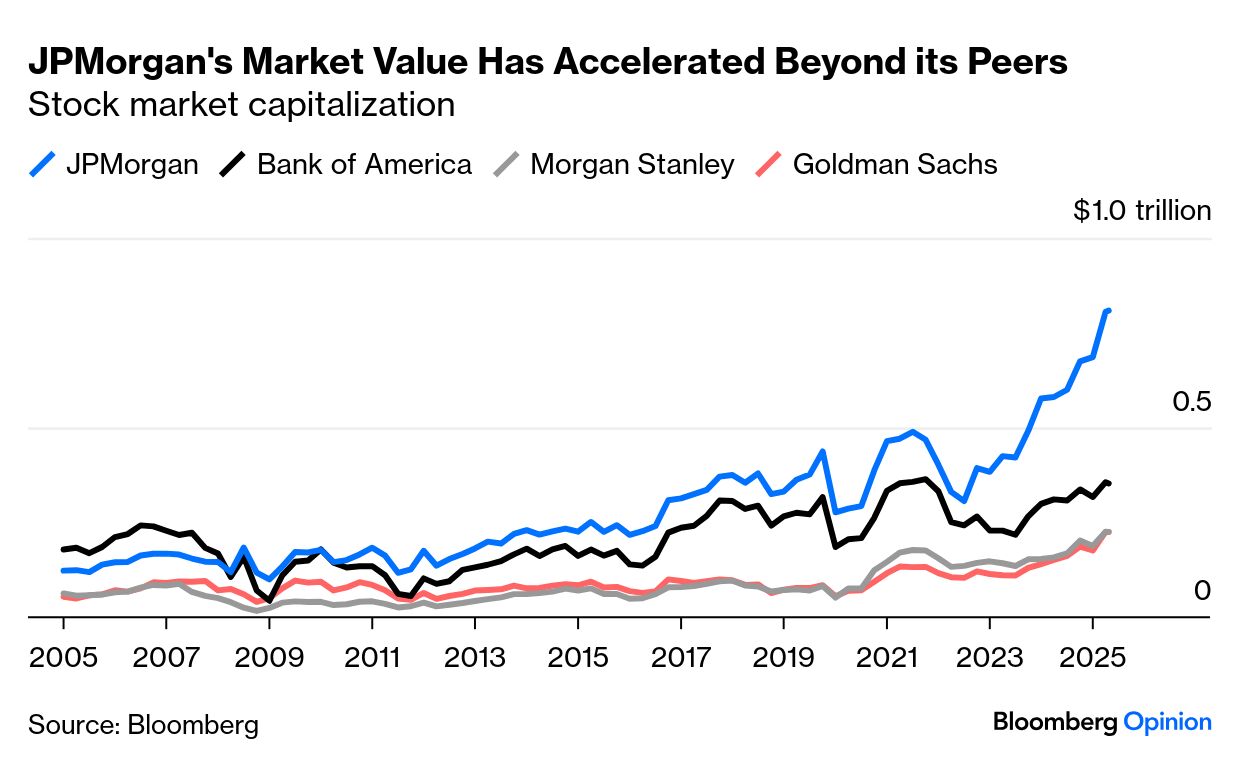

J.P. Morgan Would Be Pleased, No? | The genius of HBO’s The Gilded Age is that while it is a low-stakes historical drama, portions of the plot are, indeed, based on actual history. So you get a steady drip of fun facts, like: a female engineer was critical in building the Brooklyn Bridge; New York’s elite waged opera wars between the Met and the Academy of Music; alarm clocks — yes, alarm clocks — were once a golden ticket to upward mobility. And so on. Even the railroad tycoons and cosmopolitan heiresses in the soap opera are loosely based on real-life figures. Which brings me to the cigar-smoking, signet-ring-wearing, mustachioed robber baron we’re introduced to in Season 3:  Source: Karolina Wojtasik/HBO Perhaps you recognize him? J.P. Morgan was one of the most influential, ruthless financiers of the Gilded Age, hence why his character (played by Bill Camp) has a linchpin role in the latest plot. He’s called on by George Russell — the show’s Vanderbilt-esque leading man — who is seeking investors for his greatest project yet: A railroad to connect New York, Chicago and LA. Although viewers don’t know how Russell’s business venture will fare — things aren’t looking pretty, judging by this trailer — I can confidently say that Morgan’s namesake moneymaker is doing just peachy 140 years later. Valued at north of $800 billion, JPMorgan is now worth more than three of its largest competitors — Bank of America, Citigroup and Wells Fargo — combined. That skyrocketing blue line would please the late Mr. Morgan, no? Well, not exactly: Paul J. Davies says the bank’s dominance creates a number of headaches for Wall Street wunderkind Jamie Dimon. “To find growth that doesn’t make the bank more of a risk to itself and the economy it inhabits, it has to be very well run. But its immediate problem is an extremely high stock valuation and billions of dollars of excess capital – both of which threaten its returns if mishandled,” he says. Dimon, it seems, has been too pragmatic, too adaptive and too patient for his own good. Paul explains: “JPMorgan has roughly $60 billion of equity capital more than it needs to meet regulatory requirements. It is expected to spend about one-quarter of that on share buybacks over the rest of this year … Sounds great, but there’s a problem: Its shares are so highly valued that this is a bad trade for the bank. The current price is 2.4 times the book value per share that JPMorgan reported for the second quarter – buying those shares for investors means paying them more than double the current net asset value of the company they own.” That sounds like a pickle straight out of The Gilded Age! Read the whole thing. How Do You Solve a Problem Like Marc Andreessen? | One could argue that venture capitalist Marc Andreessen is 2025’s version of J.P. Morgan. Similar to how the banker backed railroads, steel mills and electricity outposts, Andreessen has bet big on emerging technologies — the internet, software, crypto and AI — to much success. But beyond their undeniable business acumen, the similarities stop there. While Morgan was a careful member of the old-school elite, Andreessen “was reared in a tiny Wisconsin town by parents of modest means,” explains Ron Brownstein. He has made a name for himself — like many a columnist in this very newsletter — by being quite opinionated:  This isn’t a bad thing, on the face of it! But some of those more controversial opinions can cause quite a stir. Like, say, believing that racial diversity programs in higher education are complete and total bogus and they hurt native-born, working-class White people, an idea Andreessen reportedly floated in a private group chat with White House officials and technology leaders. While Ron sees merits in Andreessen’s argument — it is getting harder for White kids from poor means to rise without access to higher education — he feels his ire toward DEI programs is misdirected. “The reality is that Black and Hispanic kids, the putative beneficiaries of diversity programs, remain woefully underrepresented at the most selective institutions,” explains Ron. “By blaming diversity programs, he’s literally whitewashing the implications of an economic agenda that prioritizes huge tax cuts for people like him over investments that could help more people transcend their modest beginnings as he has.” The billionaire’s diatribe arrives at a rather awkward time. Last week, a16z, the VC firm he co-founded, helped Substack raise $100 million in a funding round at a $1.1 billion valuation. Marc Rubinstein says the humble newsletter service’s “growth metrics are certainly impressive,” but he’s skeptical whether the company can generate revenue on par with other information networks like Reddit and YouTube. Andreessen’s comments, coupled with his investment, were not well-received in some corners of Substack’s universe. Writing in her newsletter “Qualified at the Intersection,” Shari Dunn reflected on the news: Here I am, building a community on a platform whose financial backing includes a man actively hostile to the very liberation my work is rooted in. That revelation has raised deep moral questions for me. Where can we go? If I leave, I don't have the kind of massive audience that would follow me elsewhere. I would be writing into the void. And yet, staying feels complicated, too.

As I’ve written before, Substack needs to reckon with its place in the media landscape — perhaps starting with those funding its foundation. |