|

|

|

|

Good morning. And happy Christmas in July. Before thoughts of winter sneak in your subconscious, I’m here to distract you with a new investment program in the U.S. that helps build compound interest as early as humanly possible. |

|

|

|

|

$1,000 investment accounts at birth |

|

|

|

|

Imagine being handed an investment account the day you’re born, preloaded with $1,000, just sitting there, quietly growing in the background until you turn 18. That’s about to become reality for American babies. |

|

|

|

|

Thanks to the reconciliation bill signed this month by U.S. President Donald Trump, every child born between 2025 and 2028 (and who is an American citizen) get $1,000 from the U.S. Treasury. That money goes straight into a low-cost index fund and stays put until they hit adulthood. |

|

|

|

|

At 18, it automatically becomes a traditional IRA, but cash can also be pulled out early to do things such as help pay for school, start a business or buy a first home. Plus, every account can take up to $5,000 in additional contributions each year, including up to $2,500 from a parent’s employer contributions, tax-free. |

|

|

|

|

It’s a bold idea and it made me wonder: What’s the Canadian version of this? |

|

|

|

|

Turns out, there isn’t really one. The closest thing is the Canada Learning Bond (CLB), which helps low-income families save for post-secondary education. It offers up to $2,000 through a child’s RESP, $500 upfront, then $100 a year until they’re 15. But, unlike the U.S. account, there’s a catch: Household income typically has to be under about $70,000 to qualify but could be a higher or lower threshold depending on how many kids you have. |

|

|

|

|

Could Canada roll out a universal baby bond program such as the U.S. one? Not likely, at least any time soon, experts said. “There would be large administrative costs to set something like this up,” said Jason Heath, managing director of Objective Financial Partners. |

|

|

|

|

But whether it’s a U.S. baby bond, an RESP or a plain old investment account, the takeaway is the same: start early. |

|

|

|

|

Marc Henein, a senior wealth adviser at ScotiaMcLeod, told me that if you invest $1,000 with a 6-per-cent annual return for 18 years and leave it alone, it grows to about $2,854, without adding a single extra dollar. |

|

|

|

|

“Starting early would probably be the best advice I could give anybody,” Mr. Henein said. |

|

|

|

|

|

|

|

|

So, if you’re a parent in Canada, opening an RESP for your child is still your best move. The government matches 20 per cent of your contribution, up to $500 a year per child. Hard to beat. |

|

|

|

|

|

|

|

|

|

|

|

|

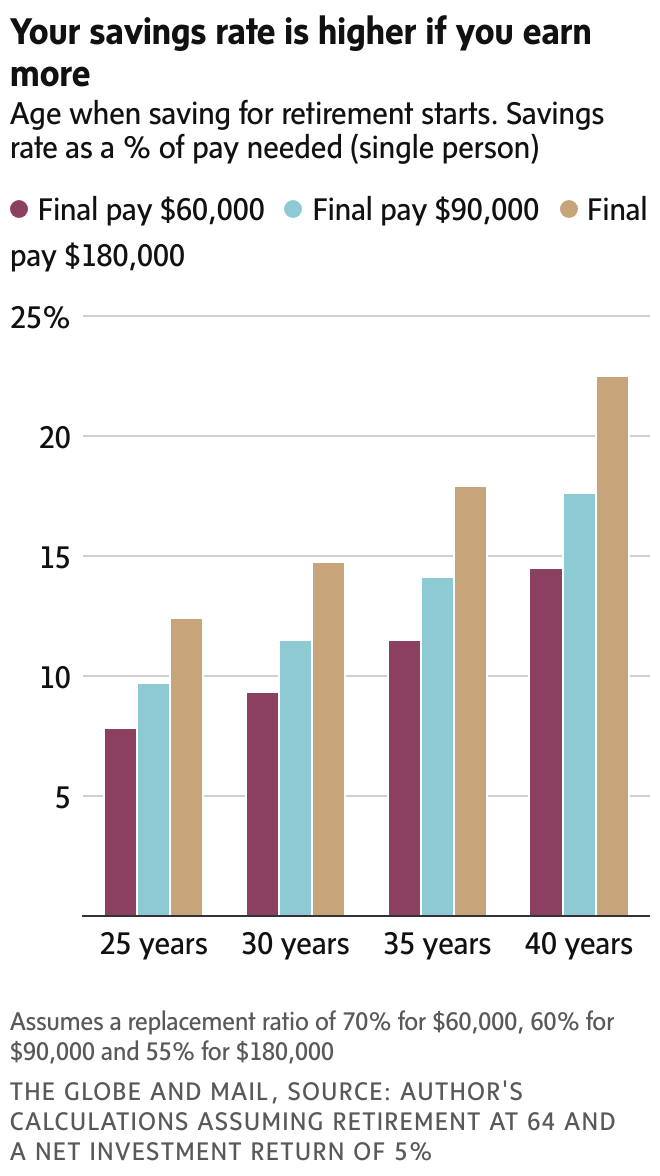

The more you earn, the more you need to save. That might seem backward, but for high-income Canadians, the usual retirement safety nets, such as CPP and OAS, don’t come close to replacing lost income. That means bigger paycheques demand higher savings rates. |

|

|

|

|

Why it matters: Many people assume a flat savings rate will work, but income level, age and whether you have a pension all dramatically change the math. Someone earning $180,000 may need to save more than double what someone making $60,000 does, just to maintain the same retirement standard. |

|

|

|

|

Yes, but: Not everyone needs to panic. Lower-income Canadians may find government benefits cover most of their retirement needs, especially if they’ve never earned much above $40,000. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Brian Borgford does his own personal investing at home in Calgary. Todd Korol/The Globe and Mail

|

|

|

|

|

|

|

|

|

|

|

The situation: Brian Borgford retired in 2014 at age 62, after 42 years in accounting, business consulting and teaching. He and his wife spent their final working years abroad in China, the United Arab Emirates and Qatar, before returning to Calgary to reconnect with family and enjoy retirement. These days, Mr. Borgford spends his time writing: He’s self-published dozens of books, including memoirs, fiction and even one on his investment strategies. He also maintains an investment blog and keeps active, though health issues have slowed his and his wife’s travel plans. |

|

|

|

|

The numbers: Mr. Borgford contributed to company pension plans, maximized his RRSPs and invested in non-registered accounts throughout his career. Early on, he invested through an adviser, but after retiring, he took control of his own portfolio, focusing on dividend-growth stocks. Today, he primarily lives off dividend income. |

|

|

|

|

His advice: “My advice to others approaching retirement is to ensure you are ready and have a plan for your postwork life,” he said. He almost retired a year earlier but waited, and that was the right call. “Once I retired, I never looked back.” His other tip: Don’t overcommit. “Remember, retirement is supposed to be fun!” |

|

|

|

|

|

|

|

|

|

|

|

|