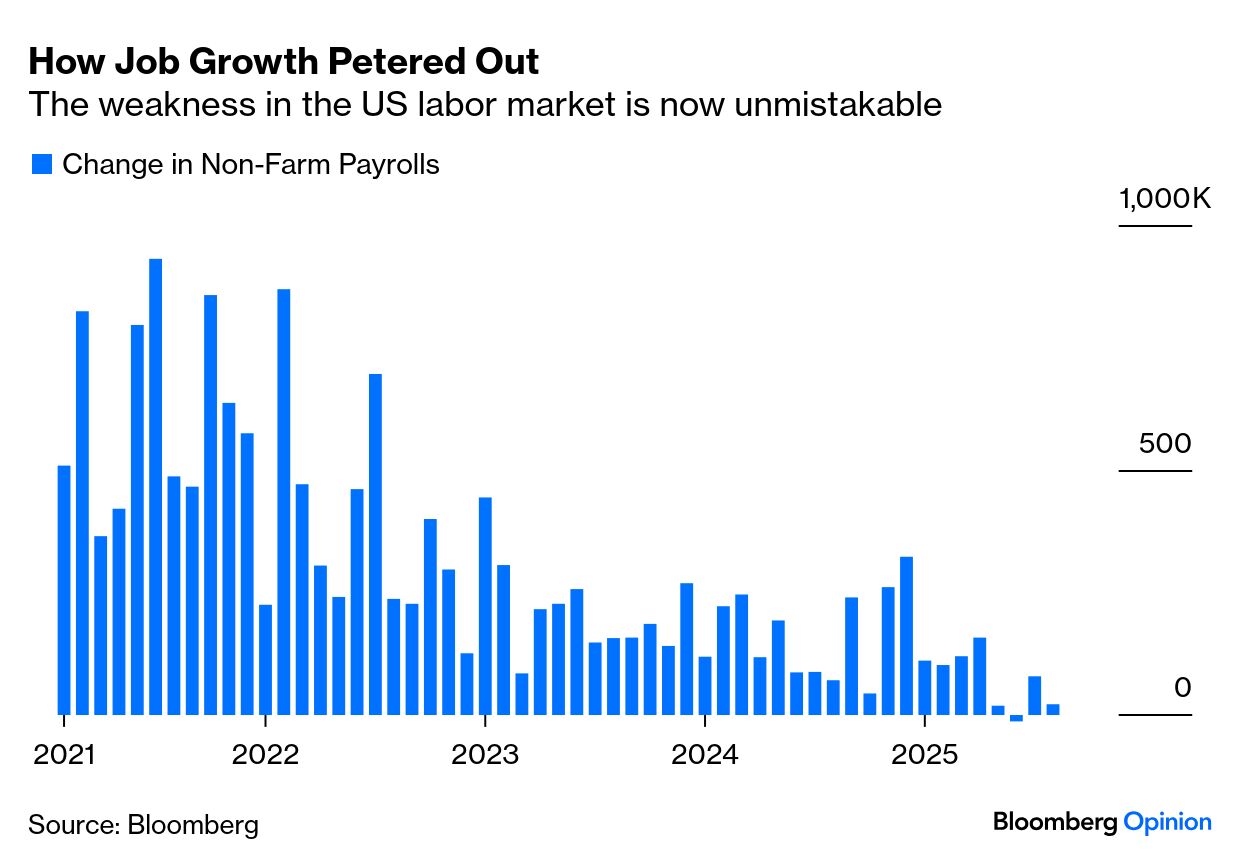

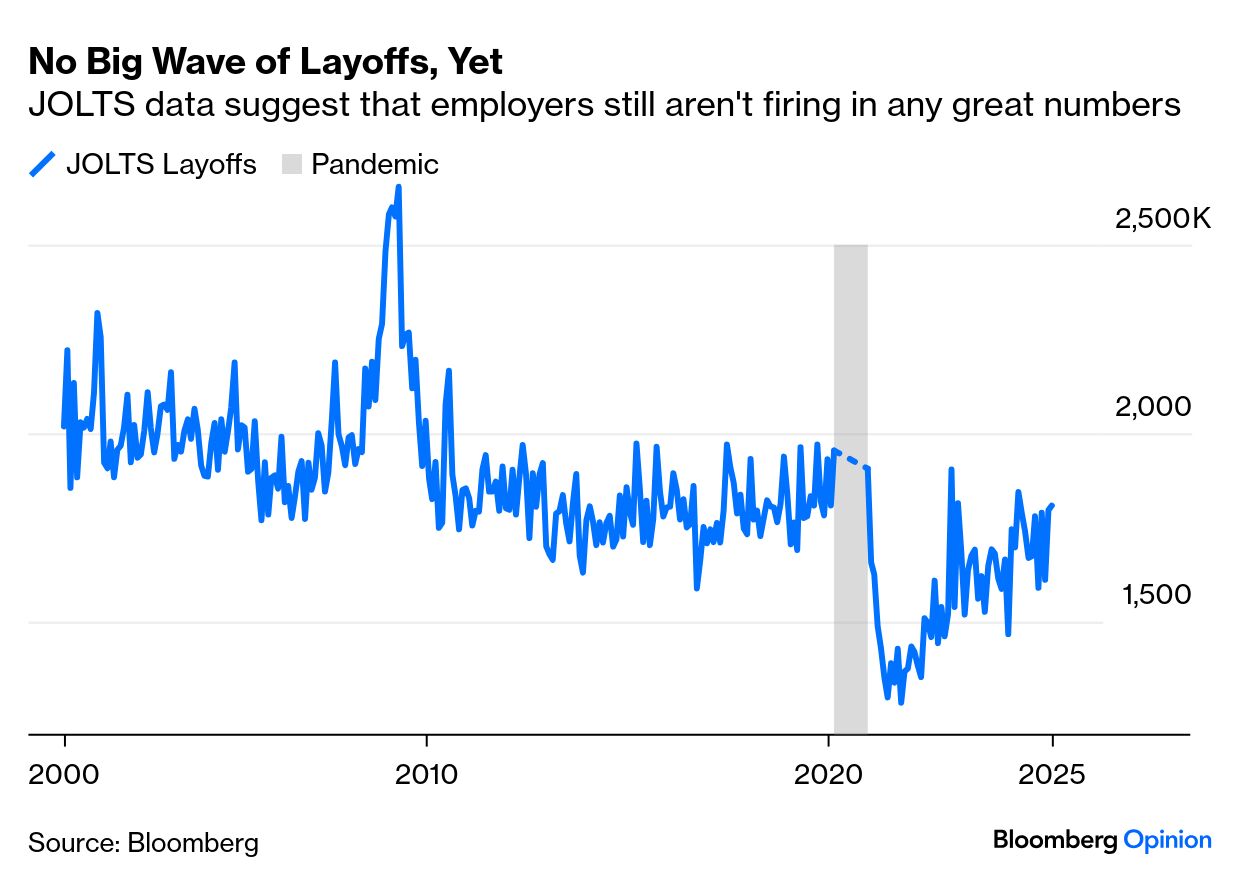

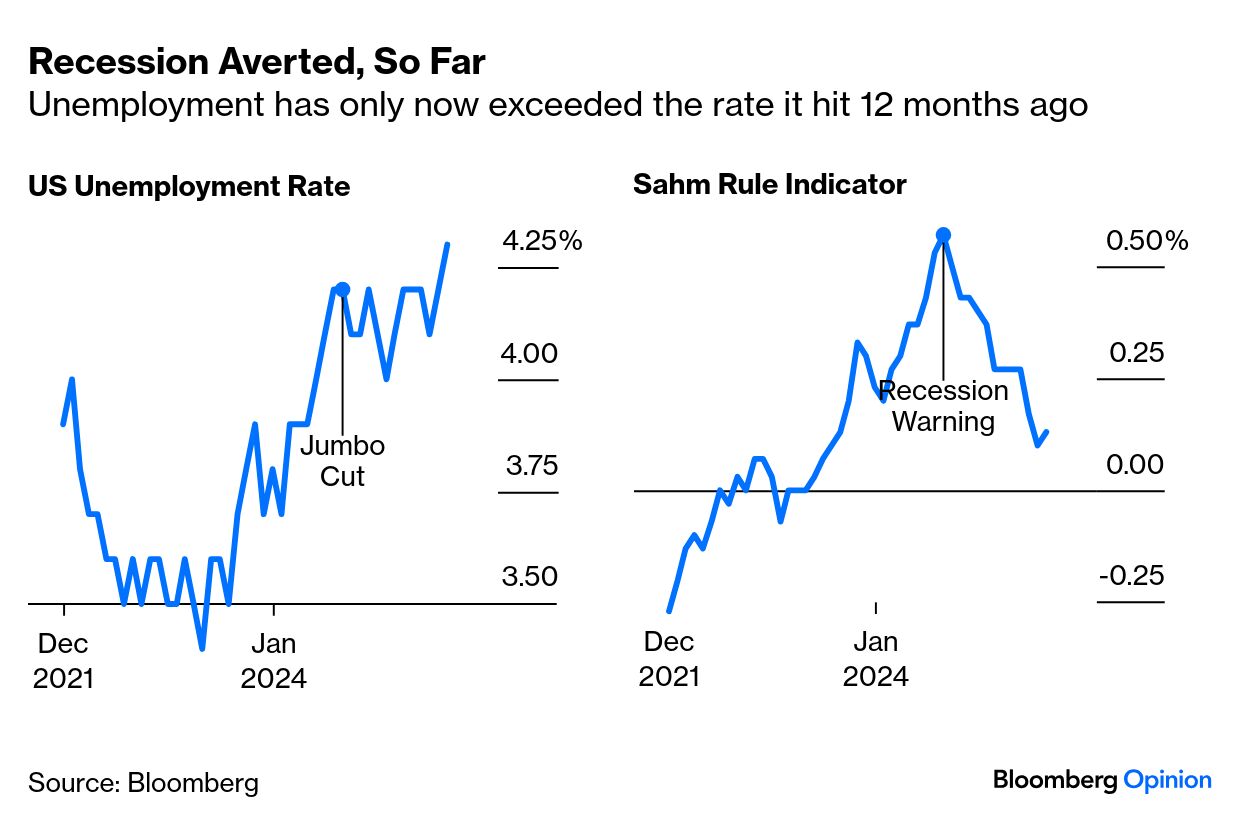

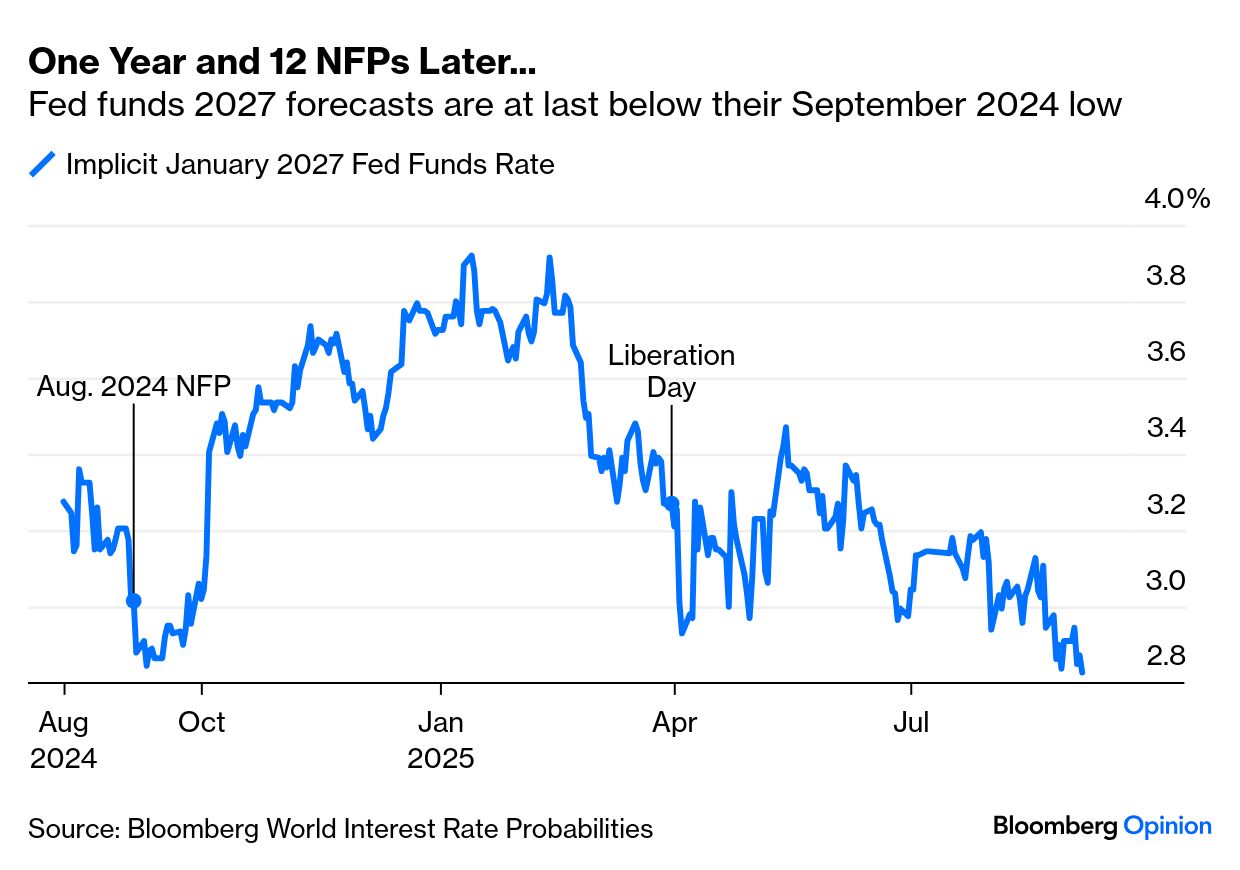

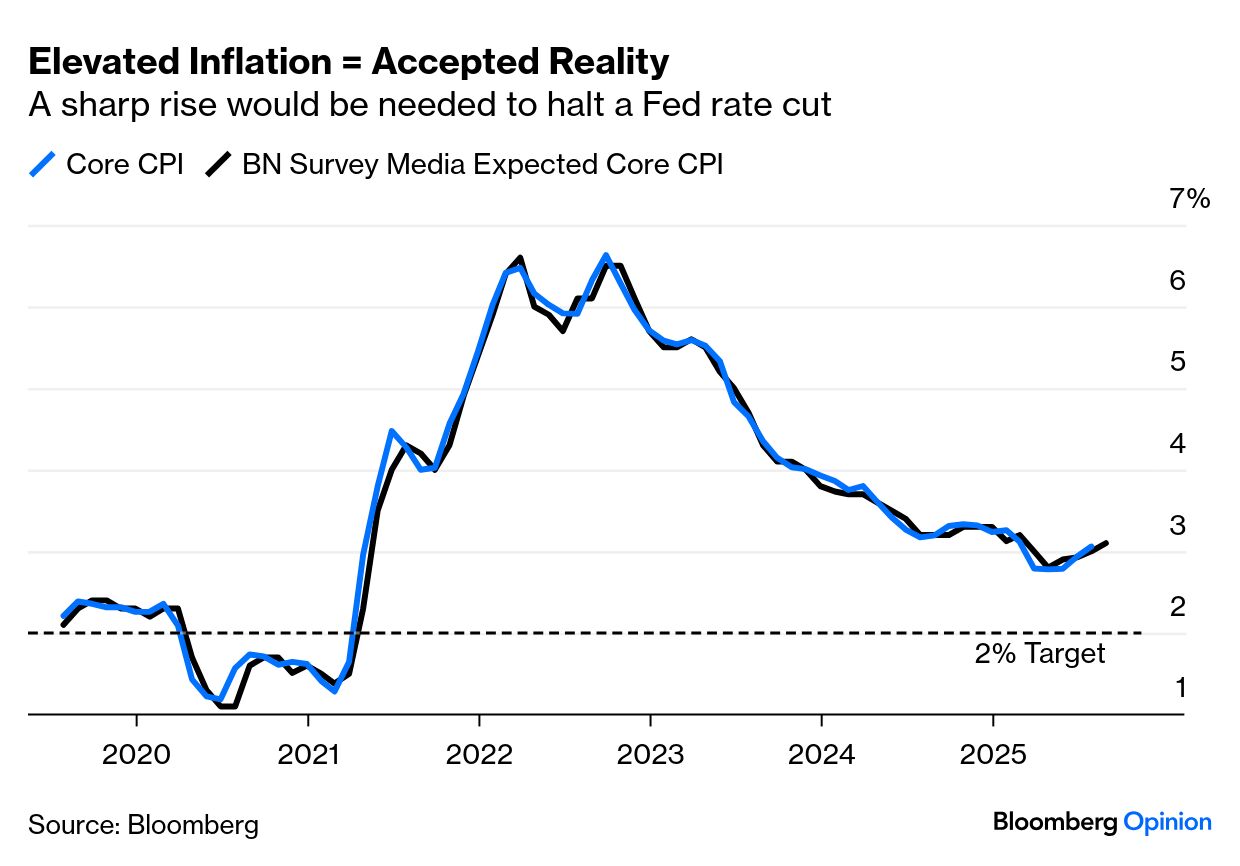

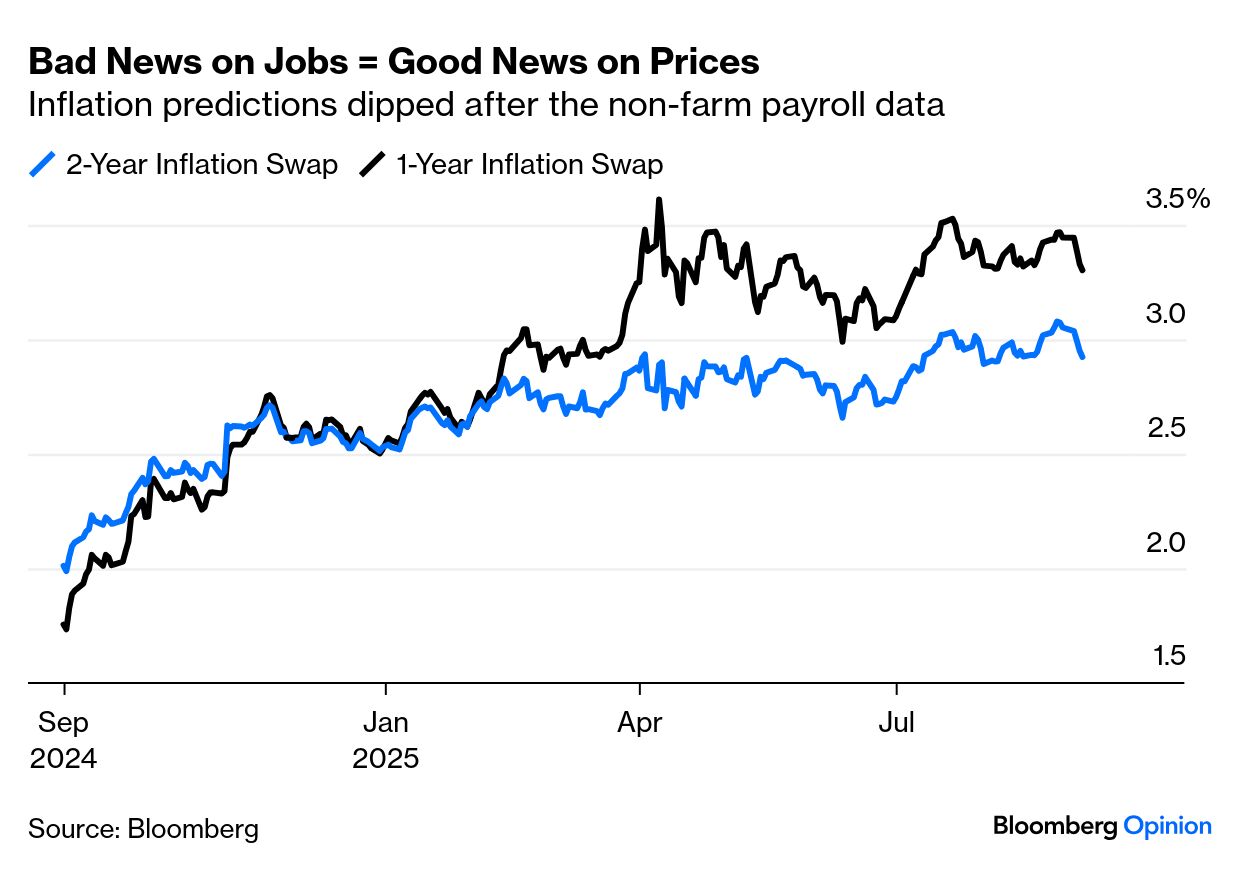

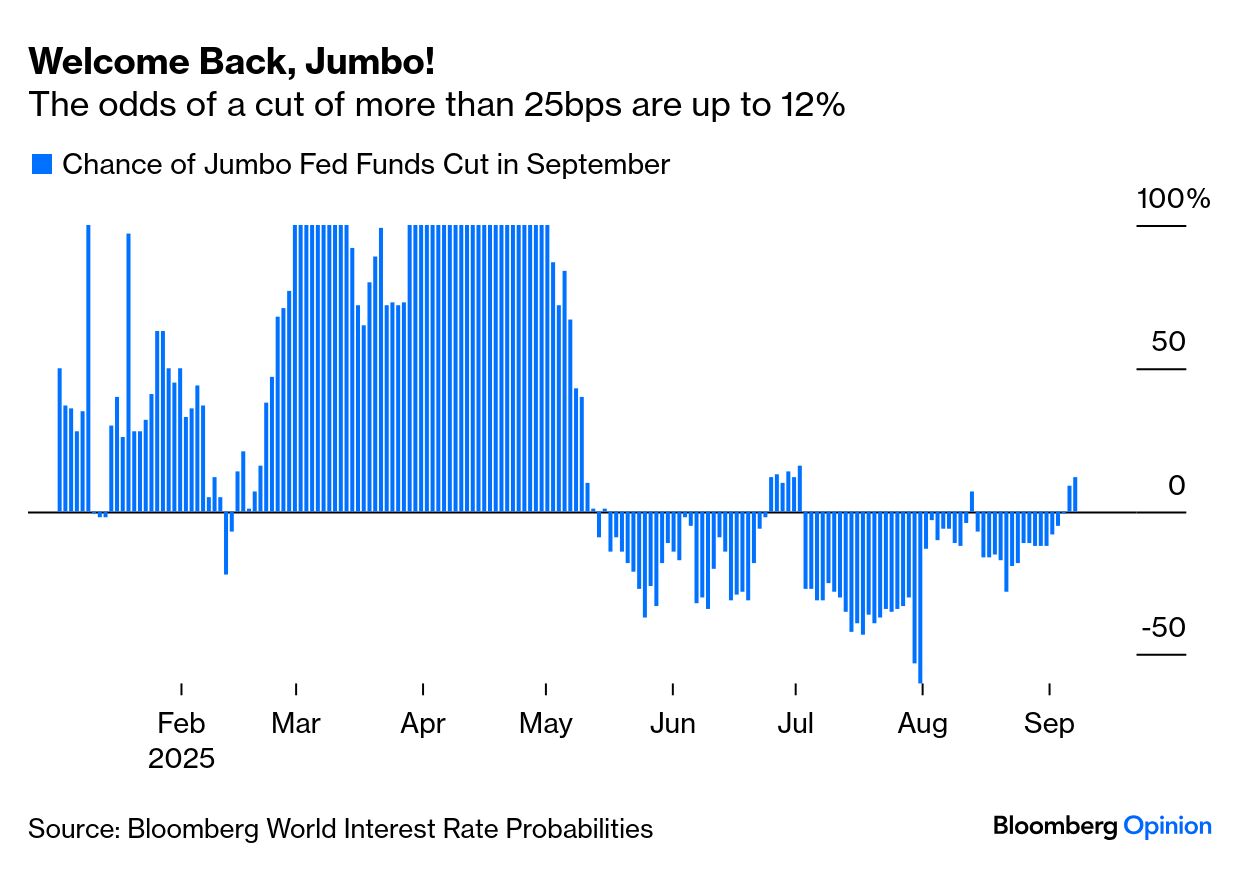

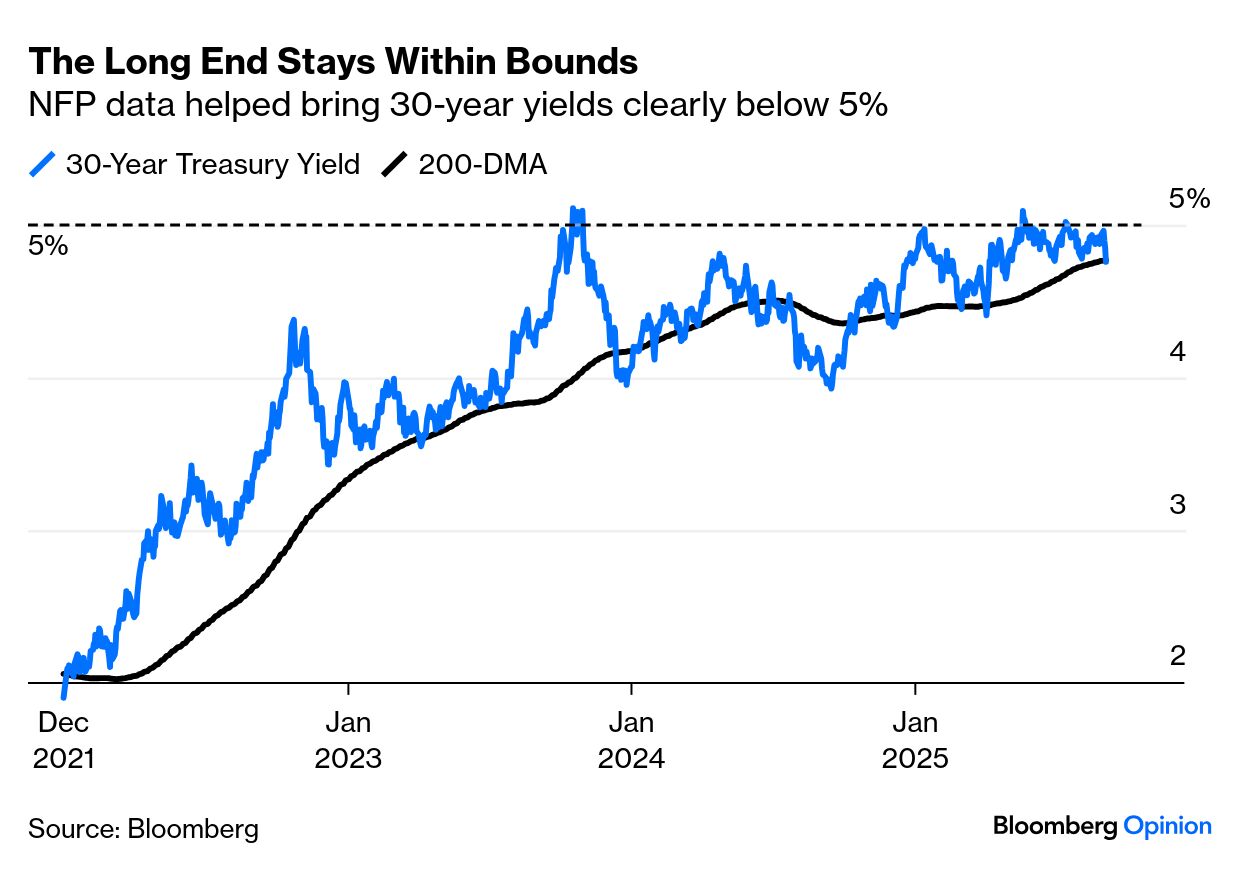

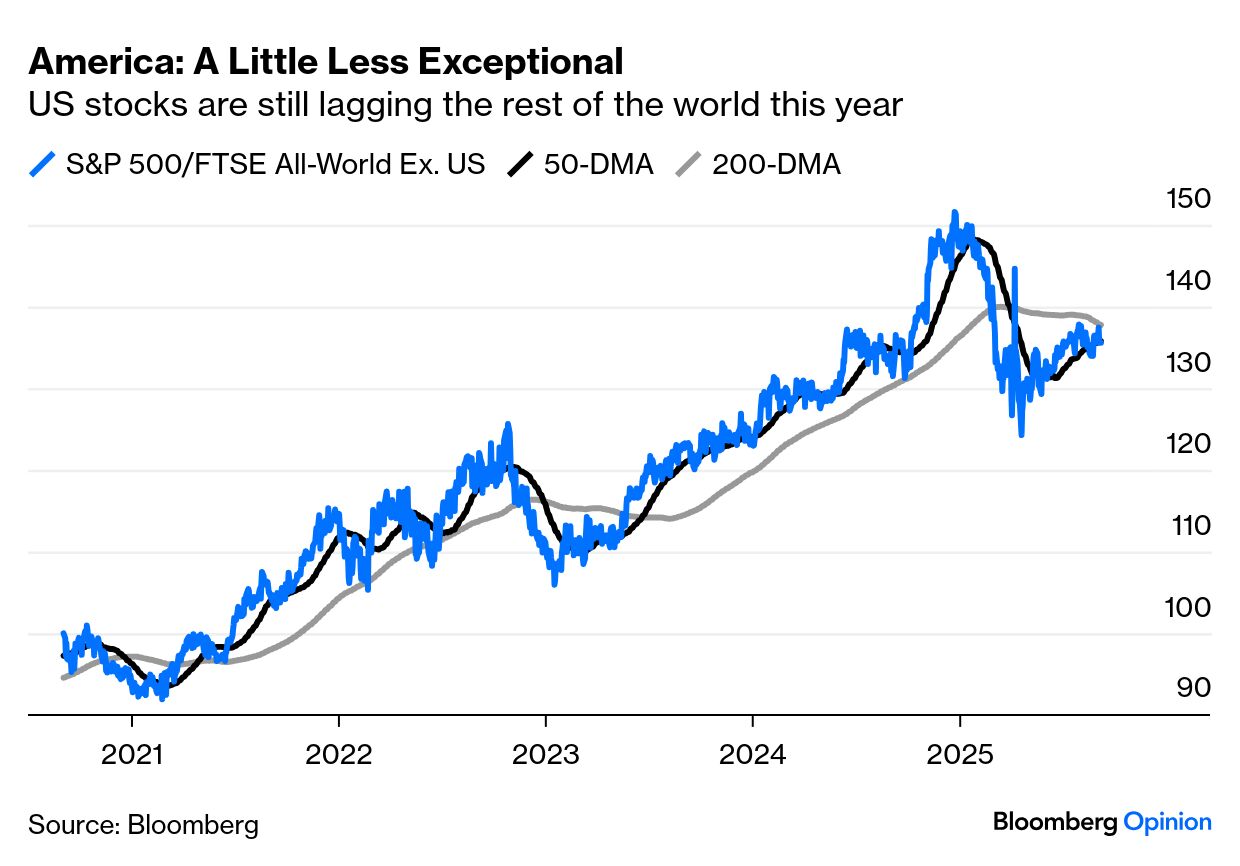

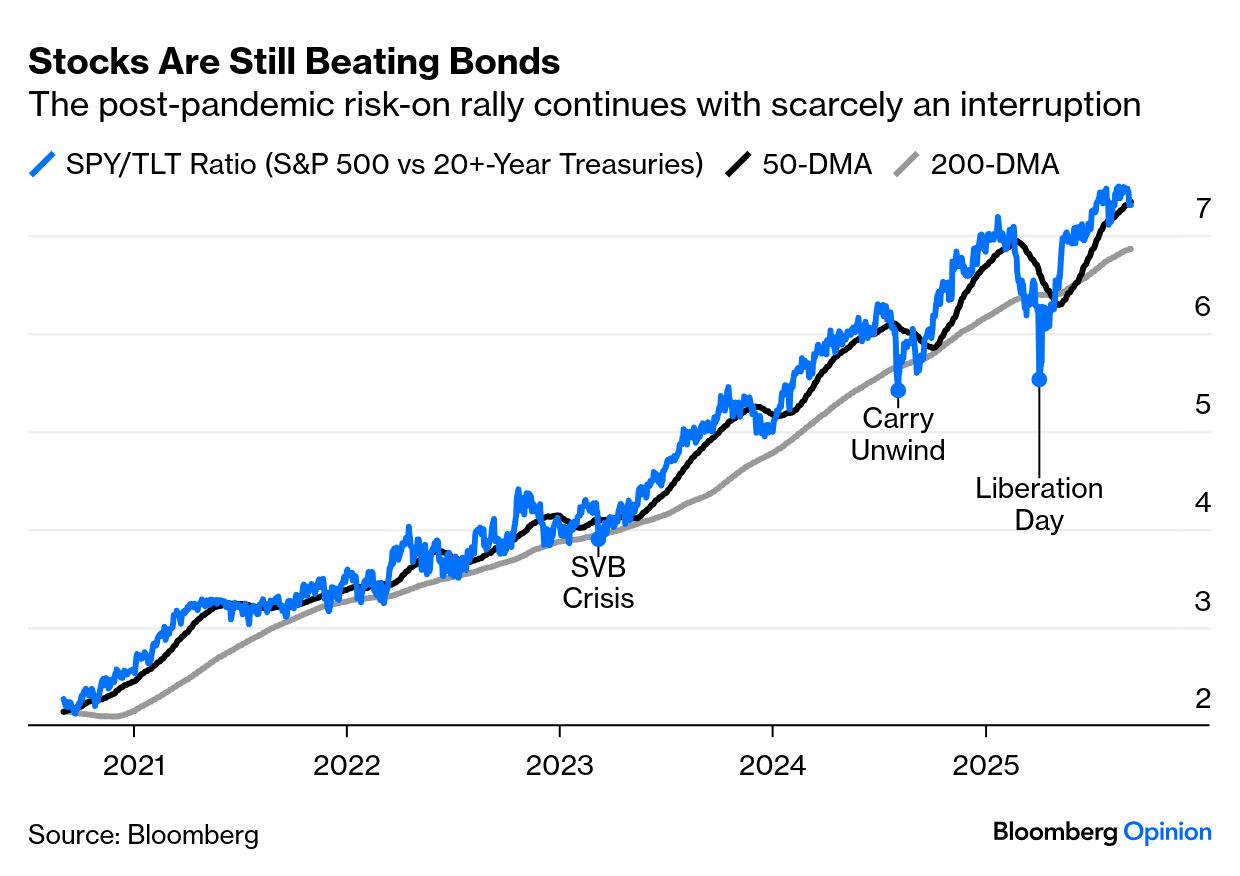

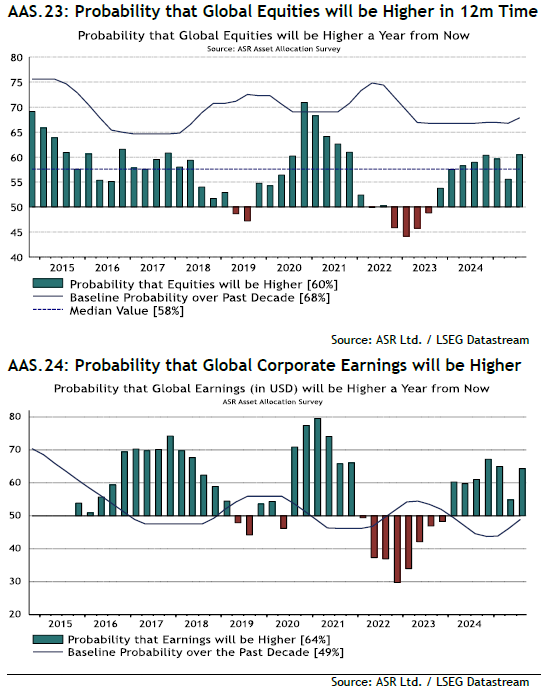

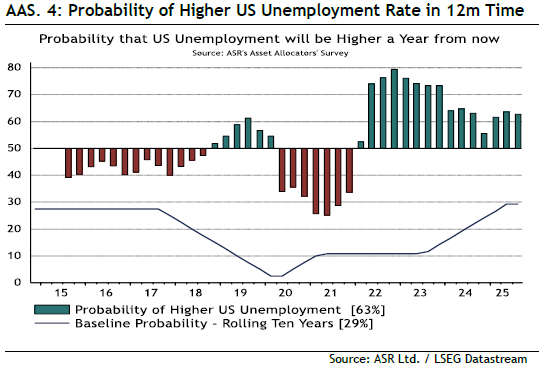

| At last, the US economic data tell a clear story. Friday’s bulletin on August unemployment showed beyond doubt that the labor market is very weak, with growth in non-farm payrolls almost extinguished: The Job Openings and Labor Turnover Survey (JOLTS) for July showed fewer vacancies, but no widespread layoffs. Hiring has slowed down, but employers are in no hurry to fire workers: The separately compiled unemployment rate also clearly deteriorated, reaching a post-pandemic high of 4.3%. All of this affects the Federal Reserve. A year ago, unemployment had risen swiftly to 4.2%. That triggered the 0.5 percentage point rise in the rate from its recent low that according to the Sahm Rule (named for Bloomberg Opinion colleague Claudia Sahm) means a recession is under way. The usual pattern is for unemployment to gain steadily for a while, and then surge much higher. Last September, the Fed responded with a “jumbo” cut of 50 basis points, and delayed that recession. The unemployment rate fell and has only now advanced back above 4.2%. The Sahm Rule no longer predicts a recession: The last 12 months make the Fed’s policy look surprisingly defensible, given the invective leveled against them. But with employment now declining, futures are pricing a fed funds cut next week as a 100% probability. Meanwhile, markets once more expect rates below 3% by the end of next year — the lowest such projection since last September: At this point, only a shockingly bad inflation number on Thursday could possibly avert a cut. The current consensus forecast, according to Bloomberg, calls for core CPI of 3.1%, so traders assume — probably correctly — that the Fed will ease even if inflation stays this high: Inflation swaps suggest that the poor jobs numbers have spurred optimism that price rises can be kept under control. Both one- and two-year inflation projections dipped sharply to end the week: After months of arguing over whether the Fed should cut in September, the issue has suddenly returned to whether they might make a “jumbo” move of more than 25 basis points. Last September’s jumbo easing seems to have worked well. Futures currently put an implicit chance of 12% of a significant move (with at least 25 basis points priced as a certainty): Rick Rieder of BlackRock suggested on Bloomberg TV that it was time for 50 basis points. Standard Chartered Plc’s Steven Englander also argues that “the combination of soft data and downward revisions justify a significant move” — but predicts the Fed won't commit to further cuts, which might be another good lesson to learn from last September. So, barring a very, very big surprise from the inflation numbers this week, the Fed will cut, and after a year of doubt the market is again confident that the fed funds rate is heading down below 3%. The consumer price index data will probably decide whether the central bank really unleashes the jumbo. Where Does That Leave Us? | The August non-farm payroll announcement was a big market event, but not totally as might have been expected. Perhaps most significantly, the numbers reined in long-run bond yields — both in the US and elsewhere — which had shown signs of breaking upward: Relative to global peers, the US continues to look less exceptional than it did. Compared to FTSE’s index for the rest of the world, the S&P 500 has stabilized, and remains well below its peak during the post-election excitement: Meanwhile, US stocks are still comfortably beating bonds, as they have done throughout the post-pandemic era. There were brief interruptions during the regional banking collapse two years ago, and again after the yen carry trade unwind in August 2024 and after “Liberation Day.” This latest slowdown is not thus far seen as a reason for bonds to outperform stocks: But there are obvious nagging worries about inflation. In gold terms, the S&P 500 is down over the last five years — in other words, it’s underperformed gold. This is not typical of broad optimism: And yet markets are in unambiguously optimistic mode. According to the latest global survey of asset allocators by Absolute Strategy Research, conducted just before the jobs numbers, big money managers expect share prices to climb over the next year, on the back of rising earnings: That’s the kind of performance that generally requires a robust economy. And yet a majority of those same allocators expect both higher unemployment and higher inflation 12 months from now: David Bowers of Absolute Strategy suggests an apparently coherent narrative: Asset allocators are convinced that central banks will look through any short-term rise in inflation and will carry on easing; and they are convinced that the US yield curve slope will steepen as short rates fall faster than long yields.

The problem, he points out, is that a steepening yield curve tends to mean that the output gap — the degree to which the economy is running below potential — is widening. That would be negative for corporate profits. Five months on from “Liberation Day,” and after an unambiguous employment report, the market still doesn’t have a coherent narrative of its own. |