|

|

|

|

|

|

|

|

|

More than half of Canadians say they’re struggling to keep up with bills, according to the Financial Consumer Agency of Canada. John Raoux/The Associated Press

|

|

|

|

|

Oh, hi again. Debt can feel heavy, and it doesn’t just affect your day-to-day life – it can shape what your future looks like. Today, we’re diving into some practical steps to tackle debt head-on. |

|

|

|

|

|

|

|

|

|

|

A recent report from the charity Prosper Canada found that on average, low-income Canadians carry $34,359 in overall debt because of a lack of savings. |

|

|

|

|

At the same time, more than half of Canadians say they’re struggling to keep up with bills, according to the Financial Consumer Agency of Canada. Insolvencies are ticking up too, with 4.2 out of every 1,000 adults filing in 2024, the highest rate since 2019. |

|

|

|

|

If you’re feeling stretched, you’re not alone. The question is what to actually do about it. Here are four practical ways to start building a financial plan when debt feels overwhelming: |

|

|

|

|

1. Clearly understand what you owe (even if it’s uncomfortable) |

|

|

|

|

Start by listing every debt, including credit cards, lines of credit, student loans – everything. Include the interest rate and minimum payment. This is the foundation of any plan; without it, you’re left guessing. From there, you can choose a payoff strategy that works best for you, whether that’s tackling the highest-interest debt first or smaller balances for quick wins. |

|

|

|

|

2. Build a small buffer, even while paying debt |

|

|

|

|

It might feel like every extra dollar should go toward debt, but that can backfire. If something unexpected comes up, you’re more likely to rely on credit again. Even a small emergency fund (think $500 to $1,000) can help break that cycle and give you a bit of breathing room. |

|

|

|

|

3. Lower your interest rate before trying to pay faster |

|

|

|

|

|

|

|

|

A lot of people focus on paying debt down as quickly as possible, but another option is making that debt cheaper. That could mean transferring a balance to a lower-rate card, consolidating debt or even negotiating with a lender. |

|

|

|

|

4. Don’t leave money on the table |

|

|

|

|

|

|

|

|

|

|

Subscribe to the Retire Rich newsletter

Are you reading this newsletter on the web or did someone forward the e-mail version to you? If so, you can sign up for Retire Rich here. |

|

|

|

|

|

|

|

|

|

|

|

|

|

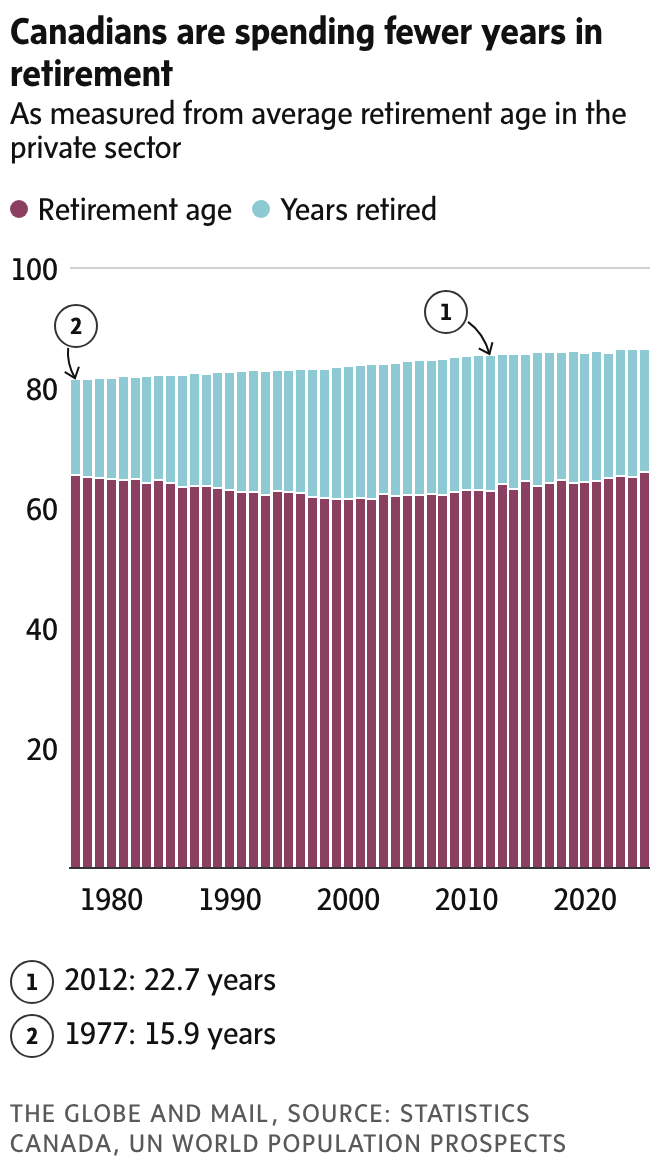

Canadians are spending fewer years in retirement than a decade ago, says Frederick Vettese, former chief actuary at Morneau Shepell. |

|

|

|

|

Yes, but: That’s not necessarily bad news. For those working later into life, a shorter retirement could make it easier to save for their needs, even as life expectancy continues to edge higher. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The situation: Clement, 45, and Uma, 46, are high-earning parents with two young kids, strong pensions and about $3.5-million in assets. With rising incomes, they’re considering buying a $2-million cottage and renovating their home, while still saving for their children’s education and aiming for $120,000 a year in retirement spending. |

|

|

|

|

The numbers: The couple earns more than $300,000 combined, has more than $850,000 in non-registered investments, $463,000 in TFSAs and roughly $540,000 in RRSPs, plus a $1.4-million home. They plan to use their TFSAs and non-registered accounts for the cottage down payment, while relying on pensions, RRSPs and CPP for retirement income. |

|

|

|

|

Advice from a financial planner: They can afford the cottage and still retire comfortably. Their pensions provide a strong foundation and projections show their savings can last into their 90s. But the cottage purchase will reduce liquidity, so the planner recommends careful withdrawal strategies, continual plan check-ins and strong insurance coverage to manage risks along the way. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|