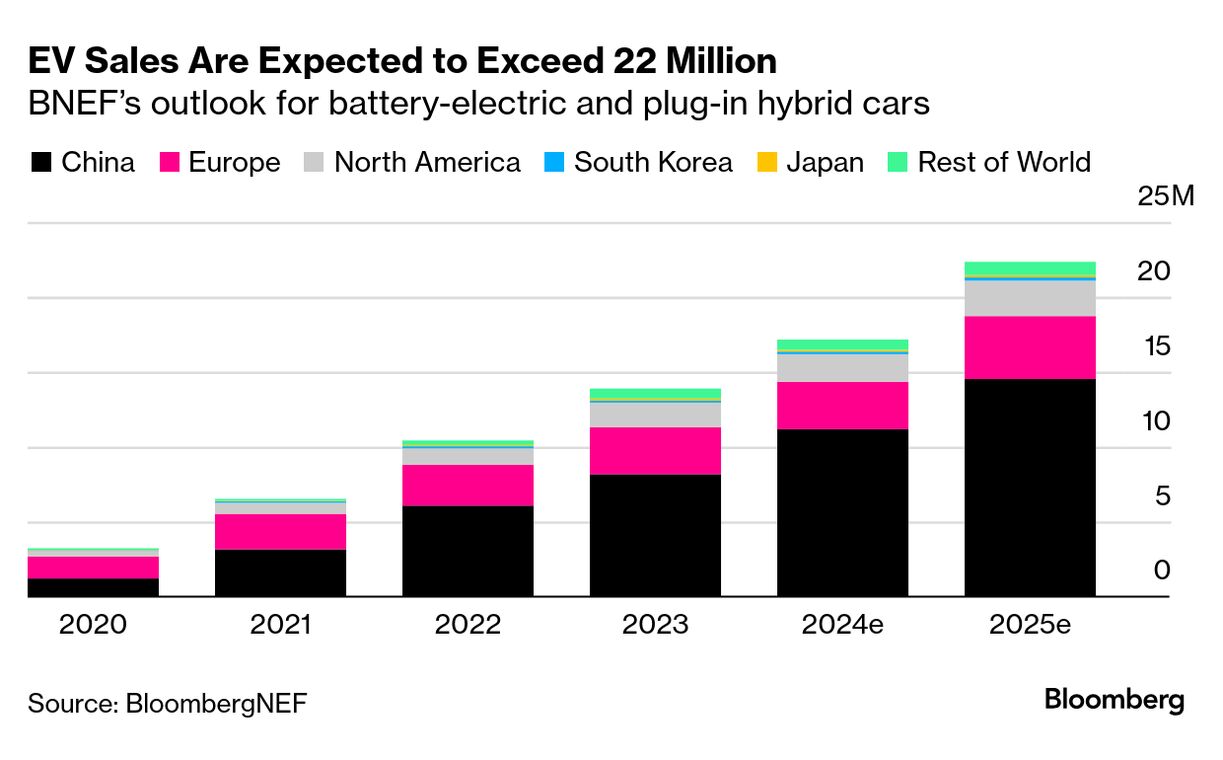

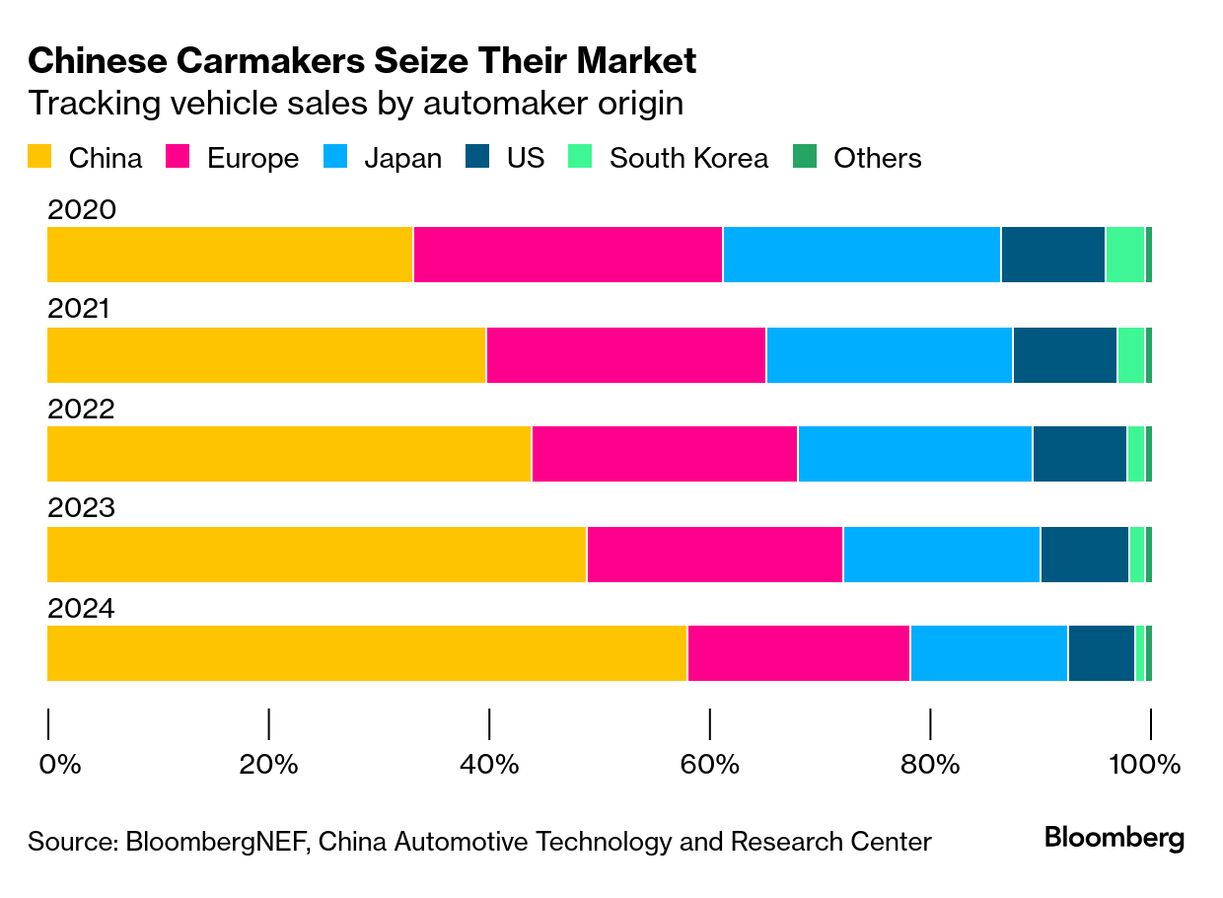

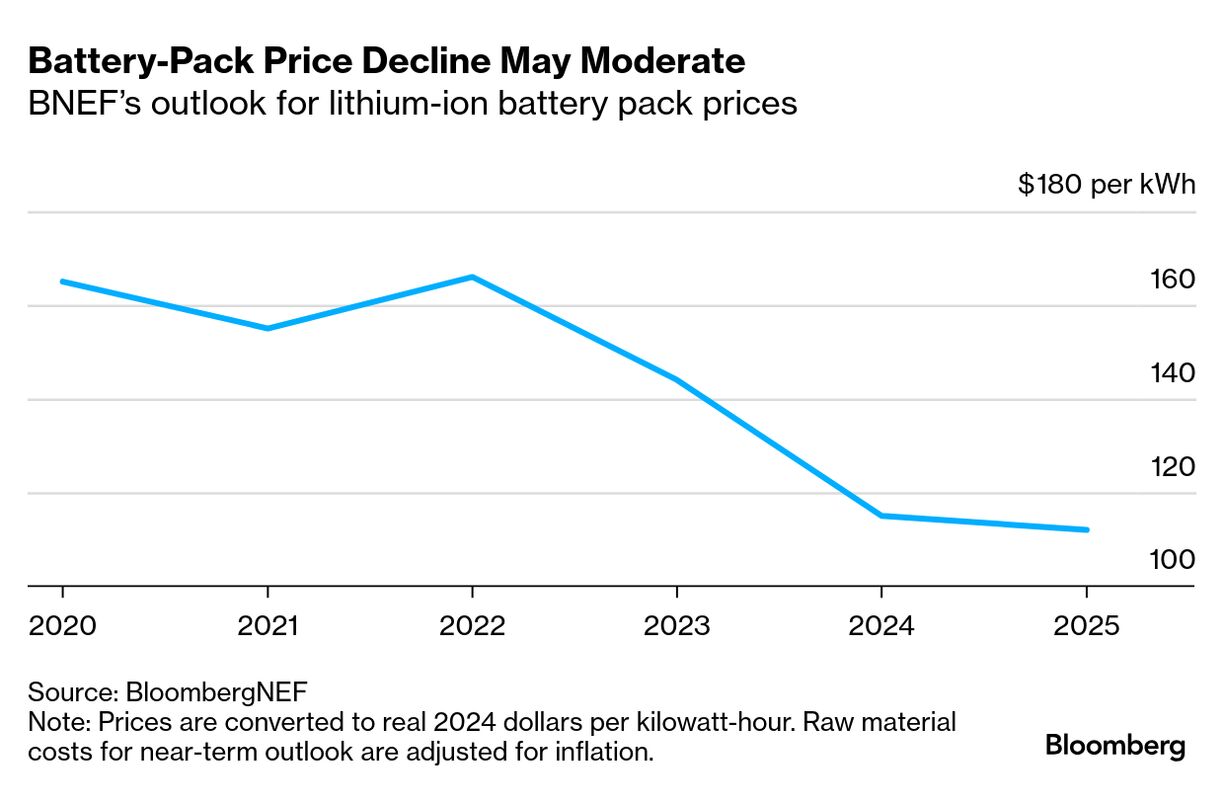

| Thanks for reading Hyperdrive, Bloomberg’s newsletter on the future of the auto world. BNEF subscribers can read the extensive version of this report here. Emissions rules, the incoming Trump administration, falling battery prices and ever more intense competition in China will all shape clean transport markets this year. The following four topics to watch are a snapshot of what BloombergNEF’s team thinks will be some of the most noteworthy developments in 2025. EV sales defy the headwinds and deliver another record year We expect global sales of battery-electric and plug-in hybrid vehicles to increase 30% to 22 million, with 61% of those being fully electric. The EV share of global vehicle sales should come in around 27% (all-electric at 16%), up from about 21% in 2024. We see carmakers selling roughly 14.5 million EVs in China, representing 65% of EVs sold globally. Sales in Europe will grow the fastest, driven by automakers doubling down on EVs to comply with the region’s emissions targets. With affordable EVs like the Renault 5 E-Tech, Skoda Epiq and Hyundai Inster coming to market, EV sales in Europe should increase 33% to just under 4.2 million units, pushing the share of sales over 30%. In the US, the EV market is bracing for a swift rollback of fuel-economy standards under President Donald Trump. Without those rules, automakers will be under limited pressure to increase sales of EVs or introduce new models. While the EV tax credit is also under threat, it will take longer to repeal, which will buy consumers time. We expect EV sales in the US to total just over 2 million, accounting for 13% of new-car purchases and up moderately from 2024. Another big automaker exits the China market International automakers are being squeezed out of China’s vehicle market as EV adoption accelerates. In 2024, almost 90% of all EV sales in the country were from domestic automakers. Most international brands still don’t have competitive EV offerings on the market, and we expect their overall share in China to fall again in 2025. Alarm bells have been ringing across boardrooms for over 18 months now, and virtually all international automakers are reassessing or restructuring their operations in China. Strategies include closing factories and laying off staff (Ford and GM) and buying stakes in local rivals like Leapmotor (Stellantis) and Xpeng (Volkswagen). Many are also now launching lower-priced EV models to try and stem the losses in market share. It’s going to be too late for some, and we expect another major automaker to pack up and leave in 2025. Calling exactly which one is difficult. Regardless of who exits next, it won’t be the last to go. International automakers misjudged the speed of China’s pivot to electric and how fast domestic rivals were coming up the curve. EV policy changes in Europe Several automakers in Europe have been calling for a review of the EU’s vehicle CO2 emissions standards. They claim vehicle manufacturers’ inability to meet the rules poses an existential threat to the European car industry. Although the European Commission has so far stood firmly behind keeping the targets unchanged, BNEF expects it will succumb to pressure in 2025 and soften them in some way.  The Rue de la Loi running through central Brussels. Photographer: Jasper Juinen/Bloomberg Two compliance years are at stake: 2025, for which the targets call for a 15% fleet-wide CO2 emission reduction compared to the 2021 level; and 2035, with targets set at a 100% reduction in fleet-wide CO2 emissions. While BNEF expects the 2035 target to remain unchanged, at least until a previously planned review in 2026. Amendments to the 2025 targets are much more likely. According to the analysis by BNEF, at least 29% of new-car sales will have to be EVs this year for the industry to comply. The final share will depend on the mix between battery-electric and plug-in hybrid vehicles. One way the European Commission might soften the 2025 compliance struggle involves allowing automakers to miss the targets this year, but obliging them to make up for the 2025 shortfall with overcompliance in 2026 or 2027. Although this would delay some EV adoption in the region, it would at least ensure automakers continue to invest in electrification. Another option could be to scrap fines for non-compliance. This would be a huge blow to the region’s most important transport decarbonization policy, as stricter targets without penalties will not be taken seriously. Battery price declines slow after a big drop in 2024 Battery prices saw another year of big declines in 2024, driven by cell manufacturing overcapacity, economies of scale, lower prices of metals and component prices, the continued shift to lower-cost lithium iron phosphate (LFP) batteries and lower-than-expected EV sales growth. Average pack prices dropped by 20% to $115 per kilowatt-hour, though some segments are already much lower. BNEF expects pack prices to decrease by a further $3 per kWh in 2025 in our base case. Metal prices may rise in the next three years as geopolitical tensions, tariffs on battery metals and stalled new projects disrupt supply and demand dynamics. Additionally, tariffs on finished battery products may lead to distortionary pricing dynamics and slow end-product demand. However, BNEF still expects higher adoption of LFP chemistries, continued market competition and improvements in technology, material processing and manufacturing to continue exerting downward pressure on battery prices. Based on BNEF’s high and low scenarios for lithium, nickel and cobalt, average global battery pack prices in 2025 could range between $109 per kWh and $116 per kWh. — By Colin McKerracher, Aleksandra O’Donovan, Yayoi Sekine and Evelina Stoikou  A Tesla is destroyed due to the Palisades Fire on Jan. 8. Photographer: Michael Ho Wai Lee / SOPA Images/SIPAPRE As the smoke clears from devastating Los Angeles wildfires, efforts to clean up the affected areas are being complicated by burnt-out electric vehicles. There were over 431,000 Teslas in operation in the Los Angeles area as of October 2024, according to data from S&P Global Mobility. Based on new registrations, their market share locally was three times that of the rest of the nation. A lot of the cars in the evacuation area were battery-powered, said Jacqui Irwin, a state assembly member representing the Pacific Palisades, one of the neighborhoods hardest hit by the fires. “We’ve heard from firefighters that those lithium batteries” burned near homes “for much longer.” |