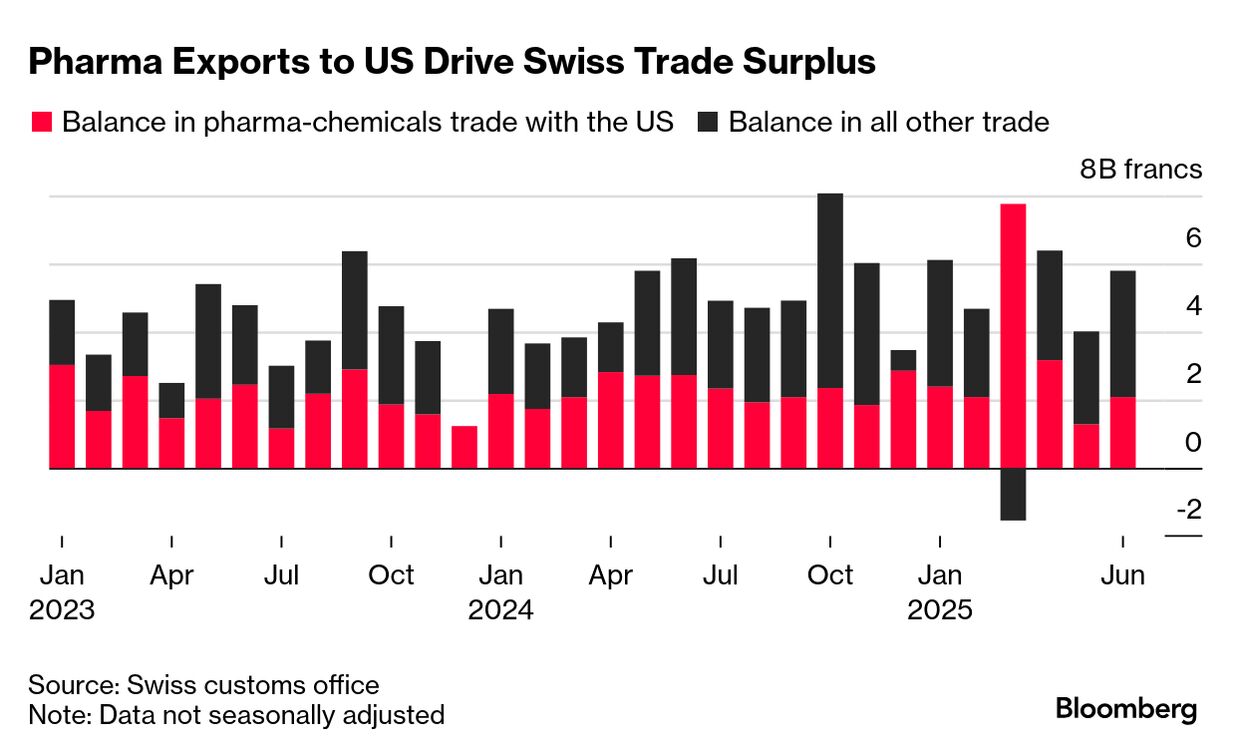

Swiss were shocked at Trump’s decision to slap tariffs of 39% on all their imports, among the most dramatic trade announcements so far. The government had been confident it could avoid such severe measures.

The stakes are enormous. The country’s goods exports to the US totaled more than $63 billion in 2024, notching up the 13th biggest trade deficit for the world’s largest economy — a tally likely to have irked Trump. For their own part, the Swiss claim to be the seventh-largest foreign investor in America.

“We weren’t able to reach agreement on the best way to reduce that trade deficit at all,” US Trade Representative Jamieson Greer told Bloomberg Television today. “They ship enormous amounts of pharmaceuticals to our country. We want to be making pharmaceuticals in our country.”

Bern’s trade negotiators were caught unawares by the announcement since they had received encouraging signals from several senior US officials, a person familiar with the talks told us. — Jennifer Duggan

What You Need to Know Today

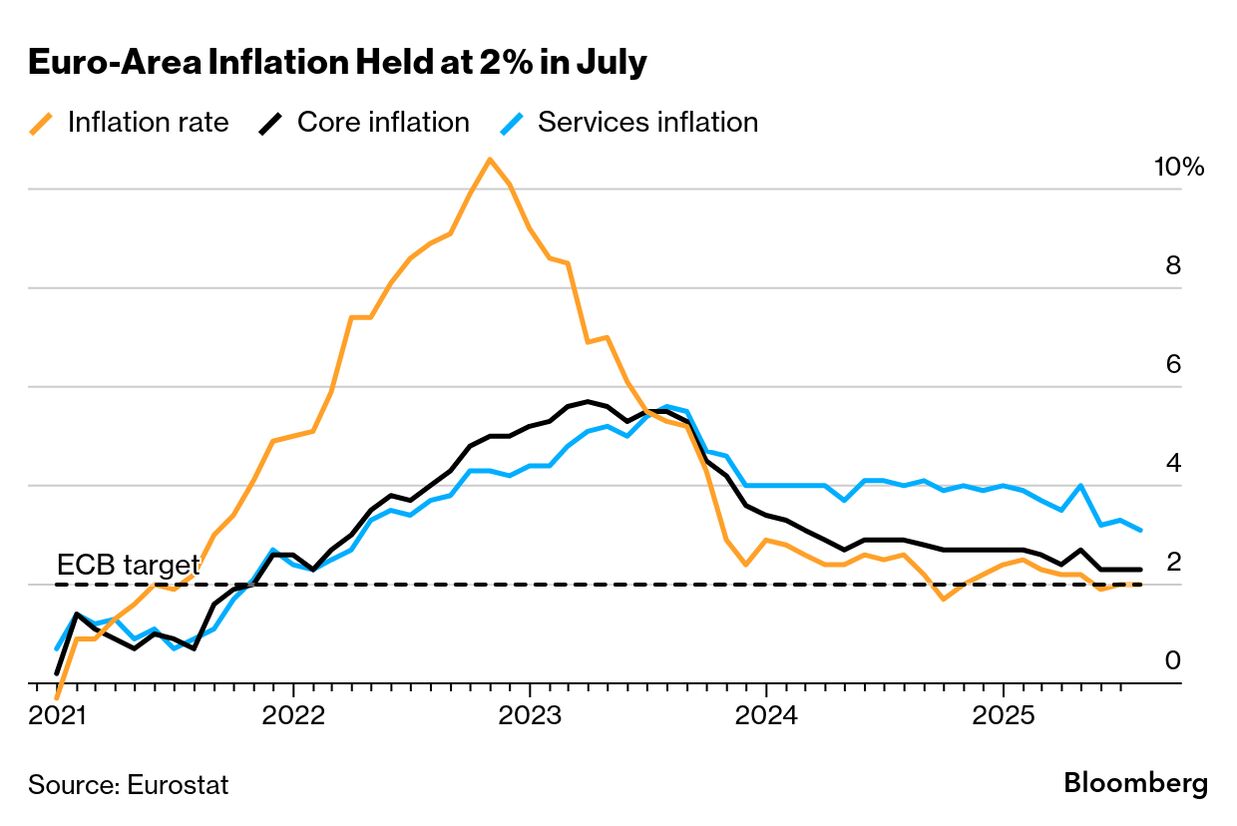

Euro-area inflation held at the European Central Bank’s target, supporting the case for officials who say there’s no rush to keep lowering interest rates. Consumer prices rose an annual 2% in July, the same pace as in the previous month, Eurostat said. Economists polled by Bloomberg had expected a slowdown to 1.9%. A core measure stripping out volatile energy and food costs increased 2.3% on the year, while closely-watched services inflation was the weakest since early 2022.

A weaker-than-expected July jobs report is calling into question the US Federal Reserve’s wait-and-see approach to interest-rate cuts, boosting the likelihood of a reduction at the central bank’s next meeting in September. Data published today by the Bureau of Labor Statistics showed payroll gains slowed to just 35,000 on average over the last three months, marking the slowest pace of hiring since the onset of the pandemic in 2020. US manufacturing contracted at the fasted pace in nine months while the unemployment rate ticked up to 4.2%.

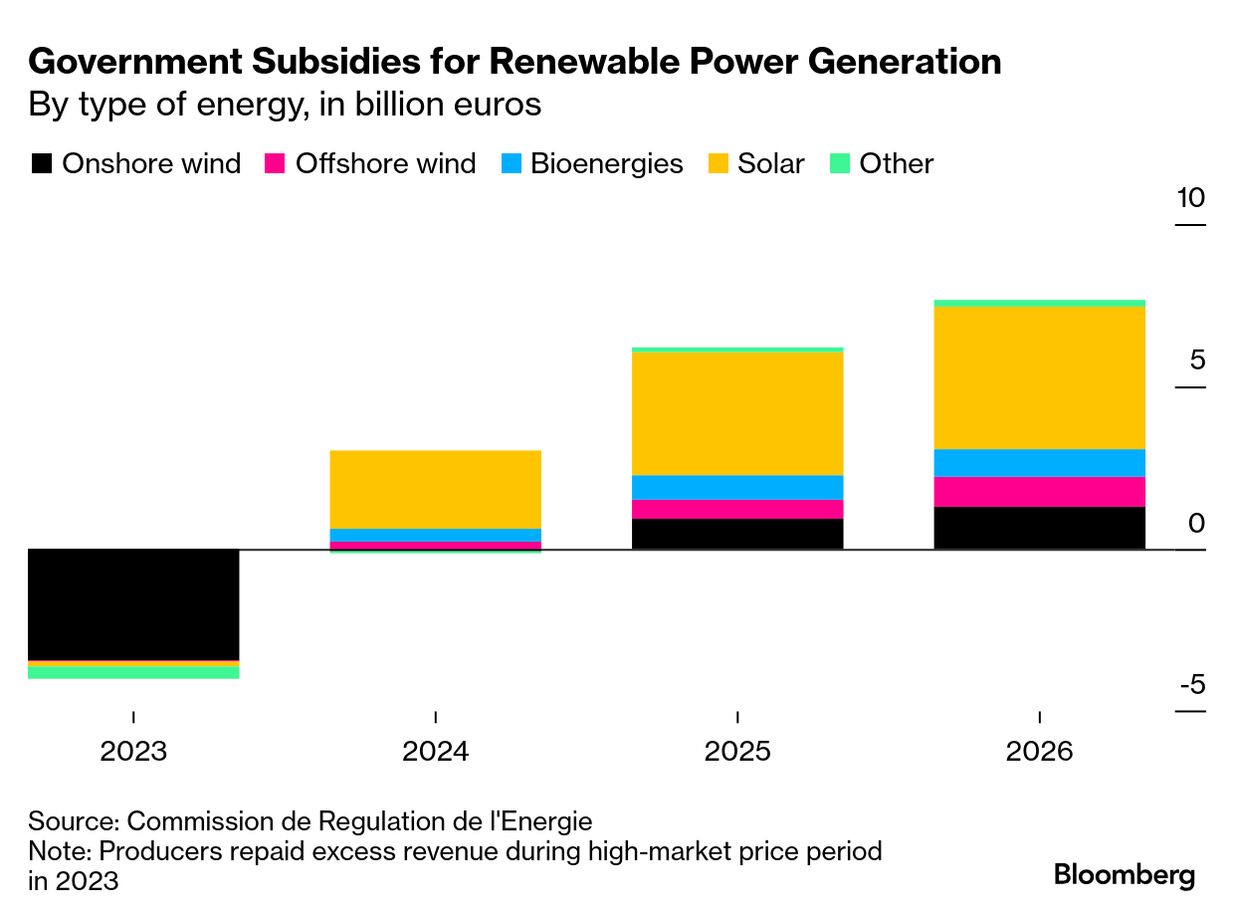

French government subsidies for renewable energy are set to jump 23% to a record €9 billion ($10.4 billion) next year, after almost doubling in 2025, according to the regulator. The surge in spending comes as the country adds more solar, wind and biogas. It may fuel a growing political controversy over the cost of the industry in a nation that’s grappling with ballooning debt and a glut of low-carbon electricity.

Senegal will take steps including raising taxes and renegotiating energy contracts to raise almost $10 billion over three years to help the West African nation deal with a debt crisis. Over the coming months, the government will cut spending and take measures to boost domestic revenue as part of efforts to stabilize public finances and restore investor confidence, Prime Minister Ousmane Sonko said in the capital, Dakar, today.

Artificial intelligence is giving some climate research projects a much-needed boost at a time of worsening extreme weather and funding cuts that threaten science in the US and elsewhere. While generative AI faces criticism due to the large amounts of power required to train and run sophisticated models, it also holds the promise of advancing science. Researchers are teaching existing AI models and creating new ones to perform routine tasks that would require several people to work for weeks or even months.

Mediobanca Chief Executive Officer Alberto Nagel said that national governments are an obstacle to creating bigger banks in the EU. “I don’t think it’s going to help the consolidation” of the financial industry in the bloc, Nagel said on Bloomberg TV, referring to efforts to slow or even prevent banking takeovers in Germany, Italy and Spain. That level of obstruction is a “new factor,” he said. Several banks including Italy’s UniCredit and Spain’s BBVA have launched attempts to buy rivals, only to meet with sometimes bitter opposition.

Alberto Nagel Photographer: Giuliano Berti/Bloomberg