| Bloomberg Evening Briefing Americas |

| |

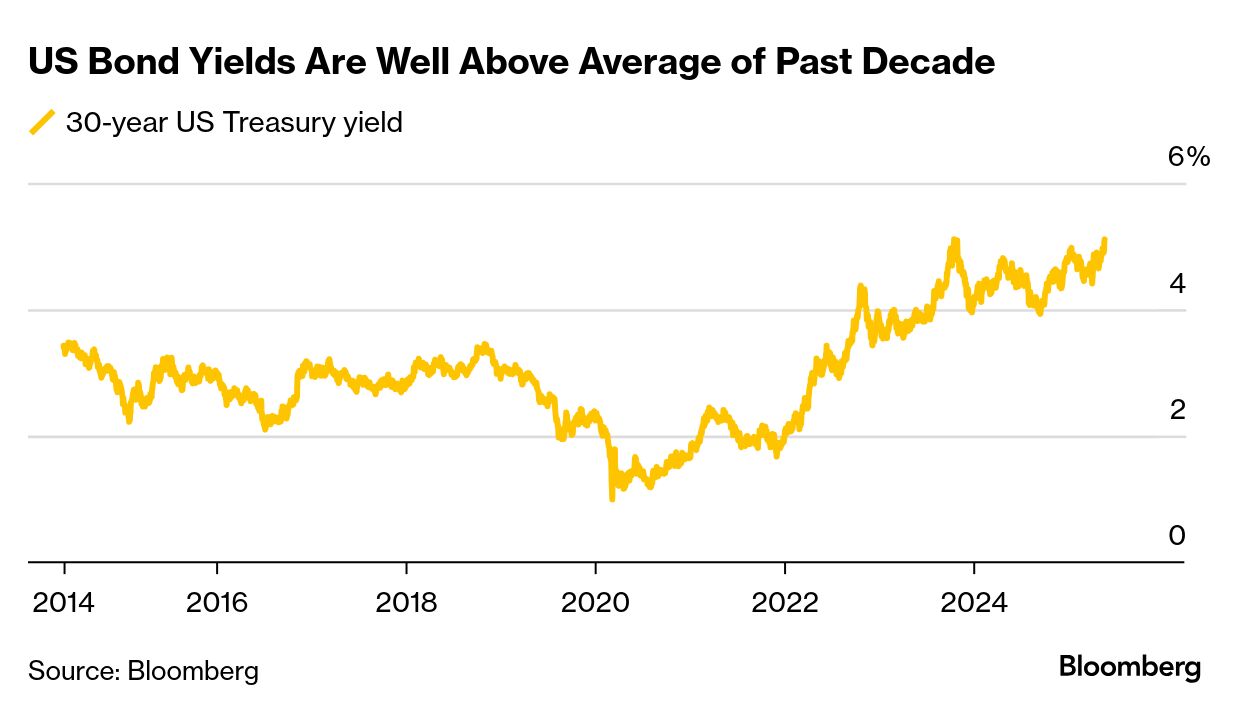

| US President Donald Trump’s signature tax bill passed the 435-member House of Representatives on Thursday morning by one vote. The sprawling, multitrillion-dollar package proposed by Republicans, which would (among many other things) slash funding for safety net programs in favor of extending tax cuts, is projected to add trillions of dollars to America’s almost $37 trillion national debt. The bill now heads to the Senate, which like the House is also narrowly controlled by the GOP. Whether the House bill’s more extreme provisions survive the Senate and a subsequent conference remains to be seen. But short of a massive transformation, the end result is unlikely to please increasingly nervous investors who see the country’s ballooning debt as a monstrous chicken coming home to roost. The yield on 30-year Treasury bonds has passed 5%, injecting a dose of harsh economic reality into Trump’s fiscal policy. Last week, Moody’s joined other bond-rating providers in lowering the US sovereign grade. The market has been manifesting unease over the US fiscal profile and the repeated unwillingness of its political parties to address a calamitous state of budgetary affairs. Investors are beginning to question whether they would loan the US government money—and other warning signs are emerging that America’s interest bill alone could accelerate fiscal deterioration. Meanwhile, Deutsche Bank’s Tim Baker warns that the US dollar may end up paying the bigger price if fiscal concerns persist. The dollar has already borne the brunt of the market’s early reaction to the Moody’s downgrade. A Bloomberg gauge of the US currency is now down nearly 1% on the week and more than 7% so far this year—its worst annual start on record in data going back to 2005. —Jordan Parker Erb and David E. Rovella | |

What You Need to Know Today | |

| |

|

| A federal judge has for now blocked as unconstitutional Trump’s efforts to shutter the Department of Education, including a plan to cut the workforce in half and remove thousands of employees. US District Judge Myong Joun in Boston found that Trump lacked power to effectively dissolve a federal agency created by Congress by getting rid of its employees, closing regional offices and moving programs to other federal agencies. In a Thursday ruling, Joun wrote the personnel cuts would “likely cripple the department” and ordered the administration to reinstate employees to carry out duties required under US law, including managing federal student loans, aiding state education programs and enforcing compliance with civil rights laws. The injunction blocks a “reduction in force” announced in early March to cut more than half of the department’s employees, as well as a March 21 executive order directing US officials to “take all necessary steps to facilitate the closure of the Department of Education” to the fullest extent allowed by law. | |

| |

|

| The Justice Department is probing whether Google violated antitrust law with an agreement to use the artificial intelligence technology of a popular chatbot maker. Antitrust enforcers are examining whether Google structured an agreement with Character.AI to avoid formal government merger scrutiny. Such deals have been hailed in Silicon Valley as an efficient way for companies to bring in expertise for new projects. However, they’ve also caught the attention of regulators wary of mature technology companies using their clout to head off competition from new innovators. | |

|

| Fannie Mae and Freddie Mac shares surged to their highest levels in 16 years after Trump’s proposal to privatize the mortgage companies. While investors are enthusiastic about the plan, it will be tricky to pull off. Trump floated the idea in his first term, with then-Treasury Secretary Steven Mnuchin taking the lead, but ran into resistance over fears that any move to change their status as government-sponsored enterprises would disrupt the mortgage market. Shares of Fannie soared 51% for their strongest performance since August 2009, while Freddie jumped 42% for its best day since September 2019. | |

|

| |

|

| A new Trump administration report blames the rise in chronic diseases in the US on unhealthy food ingredients, chemicals, overreliance on medication and corporate spending, but stopped short of attacking food growers and manufacturers as much as they feared. The 69-page report was compiled by the “Make America Healthy Again Commission,” which is led by Health and Human Services Secretary Robert F. Kennedy Jr. Agricultural companies, pharmaceutical manufacturers and others have worried that the push by Kennedy—known for unorthodox and unsupported views on topics ranging from health to vaccines—will lead to a raft of new regulations. However, the report doesn’t lay the groundwork for the type of aggressive policies that had most concerned them. | |

|

| |

What You’ll Need to Know Tomorrow | |

| |

| |