|

|

|

Top performers: Our interactive Global League Tables rank investors, advisers, and more across the full spectrum of private market activity. Explore them here.

Barometers: Traditional private fund performance reporting lags by months, but we provide nearly real-time, data-driven estimates of performance across PE, VC, private debt, infrastructure, and natural resources. See Q2's results here.

Tech roundup: Read about VC dealmaking in AI & machine learning and enterprise SaaS.

Q2 comp sheets: Our quarterly guides on public company valuations and financials are now available for AI and mobility tech. |

|

|

|

|

|

| |

| A message from the American Investment Council |

|

|

| Advancing private equity & private credit across America |

|

The American Investment Council strengthens the private equity and private credit industries by defending its license to operate in every community across the nation. The American Investment Council is committed to promoting how investment supports jobs, small businesses, and retirees across the United States.

Learn more about this mission here and join the American Investment Council |

|

|

|

|

|

| |

|

|

|

There is a lot of anxious energy floating through offices and boardrooms right now. Who is eating the cost of tariffs? What will the Fed do in September? Why are we seeing downward revisions in economic data? When will we all lose our jobs to AI?

Even as public markets push to new records, sentiment across the board is shaky. It doesn't help that we're in the last stretch of summer—the days are still long and the heat is getting to us all.

This week we released our latest US Market Insights report, providing a comprehensive snapshot of private markets, from PE and VC to private credit and infrastructure, through the first half of 2025. We have nearly 100 pages of charts and data trying to bring clarity in the face of uncertainty.

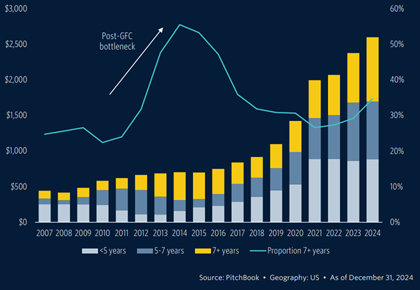

Private markets are in their own dog days. The average age of investments across all types of drawdown funds is lengthening, and the exit environment is a question mark (with the exception of anything that has AI or crypto written on the box).

|

| PE NAV ($B) by fund age |

Investors have seen cycles like this before, it took the better part of a decade to digest the pre-GFC deal environment. But also, the asset class has multiplied a few times over since then.

Continuation funds and secondary transactions are on pace to eclipse 2024 levels. And, excepting 2020, the percentage of GP-led transactions is at a 10-year high.

As the pressure to complete the investment cycle builds for GPs, we have different release valves than existed a decade ago. Registrations for semi-liquid vehicles are at an all-time high and the floodgates of capital from retail investors are being readied.

In the meantime we all are forced to hurry up and wait. See our full view across macro, asset allocation, PE, VC, and more in our Q3 Quantitative Perspectives: US Market Insights.

|

|

|

|

|

|

| Valuations reset amid AI's rise |

|

|

After years of inflated pandemic-era valuations, VC is entering a long-overdue correction to match market realities. A quarter of VC rounds have been down or flat, the highest share in a decade, and nearly every high-profile IPO debuted well below their private market peaks in Q2.

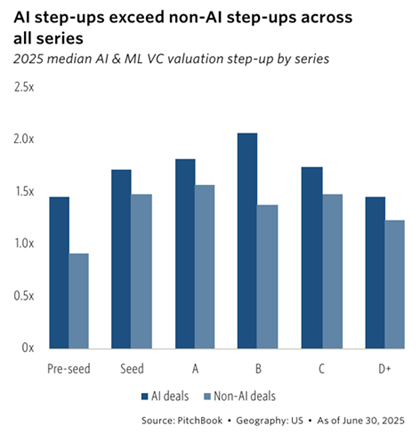

Venture's bifurcation is stark: While the broader market contends with muted valuation growth, AI companies continue to command higher step-ups, faster fundraising cycles, and larger deal sizes across all stages. The median Series B step-up for AI startups is 2.1x, compared with 1.4x for non-AI peers.

Sectors aligned with the administration's policy priorities—AI, defense tech, fintech, and crypto—are also enjoying valuation resilience. It is no coincidence that stablecoin issuer Circle more than doubled its stock price on its first trading day, buoyed by legislative progress on the GENIUS Act.

The good news? This normalization is a healthy correction. By shaking off their "golden handcuffs" of legacy markups, startups can reopen paths to funding and exits. Yet, with volatile public markets and lingering macroeconomic uncertainty, the path forward will remain uneven. For now, 2025 is shaping up to be a defining inflection point for venture.

Read more about the current venture ecosystem in our US VC Valuations and Returns Report.

|

|

|

|

|

|

| |

|

|

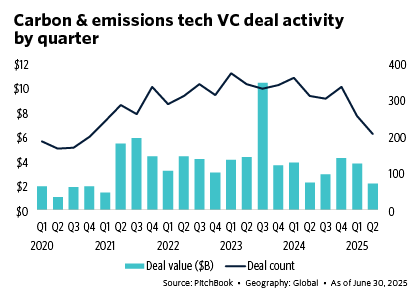

Carbon & Emissions Tech VC Trends

Startups in the carbon and emissions tech industry collected $2 billion in VC funding in Q2—representing a decline of 44% quarter-over-quarter.

The quarter marked a four-year low, driven by a lack of mega-deals and a steep decline in funding for the carbon tech segment.

|

|

Despite the slowdown, median deal sizes overall continued their long-term climb, and policy shifts under the Big Beautiful Bill Act are poised to reshape incentives for carbon capture technologies.

Read the free report

|

|

|

|

|

|

| |

|

|

Sept. 18: Our senior analyst Anikka Villegas will be presenting at Morningstar's Sustainable Investment Summit, covering the future of climate, ESG, and DEI in private markets. Register today to gain insights on investor trends, performance, and diversity.

Sept. 24-26 PitchBook is partnering with IPEM to offer a €500 discount for IPEM Paris 2025. Learn from private capital market leaders, including PitchBook senior analyst Nicolas Moura, who will present an EMEA market update. Register here |

|

|

|

|

|

| |

|

|

Our insights and data featured in the press:

• PitchBook analysts' take on the executive order that could make it easier to incorporate alternative assets into 401(k)s. [CNN; | | | | | | | |