural commodities, currency appreciation, or more. The US can proceed to gradually implement tariffs if China does not meet these demands.

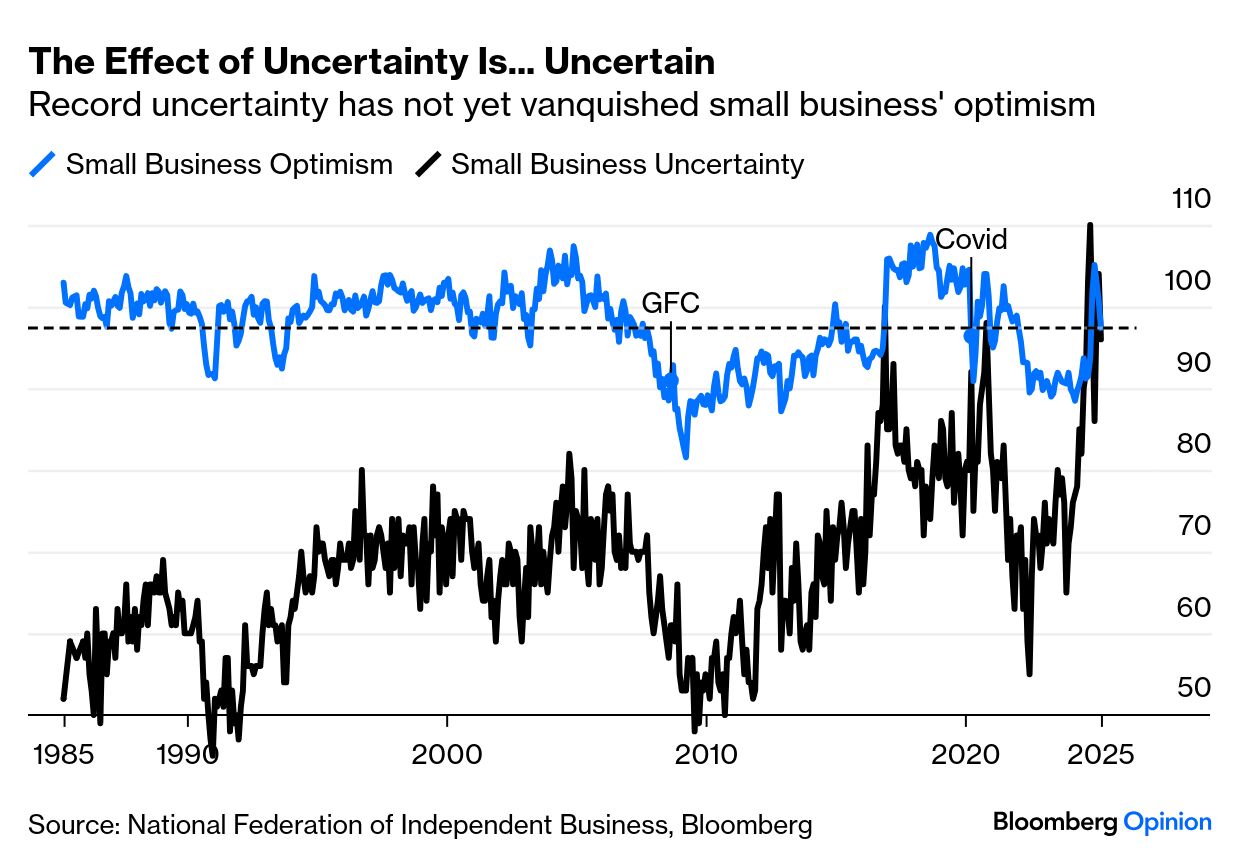

Miran’s precise suggestion was to raise tariffs by 2% each month until an agreement was reached. That would have worked very much better than the chosen strategy of hiking the tariff on China to 145% in very short order. The exasperating twists and turns of the last three months mean that any forward guidance cannot be credible. That has had a massive effect on uncertainty, even for the administration’s natural constituency of small business owners. The National Federation of Independent Business has been polling on this for decades, and its members have never before felt so uncertain — but it’s important that their overall optimism still seems relatively healthy: It’s not yet clear how damaging this will be, but the administration has taken a big risk by acting in such an unpredictable way. Don’t Upset the Markets President Trump has shown repeated concern for the health of financial markets throughout his Administration. That concern is fundamental to his view of economic policy and the success of his presidency. I therefore expect that policy will proceed in a gradual way that attempts to minimize any unwanted market consequences.

The White House is doing its best to look as unbothered by market selloff as it can. Reversals on the Fed and on “reciprocal” tariffs show that there is indeed a “Trump Put,” but the level to which the market must fall before it’s activated is much lower than many had assumed. Tariffs Aren’t Inflationary Tariffs provide revenue, and if offset by currency adjustments, present minimal inflationary or otherwise adverse side effects, consistent with the experience in 2018-2019.

This looks increasingly like over-learning the lesson from the very different environment of the brief 2018 trade war. That time, as Miran said, the tariffs were imposed gradually and with due warning, against a backdrop of placid inflationary pressure. They’re much higher now, and there is anxiety among the population about another pickup in prices. Demand for Treasuries Is Eternal Much (but not all) of the reserve demand for [dollars and Treasuries] is inelastic with respect to economic or investment fundamentals. Treasurys bought to collateralize trade between Micronesia and Polynesia are bought irrespective of the US trade balance with either, the latest jobs report, or the relative return of Treasurys vs. German Bunds.

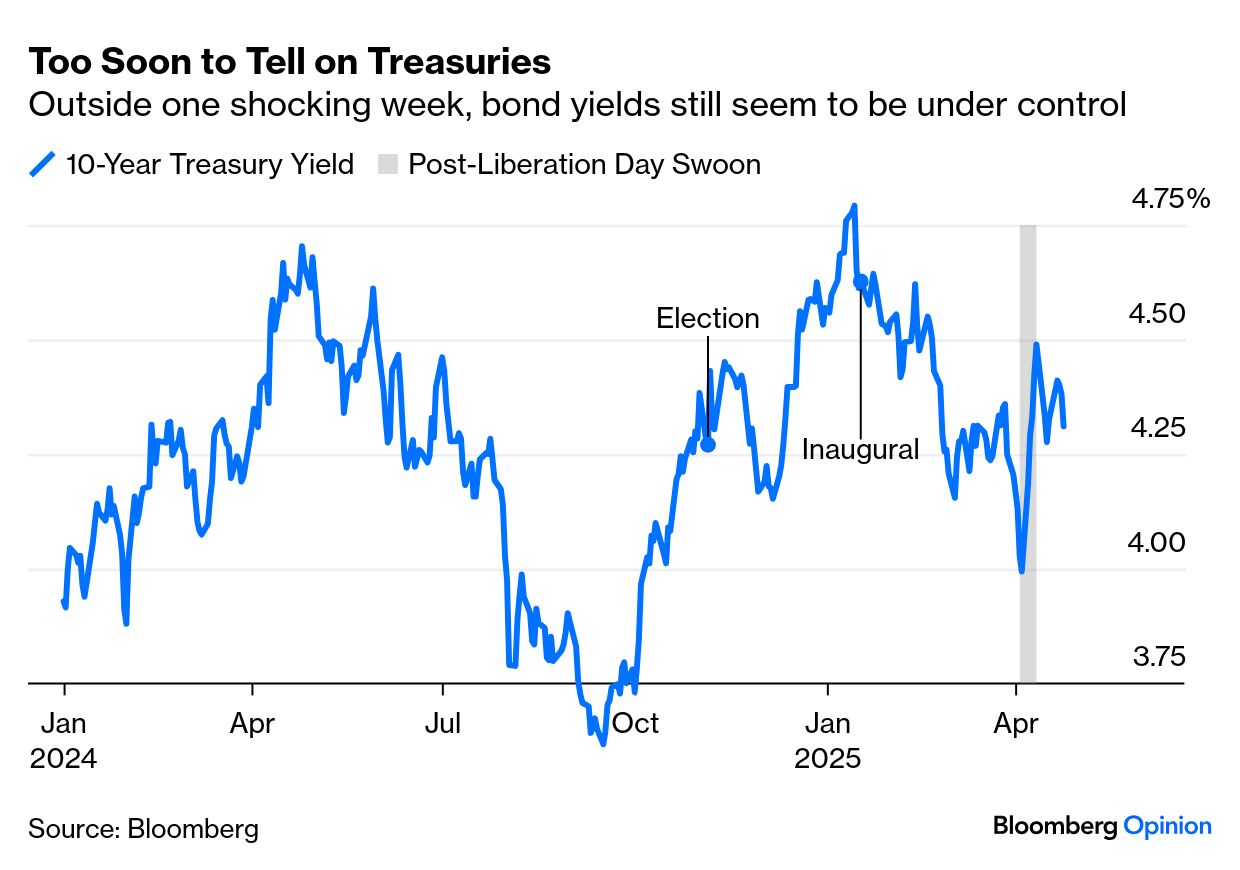

Demand may not be as inelastic as all that. The week after Liberation Day saw a combined run on both the dollar and Treasuries, which drove the 10-year yield up by the most in a week in more than 20 years. It’s a sign that foreigners have suddenly become much more discerning in their demand for US debt. That said, apart from one shocking week, the Treasury trend is still unclear: Foreigners Will Pay for the Privilege of Lending to the US Treasury can use the International Emergency Economic Powers Act to make reserve accumulation less attractive. One way of doing this is to impose a user fee on foreign official holders of Treasury securities, for instance withholding a portion of interest payments on those holdings.

This assertion is beginning to look very questionable. Effectively, the suggestion is that the US should charge foreigners a fee for the privilege of lending to Uncle Sam. Just this month has seen sharply increased interest in alternatives, such as German bunds, Swiss francs, gold, and even Bitcoin. If the US tries to charge a fee like this, the likelihood is that it will just stop the flow of funds into the US — and make it that much harder to fund the deficit. The US Can Beat China in a Game of Chicken Preventing retaliation will be of great importance. Because the United States is a large source of consumer demand for the world with robust capital markets, it can withstand tit-for-tat escalation more easily than other nations and is likelier to win a game of chicken... This natural advantage limits the ability of China to respond to tariff increases.

The game is still going on, but it looks at present like this is flat wrong. China retaliated swiftly, and amped up the pressure with extra measures such as blocking exports of rare earths. Trump’s rhetoric is already swerving away from the confrontation, saying he wants to be “nice” to China with a deal that lowers tariffs. The Chinese response is that tariffs have to come down first before talks can begin. It’s true that the US buys a lot from others. But this game will be won by the player who can absorb the most pain. That appears to be China, even though it also stands to lose more. This looks like it was a critical bad assumption, and the error has been magnified by the ham-fisted way in which tariffs were imposed. So where does this leave us? A hundred days in, Miran’s “User’s Guide” shows that the administration entered the conflict with an inflated view of its own strength, and that it has been handled more abruptly and aggressively than the architects of the policy wanted. The response so far has not been what was bargained for.  Maybe it’s time for a revised edition. Photographer: Tierney L. Cross/Bloomberg All of that said, the White House wanted a weaker dollar and has got it. Interest rates haven’t broken above their recent ranges, while lower oil prices very much help its agenda. Equities remain buoyed by good earnings results (most recently from Google-owner Alphabet Inc., which enjoyed a 6% bump in after-hours trading after beating expectations for profits and revenues). A Mar-a-Lago Accord of the kind envisaged in the “User’s Guide,” in which foreigners buy 100-year zero-coupon bonds from the US in return for staying under its security umbrella, now looks unachievable. If such a deal can be made by anyone, it needs to be negotiated with far more finesse than witnessed so far, and the counterparties need to be given good reason to believe that they can trust Washington. For the future, enough remains unclear that it would be unwise to make assumptions about where the dollar and Treasury yield go from here. We’re not keeping to the course laid out by Miran, but that doesn’t mean that we are irrevocably on the road to de-dollarization. |