| | In this edition, world leaders are doomscrolling, but investors aren’t, and energy constraints stemm͏ ͏ ͏ ͏ ͏ ͏ |

| |  | Business |  |

| |

|

- $4 gas

- Wall St.’s Gulf plans

- A fix for private credit

- Tiny homes on Compound Interest

- Judicial (in)discretion

An activist sad ghosts Snap … |

|

World leaders are doomscrolling. Why aren’t investors? “I am forced to know things about what could happen in the coming week, and the effects it will have on the economy and our daily lives, that no longer allow me to sleep,” Italy’s defense minister said yesterday. Also staring at the ceiling are South Korea’s president and European Central Bank chief Christine Lagarde, who is talking about shocks “beyond what we can imagine.” If you’re the last one sleeping soundly, here’s Germany’s military chief: “Conflict with Russia in the next few years is inevitable.” These are people with real-time data feeds and classified briefings. Markets have flinched but haven’t freaked out: Oil is well short of where many analysts think it should be, and the Nasdaq’s correction territory is driven by AI fears not global shocks. The two leading answers are resiliency and complacency. The world is either so flush with money that it can absorb any risk, or investors figure they’ll be bailed out (again) by governments if things get too bad. But there’s a third option: We’re on borrowed time. The buffer provided by oil already at sea and releases from national reserves “is now being exhausted in real time,” write the usually sanguine experts at Rystad Energy. (See below for a handy chart on when the last prewar tankers will arrive at your local ports, and maybe buy some call options on Australian stocks while you’re at it.) One way to think about it is that we’re living in the supply-side version of the pandemic’s demand shock. Scientists were warning us, and we went out to dinner anyway. Then we didn’t for a very long time. The second and third-order effects of the Iran war haven’t hit yet: crops stunted by fertilizer shortages, Asian factory blackouts, MRI rationing due to helium shortages, grocery prices hit by higher trucking costs. They will arrive in the same way the pandemic’s economic effects did, slowly and then all at once The rise of high-frequency trading convinced us that everything is priced in instantly, obscuring pockets of friction. Oil tankers move slowly. So do Marines. And all the while, the slow-motion bank run happening inside private credit marches on. For now, these funds are funding their own collapse, at quarterly intervals. It’s Silicon Valley Bank, but with some structural lag. |

|

Oil glidepath risks stalling out |

Time is running out for companies that are taking a wait-and-see approach to the Iran war’s impact. US gas prices hit the psychological cliff of $4, and skyrocketing energy costs sent Eurozone inflation to a 14-month high. The EU energy chief urged Europeans to cut travel, while Seoul is weighing imposing driving restrictions. The last shipment of Middle Eastern jet fuel will reach Britain this week, and the airline industry warned of shortages if the war continues: The Strait of Hormuz accounts for 20% of the world’s oil, but 40% of Europe’s. Meanwhile, Unilever blamed the war for a hiring freeze, an early sign of the layoff air cover we predicted earlier this month. |

|

Wall St. sticks with the Gulf |

The war in Iran is a stark reminder that, for all its money and glitz, the Middle East remains a volatile place. But borrowing one of Goldman Sachs’ founding principles, Wall Street remains long-term greedy. The war has “no impact on our excitement about going all in,” said David Manlowe, CEO of the $92 billion credit manager owned by Franklin Templeton, told Semafor’s Matthew Martin. “We’re thinking about the future in decades.” General Atlantic CEO Bill Ford told Semafor last week that “the biggest mistake we could make is to pull back and not be prepared when the markets become more investable.” Gulf leaders and regulators have long memories. Several executives pointed to the cautionary tale of Citigroup, which sold its stake in a Saudi bank in 2004 and was unable to return to Riyadh until 2017. |

|

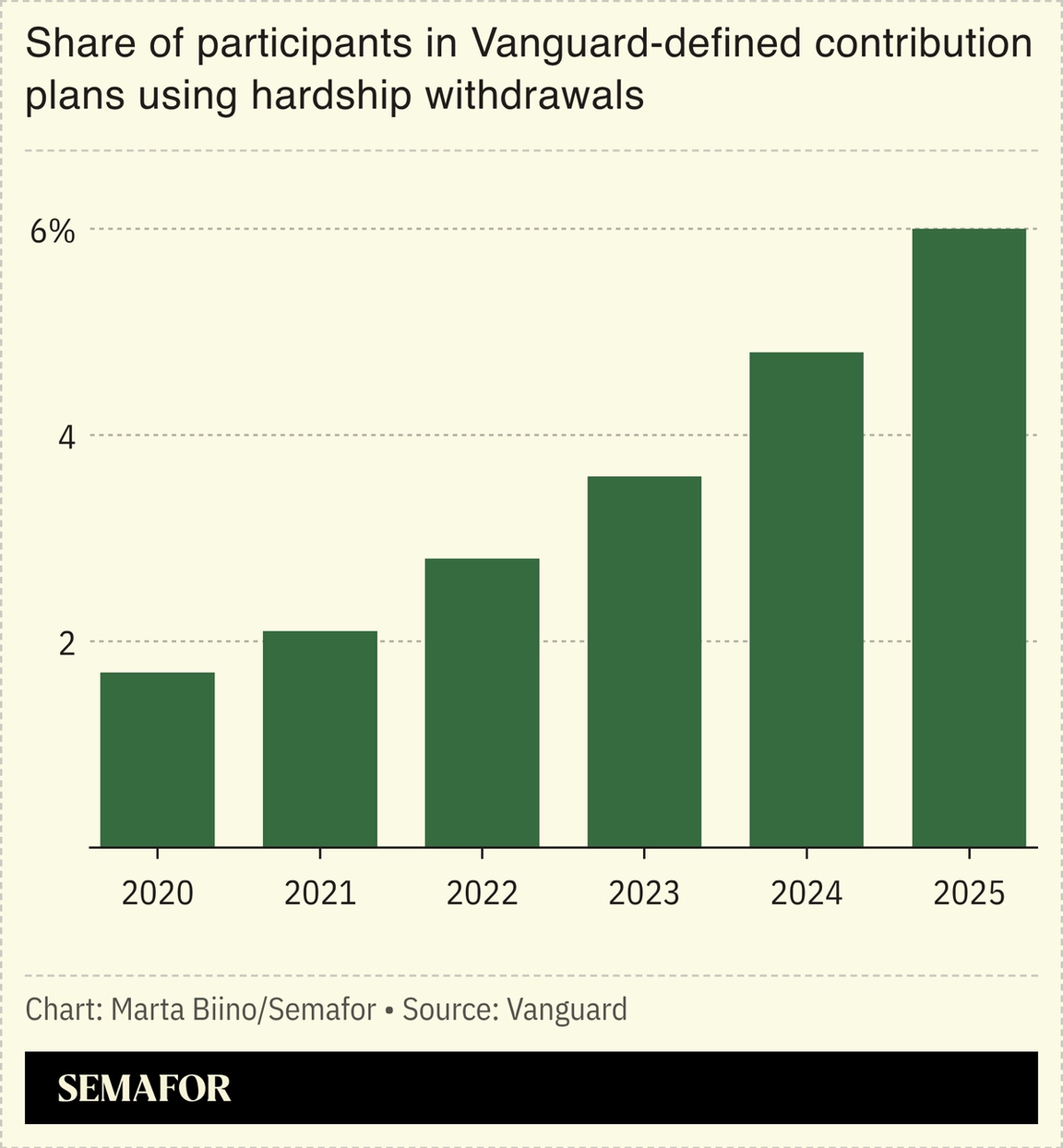

A 401(k) fix for private credit |

The Trump administration is offering private credit a way out of its problems. Opening up 401(k) accounts to alternative assets, a move the Labor Department advanced with new employer rules on Monday, would help solve the crisis now facing investment firms whose retail shareholders are running for the exits. Alternative assets are “not a carrot that you pull out of the ground every day to see how it grows,” KKR’s Alisa Wood told Semafor. The problem is that funds marketed to retail investors allow just that, offering them the chance to take out a sliver of their money on a quarterly or monthly basis. It’s almost designed to malfunction when nerves are high. “The least satisfying, but most accurate, thing to be said about private credit right now is that it’s working exactly as it’s supposed to,” we wrote last week. Retirement accounts are harder to cash out of, because doing so brings steep taxes. That would give individual investors exposure to alternative assets and would protect them from their instincts to panic at the worst moments. Historically less than 2% of Americans tapped their 401(k) for emergency cash every year. That number has risen, but those redemptions could be more easily met by selling stocks and bonds that are expected to remain the bulk of 401(k) assets. |

|

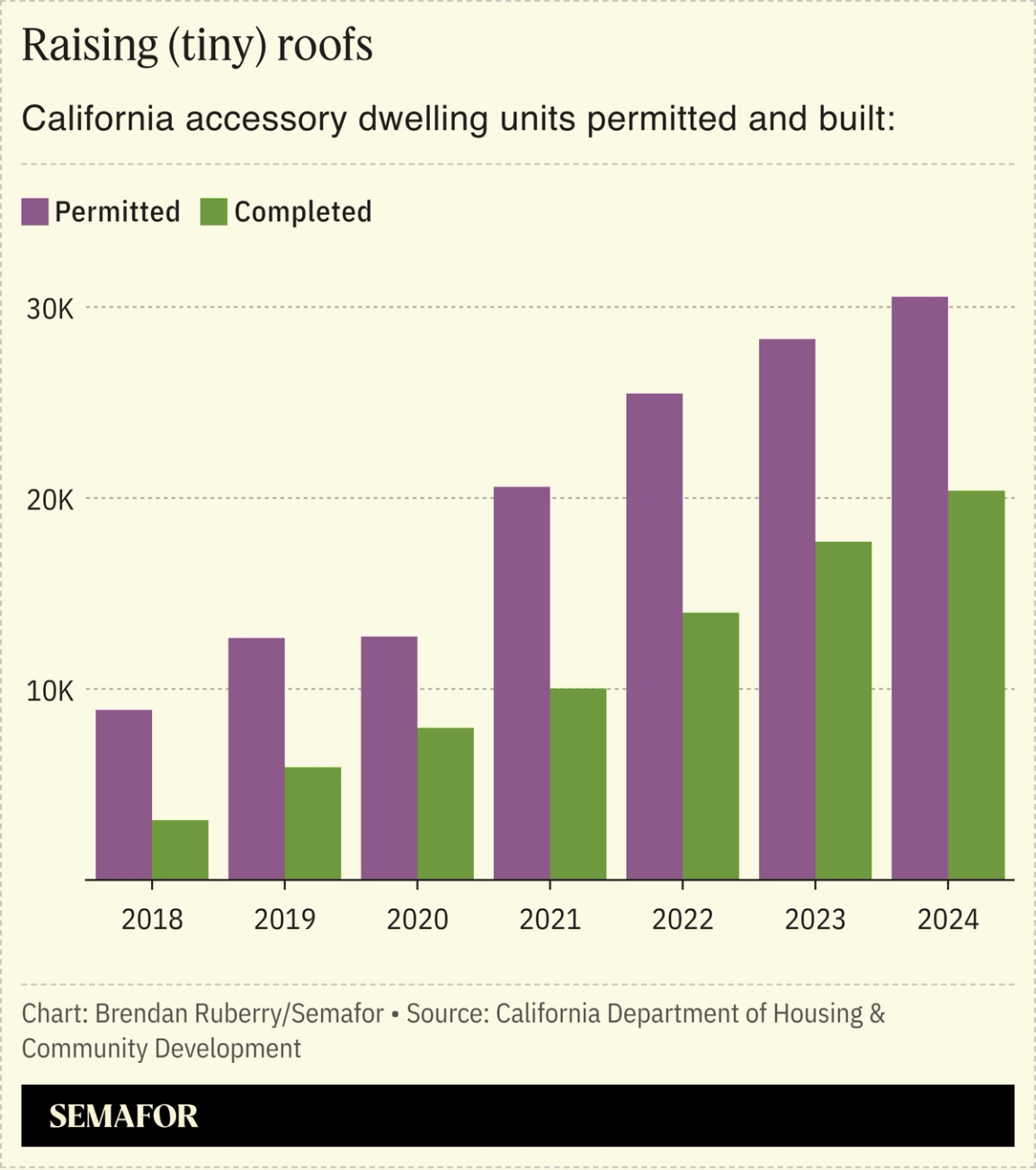

Can tiny homes fix America’s housing? |

Tiny homes, prefabricated and dropped into backyards across America, could solve two great shortages in the US economy: Housing and cash-generating investments.

The CEO of Samara, which spun off in 2022 from Airbnb and makes apartment-sized housing units that fit in people’s backyards, said the easing of zoning regulations and an appetite among investors should make tiny homes a financeable asset that gains in value over time.

Banks “understand the mortgage of the front yard very well. We’re trying to create a different asset class” in the backyard, Mike McNamara said on Semafor’s Compound Interest show. For now, Samara is providing the financing itself, offering to lend 100% of the cost of a unit if the main house has enough equity built up. “We love it as an asset class,” he said. So will Apollo. |

|

LinkedIn trips up Musk nemesis |

Daniel Cole/Reuters Daniel Cole/ReutersThree lawsuits involving Elon Musk, including one over his giant pay package, will be reassigned after the presiding judge appeared to endorse a LinkedIn post critical of the billionaire. Kathaleen McCormick, the chief judge in Delaware’s business court, is a longtime bugbear for Musk, forcing him to complete his $44 billion takeover of Twitter after he got cold feet and invalidating his Tesla pay package in a decision that was partly overturned on appeal. Musk cited “activist judges” in his decision to move Tesla’s legal home from Delaware to Texas, which set off a mini-exodus of ideologically aligned tech companies. McCormick wrote Monday that she hadn’t seen, or meant to like (actually, it was a heart-in-hands emoji) the LinkedIn post and rejected Musk’s lawyers’ accusations of bias, but said she would hand off the cases. This isn’t the first time a Delaware judge has gotten in trouble on LinkedIn; it may be time for a policy. — Rohan Goswami |

|

➚ BUY: Oh, Canada! Canadian stocks are bucking the trend of other falling stock exchanges, with the TSX Toronto index more skewed toward mining and commodities. ➘ SELL: Air Canada. The carrier’s CEO resigned over his inability to express condolences in both English and French following a deadly crash last week. Is this the first CEO casualty of the global resurgence in country-first capitalism? |

|

Companies & Deals- Flavortown is reaching capacity: Another “global flavor” giant is in the offing. McCormick is buying Unilever’s much-larger food business in a $60 billion transaction, just days after another food-related megadeal: Sysco’s $29 billion acquisition of Restaurant Depot.

- Blame the robots: The former CEOs of Coca-Cola and Walmart said AI hastened their retirements, arguing the companies needed a chief with better understanding of the technology.

WatchdogsMarkets- The Art of the Broker-Dealer: Defense Secretary Pete Hegseth’s broker tried to buy defense stocks on the eve of the Iran war, the Financial Times reported. The Pentagon denied the allegations and demanded a retraction; the FT stands by its reporting. A reminder that informed trading doesn’t always pay: The stocks in question have declined 13% since the start of hostilities.

|

|

| |  | | | You’re receiving this email because you signed up for briefings from Semafor. |

|