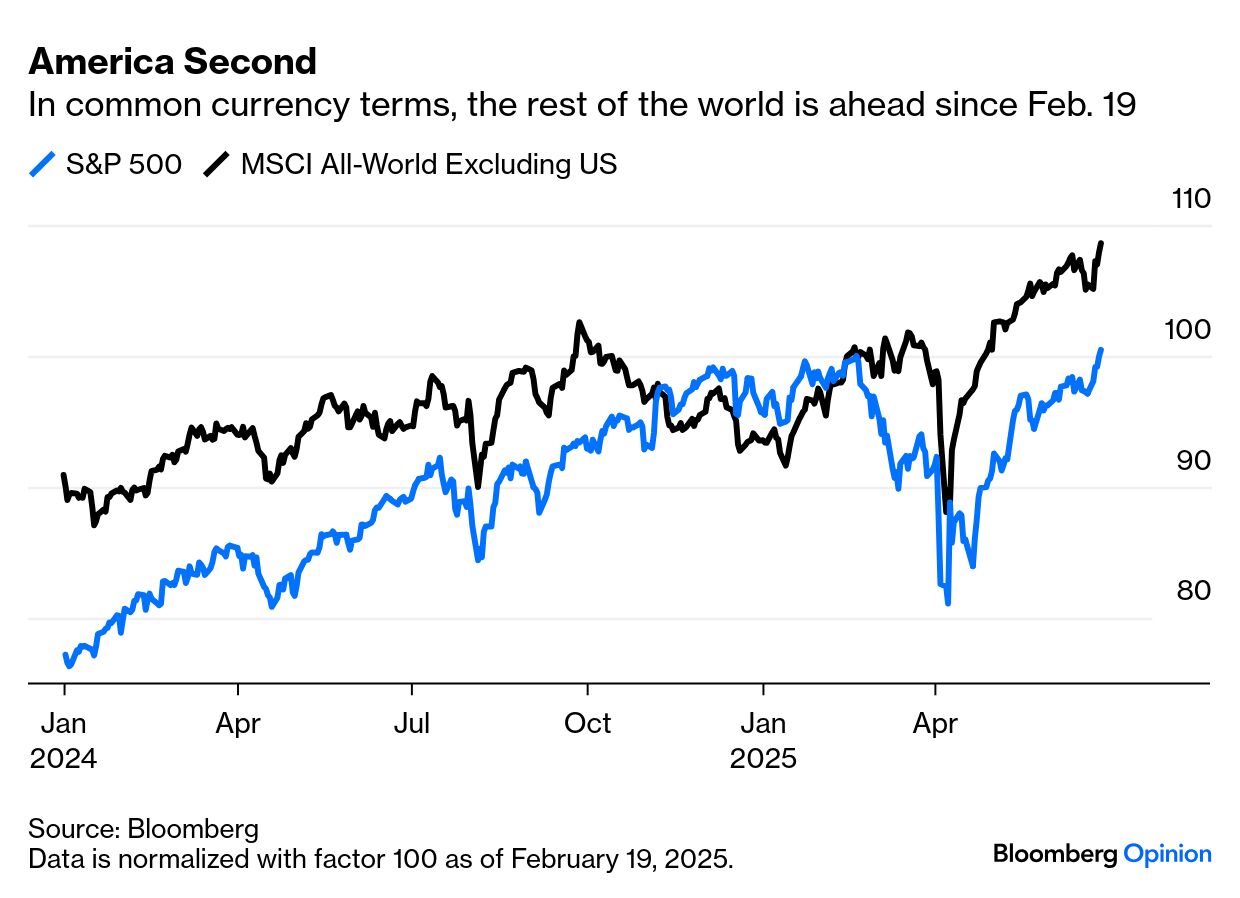

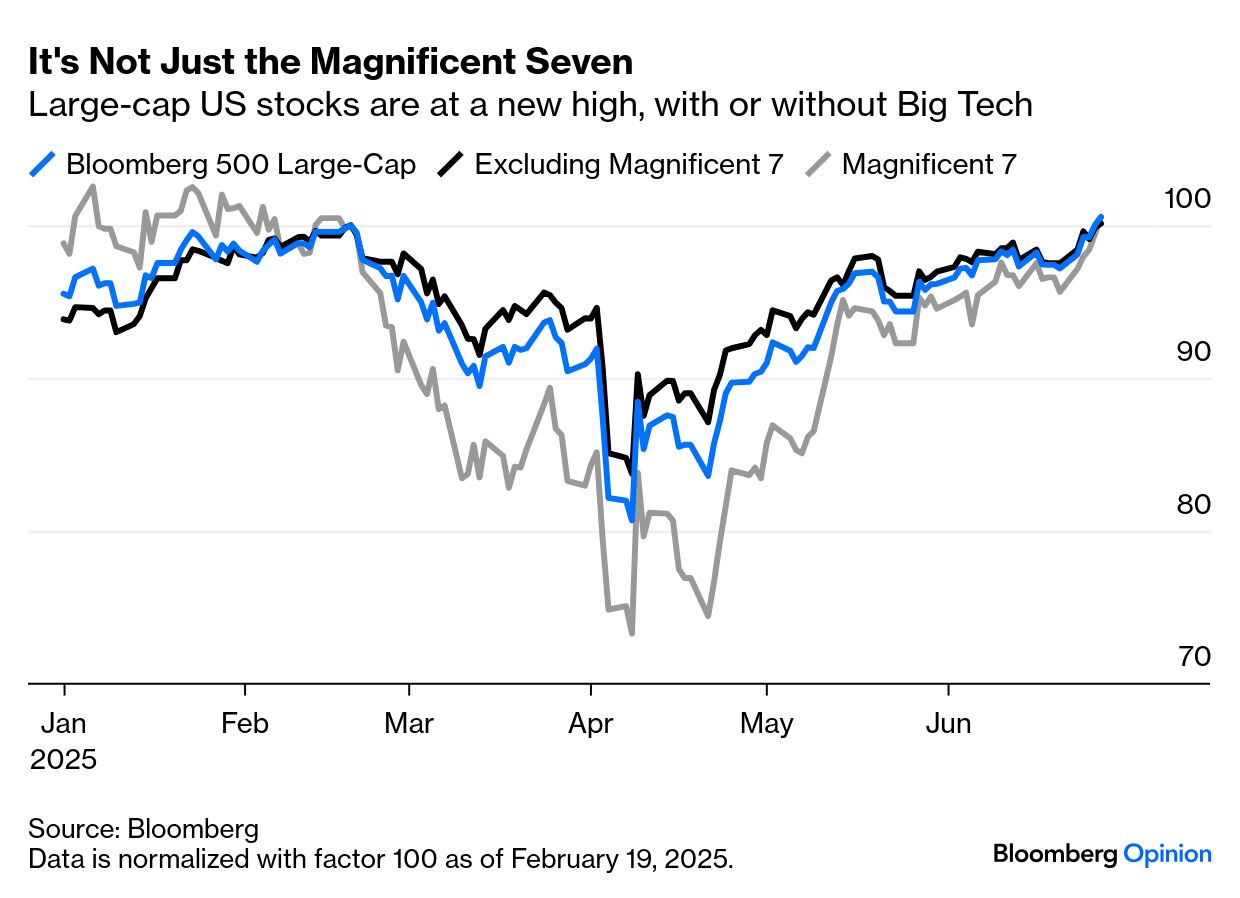

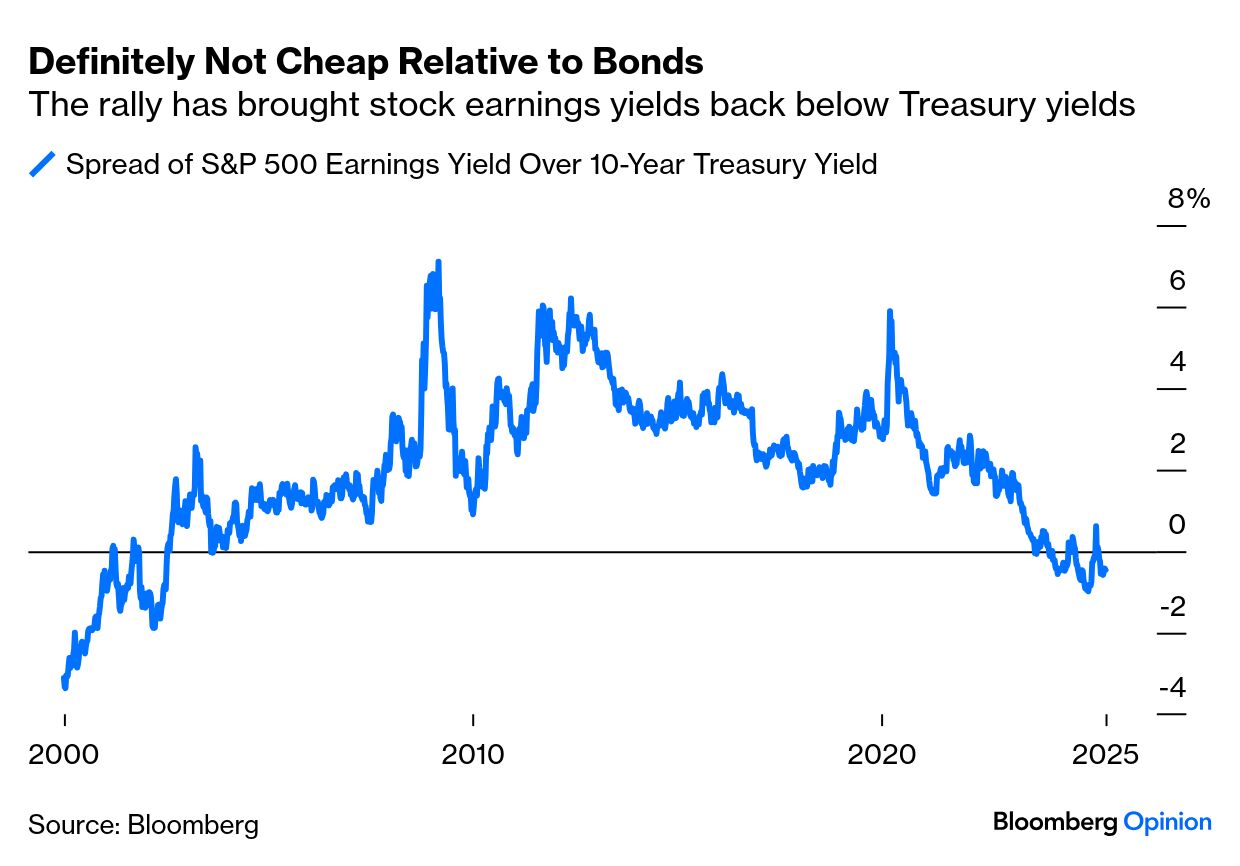

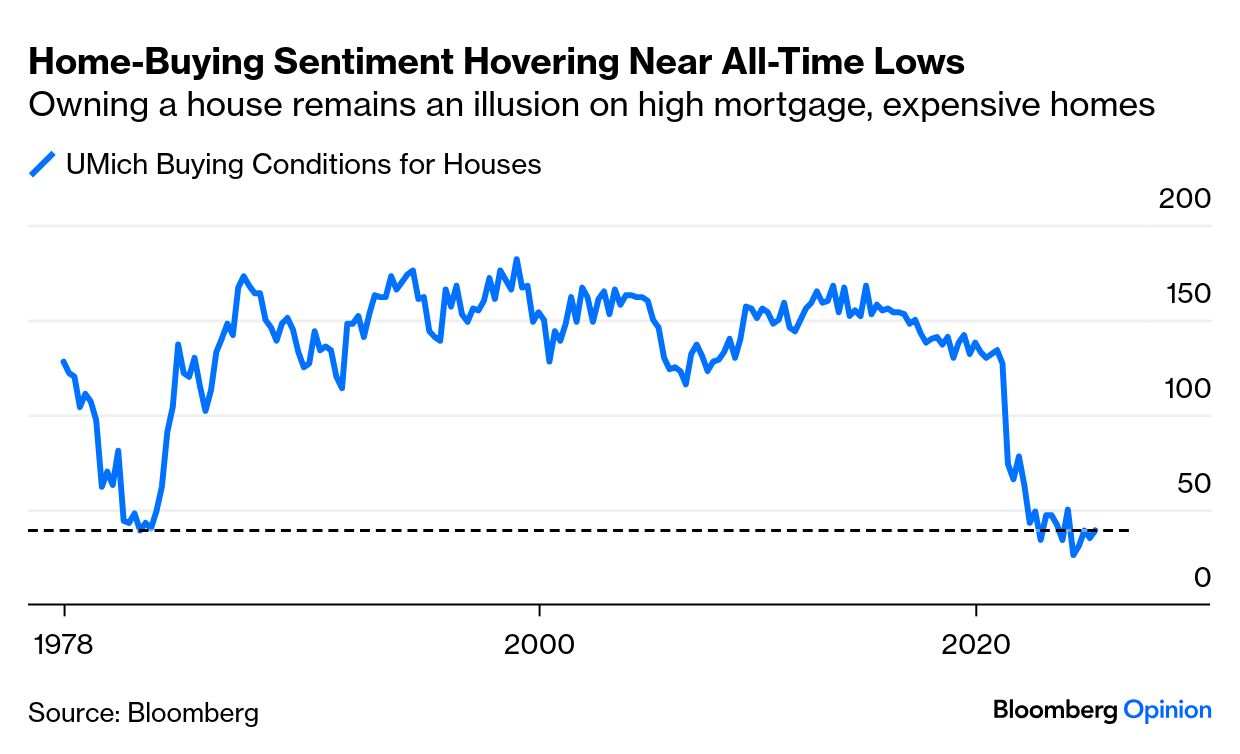

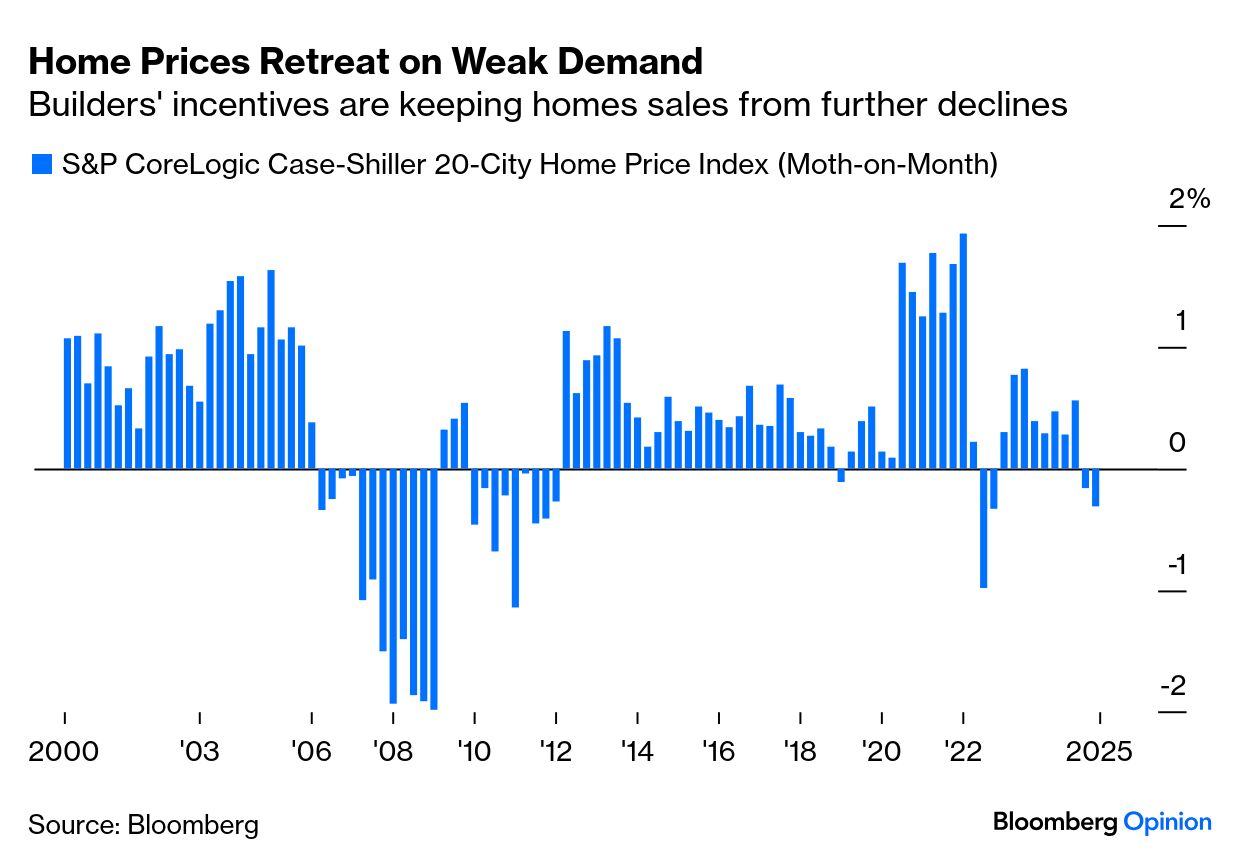

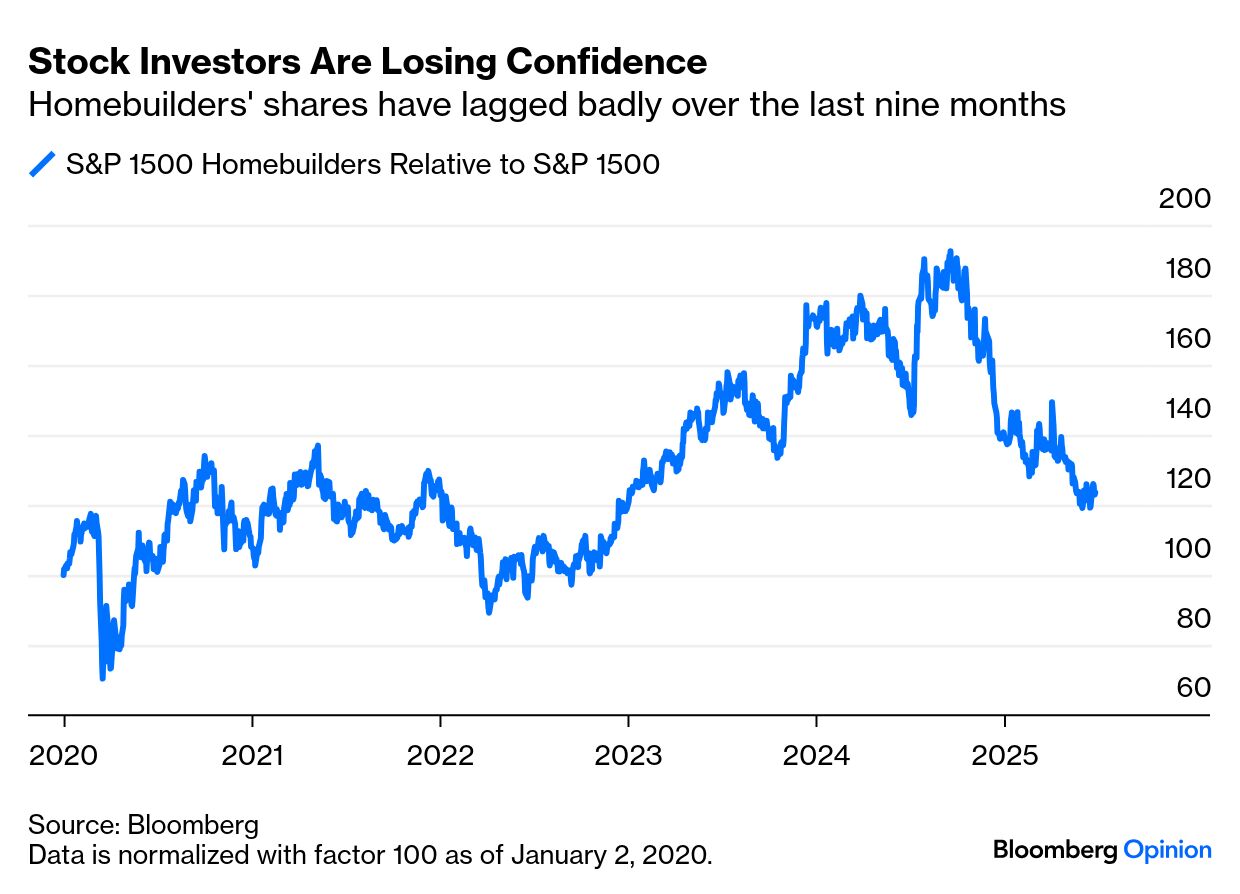

| Liberation Day can be forgotten. Coronation Day — Feb. 19, when the White House released an image of President Donald Trump wearing a crown, and the S&P 500 set a high for the year before beginning its descent — is also firmly in the past. As the US begins Independence Day week, the index is back at an all-time high. There are many reasons behind this, but plainly it’s an America First stock market record. The benchmark is above its Feb. 19 level when denominated in dollars, but not when valued in any other major currency. This high owes much to the dollar’s depreciation: The rest of the world’s stocks have beaten the US by about 10 percentage points since then. In dollars, that means a nice gain: The new all-time high doesn’t, then, challenge the prevailing narrative that it’s best to take money out of the US and reallocate elsewhere. The hugely significant decision to remove the Section 899 “retaliation tax” clause from the One Big Beautiful Bill Act currently before Congress will be a major relief for asset allocators on this basis, but leaves much of the logic for switching out of the US market intact. This rebound has little to do with the giant tech platform groups that dominate the S&P. Since the previous high, Bloomberg’s Magnificent Seven index dipped much further during the alarm over the Liberation Day tariffs, but its performance is now bang in line with an index of the other 493 largest stocks: This rebound took Wall Street by surprise. According to the regular average of strategists’ official year-end forecasts carried out by my Bloomberg colleague Lu Wang, they have just started to raise their estimates after slashing them during the trade furor. This stokes optimistic momentum, as they’re now engaged in upping their forecasts again. The selloff was driven primarily by politics — growing realization that Trump 2.0 was serious about tariffs, followed by outright horror after the extreme levies announced on April 2, Liberation Day. The 90-day pause that triggered the rebound ends next week. It’s unclear what the administration will do then, but Canada’s concession to withdraw a digital sales tax to restart trade talks suggests nothing can be taken as a foregone conclusion. Thus the rebound reflects the belief that a) the big Liberation Day tariffs will quietly go away for the most part, and b) the levies already in place won’t hurt the economy or company bottom lines too much. After a good few weeks for the administration, the hope is that Trump will desist from market-unfriendly ideas (tariffs and a clampdown on legal migration), while going ahead full-bore on tax cuts and deregulation. The faith that margins will be proof against tariffs (which, after all, are paid by importing companies) and against other pressures is perhaps the greatest reason for concern. The S&P 500 is back trading at more than three times sales, close to a record: Sales multiples can widen like this because profit margins have boomed since the pandemic. If companies keep a higher proportion of their revenues as profit, then it makes sense for the revenue multiple to increase. But, as I outlined over the weekend, there are ample reasons to think that Trump 2.0 policies won’t be kind to margins. This looks like an extremely exposed position that is impossible to call cheap. It’s also more or less impossible to say that stocks are decent value compared to bonds. This rally, combined with sticky Treasury yields as the Federal Reserve resists cutting rates, has brought the earnings yield on the S&P (the inverse of the price/earnings multiple) below the 10-year Treasury yield. Buy now and you are receiving no compensation for the extra risk of stocks compared to bonds: This points to another key explanation for the rally: The belief that rates and longer-term yields will soon fall. That’s in part because of the increasing pressure on the Fed, and the likelihood that it will soon be under the charge of someone more dovish. Any signal that the Fed’s independence is in question would do further damage to the dollar, but that would not be a problem for domestic investors in US equities. There’s also a prevalent belief that the Fed should cut rates. That would follow from a belief that tariffs’ impact on inflation is exaggerated (which we’ll return to, and will be tested by the forthcoming employment data) and also from concern over the housing market, which is showing serious signs of cracking (see below). There are always upside risks with the stock market to go with the downside, and there are plenty of them (as Jonathan Levin points out). This all-time high still looks premature. |